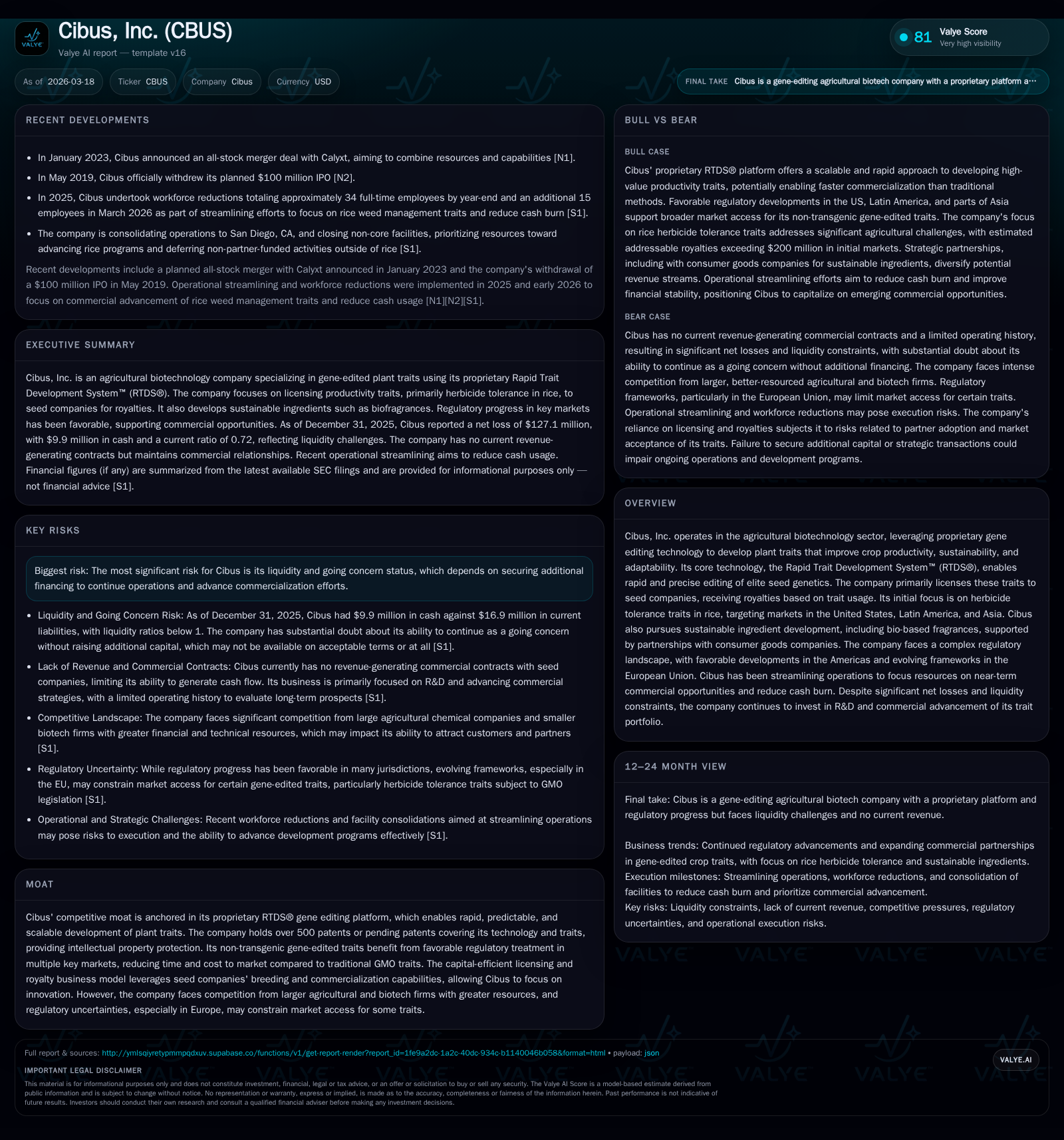

Cibus Inc. Focuses on Gene-Edited Rice Traits Amid Ongoing Operating Losses and Liquidity Pressures

Cibus leverages proprietary gene editing technology to develop plant traits with a royalty-based licensing model but faces significant financial and regulatory challenges.

Cibus, Inc. operates in agricultural biotechnology using its Rapid Trait Development System™ (RTDS®) to create non-transgenic gene-edited traits, primarily targeting herbicide tolerance in rice across key global markets. Historically, the company has incurred substantial operating losses, with limited commercial revenue and significant liquidity constraints, raising going concern considerations. Its future growth relies on commercializing rice herbicide tolerance traits and expanding sustainable ingredient offerings while navigating evolving regulatory landscapes and competitive pressures from larger agri-biotech firms.

Company Overview

Cibus, Inc. is an agricultural biotechnology firm specializing in the development of plant traits through proprietary gene editing technologies. Its flagship RTDS® platform significantly reduces the time required to develop gene-edited plant traits by enabling precise edits directly in elite seed genetics within approximately one year [S1][S6]. This proprietary system combines advanced gene editing techniques with AI-driven tools to accelerate breeding cycles—a process referred to by Cibus as "industrializing breeding," which positions it competitively within the seed trait marketplace [S17].

The company principally targets productivity traits—genetic modifications aimed at enhancing crop yields by addressing weeds, pests, diseases, or environmental stresses like heat and drought. Among these, Cibus prioritizes herbicide tolerance (HT) traits in rice for initial commercialization across regions including the United States, Latin America, and Asia. Management estimates that these rice HT traits have a potential annual addressable royalty pool exceeding $200 million upon full market penetration [S6].

Historical Performance & Financials

Cibus has maintained a loss-making profile throughout its history due to heavy investments in R&D and limited commercial traction so far. The company's revenue remains insignificant—reported revenue stood at only $508,000 back in 2017—and there has been no reported material royalty income from commercial licensing agreements as of late 2025 [F1][S1].

Operating losses have been substantial: operating income improved from negative $258 million in 2024 to negative $97.5 million in 2025 but remain sizable relative to resources available [F1]. Net losses continue unabated with $127 million lost in 2025 alone.

Cash flows from operations have consistently been negative (over -$50 million most recently), with minimal capital expenditure reflecting focused spending on core R&D projects rather than broad infrastructure investment [F1]. The current financial position reveals acute stress: as of December 31, 2025, cash and equivalents were roughly $9.9 million against current liabilities of $16.9 million resulting in a current ratio below one (0.72), indicating liquidity challenges [F1].

Historical equity has progressively eroded due to accumulated losses falling from $293 million at the end of 2023 down to about $21.8 million at end-2025. These trends underline the company's dependence on successful capital raises or partnerships moving forward [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -127 | -51 | -98 | 1 | +49.4% |

| 2024 | -251 | -58 | -258 | 1 | +6.1% |

| 2023 | -268 | -46 | -319 | 4 | -1484.4% |

| 2022 | -17 | -19 | -22 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -51 | -582.2 |

| 2024 | -59 | -272.8 |

| 2023 | -51 | -91.2 |

| 2022 | -21 | -233.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue data beyond FY2017 is unavailable; operating income shows improvement but remains negative.

Business Model & Commercial Strategy

Cibus’ core strategy centers around licensing its productivity traits—primarily non-transgenic gene-edited traits—to major seed companies who integrate them into elite seeds and manage bulk-up and commercialization processes. Royalties accrue based on trait usage per bag of seed sold or acreage planted harboring Cibus-developed traits [S6][S16]. This approach allows Cibus to remain lean by focusing on R&D innovation instead of moving downstream into seed production or distribution.

The licensing model is well-established within the industry but requires successful negotiation with large seed firms who may possess their own in-house gene editing capabilities or who might opt for competitive technologies from dominant agrochemical companies such as BASF or Bayer Crop Science [S8][S9]. Cibus maintains an extensive intellectual property portfolio—including over 500 patents or pending applications—that protects both its RTDS technology and individual trait developments providing barriers against direct competition [S8][S23].

Partnerships play a strategic role beyond the Americas where regulatory frameworks for gene-edited crops vary widely. In regions like India or much of Asia outside China—as well as Latin America—Cibus explores alternative customer partnership models that extend beyond pure licensing arrangements to accelerate market access and adoption [S6].

Additionally,Cibus pursues secondary programs around sustainable ingredient products such as lauric oils and bio-based fragrances linked partly through consumer goods collaborations. This diversified product line complements productivity traits but remains early-stage with partial partner funding essential for development progress [S6].

Regulatory Environment & Risks

A critical competitive advantage for Cibus lies in the regulatory status of its gene-editing technology. Unlike traditional GMOs involving transgenic modifications foreign DNA insertions—often subject to onerous approvals—Cibus’ productivity traits are classified as non-transgenic gene-edited products. Multiple jurisdictions including the United States (via USDA oversight), Canada, Argentina and Chile have adopted regulatory frameworks treating these products more like conventionally bred crops rather than GMOs lowering time-to-market hurdles [S12][S23].

However,this regulatory favorable landscape is far from uniform globally. Europe remains cautiously evolving new policies that could impose increased burdens particularly for herbicide tolerance traits considered sensitive; other countries retain undefined or restrictive policies presenting market access uncertainties that may limit deployment geography [S12][S23]. Regulatory changes at any stage could increase costs or delay commercialization impacting licensee decisions.

Besides product regulation,Cibus faces compliance demands related to environmental health & safety laws governing chemical use within R&D labs plus export/import controls that complicate international sales channels exposing it to penalties if breached inadvertently [S5][S10].

Public acceptance also factors into regulatory dynamics as apprehensions toward biotechnology persist among some stakeholders despite scientific consensus regarding gene editing safety; reputational damage through misinformation campaigns poses indirect risks affecting adoption rates [S19][S27].

Competitive Landscape & Differentiation

The agricultural trait domain is dominated by a handful of multinational agrochemical firms like BASF,Bayer Crop Science,Corteva,and Syngenta—each sustaining large R&D budgets,captive seed portfolios,and integrated marketing networks that represent formidable barriers for smaller innovators like Cibus [S8][S9]. Several competitors engage simultaneously as customers/licensees creating complex interdependencies.

Nonetheless,Cibus leverages its unique RTDS platform’s speed,economy,and precision coupled with focused crop targeting offering an appeal for seed companies seeking fast integration into elite germplasm.[S16][S17] With active platforms spanning multiple key row crops including canola,wheat,sugar beet,and soybeans undergoing expansion efforts,the breadth of potential markets theoretically supports scale economies.[S17]

Yet,the risk that large seed companies internalize their own gene editing pipelines remains valid potentially shrinking customer opportunity sets.[S9] Further,the rapidly evolving AI-enhanced biotech landscape amplifies innovation competition requiring sustained investment.[S26]

Future Growth Prospects & Milestones

Near-to-medium term growth hinges principally on advancing commercialization of multiple rice herbicide tolerance trait candidates across target geographies.The realization of estimated royalty streams exceeding $200 million annually post-market launch frames management’s value thesis though no firm contracts currently generate material revenues.[S6]

Cibus also plans incremental rollouts into other crops leveraging its Trait Machine system’s scalable design.[S17] Completion of a fully operational soybean platform represents a notable milestone under development bolstering portfolio diversity.

Continued engagement in sustainable ingredient products supported by partially partner-funded initiatives adds optionality but remains subordinate.

Commercial traction depends critically on license agreement signings,milestone payments,and market adoption rates by seed companies and farmers—events currently not concretely evidenced though management intends pipeline prioritization accordingly.

Watchpoints include:

- Receipt of first meaningful royalties demonstrating market acceptance,

- Regulatory approvals especially beyond favorable American jurisdictions,

- Successful capital raising or partnership deals relieving liquidity constraints,

- Progression through field trials validating trait efficacy,

- Retention of core scientific talent amid organizational streamlining efforts.

Capital Allocation & Returns Profile

Given ongoing heavy investment phase,Cibus’s financial statements reflect negligible returns with an approximate return on equity around negative 582% based on latest net loss relative to equity base at year-end 2025[F1]. Operating cash flow remains deeply negative around -$50.6 million despite cost control efforts.

Capital expenditures are minimal—in line with modest physical asset requirements—hovering under $600 thousand most recently signaling economic model focused on intangible asset creation via R&D rather than fixed asset build-out[F1].

The firm has no reported dividends nor recent share repurchases indicating all available capital directed towards sustaining operations amidst losses.[F1]

Liquidity is potentially critical over short term.Evidence points towards substantial doubt regarding going concern viability absent additional financing measures consistent with disclosures reporting needs for new equity or debt capital which may be complicated by Nasdaq listing rules requiring shareholder approval[S1].

Cash burn reduction initiatives via workforce rationalizations and facility streamlining aim at extending runway but may risk impeding operational momentum[S2,S26]. The Board continues evaluating strategic options including potential sale or partnerships intended to maximize shareholder value amidst these challenges[S1].

Summary

Cibus seeks to carve out a niche within agricultural biotechnology leveraging differentiated proprietary gene-editing technology capable of accelerating plant breeding cycles while avoiding GMO classification hurdles common among competitors. The focus on non-transgenic herbicide tolerance rice traits combined with sustainable ingredient developments presents tangible avenues for future upside. However,the company remains early-stage facing typical biotechs’ uphill battles characterized by significant operating losses,difficult liquidity conditions,and absence yet of meaningful revenue streams. Regulatory uncertainties outside certain American markets coupled with formidable competition reinforce the inherent risks. Execution success depends heavily on advancing license agreements translating innovations into royalties,navigating evolving regulations,to securing sufficient financing,to preserving talent,and achieving market adoption within constrained time horizons. Investors should recognize this profile represents high-technology venture dynamics requiring patience aligned with scientific validation,milestone achievements,and capital market receptivity.

This analysis synthesizes publicly available SEC filings including detailed annual reports (10-K), quarterly filings (10-Q), and recent corporate disclosures alongside validated financial data without providing investment advice or price guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments