Pelthos Therapeutics' Early Commercial Challenges and Strategic Position in Dermatology

Formed in 2025 via merger, Pelthos advances FDA-approved dermatology products leveraging proprietary nitric oxide technology while navigating significant operating losses and capital needs.

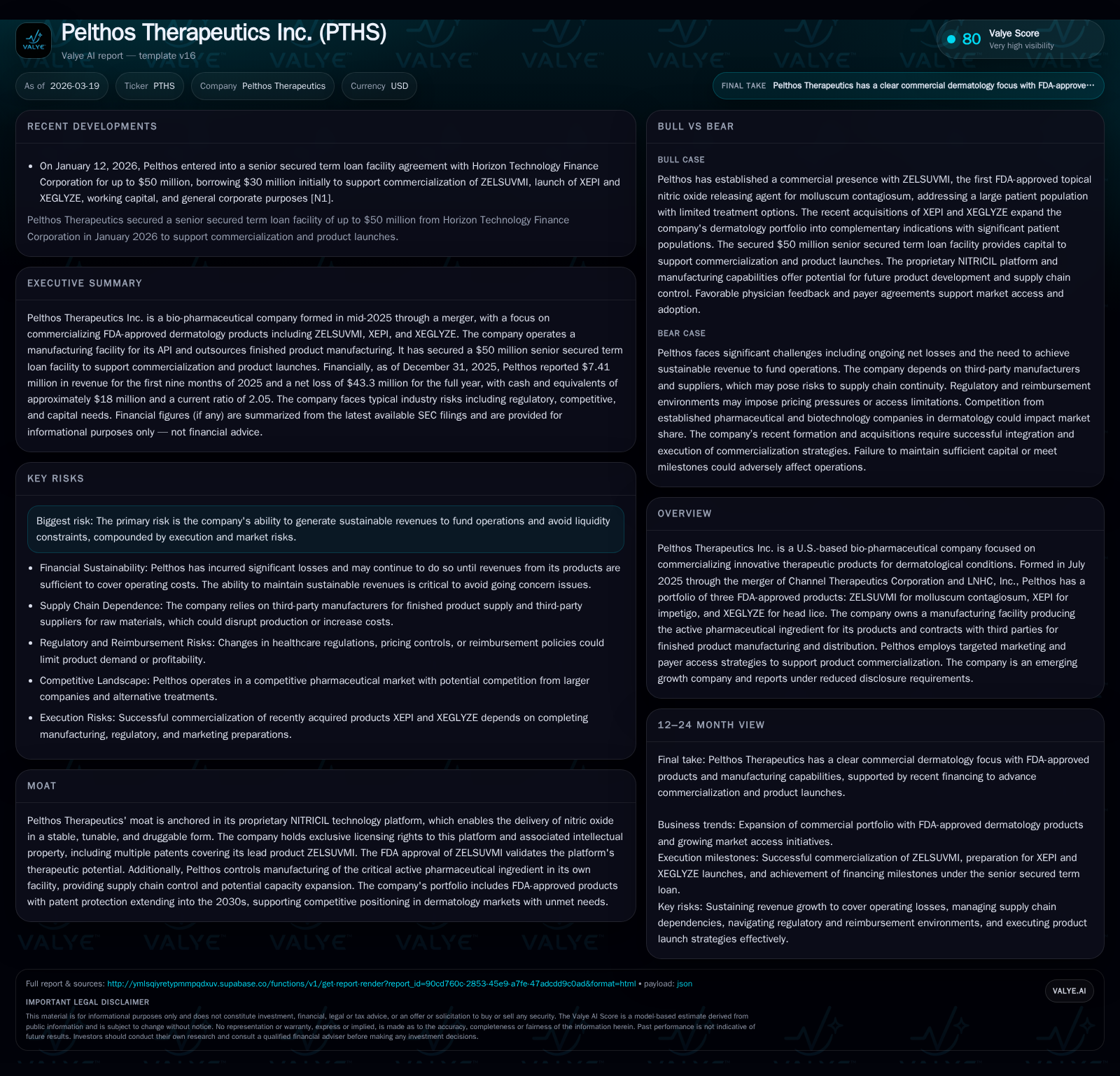

Pelthos Therapeutics Inc., established in mid-2025 through the merger of Channel Therapeutics and LNHC, markets three FDA-approved dermatology products anchored by its proprietary NITRICIL nitric oxide platform. Despite launching ZELSUVMI for molluscum contagiosum and expanding its portfolio with XEPI and XEGLYZE, Pelthos reported a net loss of $43.3 million in 2025, reflecting substantial commercialization costs amid early-stage sales. The company maintains a manufacturing facility for active pharmaceutical ingredients and secured a $50 million senior secured term loan facility in January 2026 to support ongoing commercial activities and product launches. Regulatory and reimbursement complexities, alongside execution risks, underscore the need for sustained revenue growth and capital access to achieve financial sustainability [S1][S4][F1].

Company Background

Pelthos Therapeutics Inc. was created through the July 2025 merger of Channel Therapeutics Corporation and LNHC, Inc., consolidating an FDA-approved dermatology product portfolio alongside manufacturing capabilities and research programs targeting sodium ion-channel NaV1.7 for pain therapy [S1]. The merged entity inherited commercial products including ZELSUVMI for molluscum contagiosum, as well as two additional FDA-approved products acquired later in 2025: XEPI (impetigo) and XEGLYZE (head lice) [S1].

Proprietary Technology Platform

Central to Pelthos’ offering is the NITRICIL technology platform—a proprietary nitric oxide delivery system enabling stable topical formulations. This platform is protected by worldwide licenses and patents extending into the 2030s, providing a meaningful competitive advantage within specialized dermatology markets characterized by unmet treatment needs [S1].

Financial Performance Overview

Pelthos recorded $16.2 million in net revenue for full-year 2025, reflecting approximately six months of commercial sales for ZELSUVMI post-launch. However, commercialization efforts drove total operating expenses to $49.2 million during the period resulting in a net loss of $43.3 million [S1][F1]. Operating cash flow was negative at approximately $22.6 million.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -43 | -23 | -32 | -444.5% |

| 2024 | -8 | -6 | -8 | -7.8% |

| 2023 | -7 | -1 | -7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 0 | -111.4 |

| 2024 | 75000 | 293.1 |

| 2023 | 114.5 |

Source: SEC companyfacts cache [F1].

The company’s current ratio stood at approximately 2.05x at year-end 2025 indicating short-term liquidity adequacy despite ongoing losses [F1].

Growth Outlook

Near-term growth drivers include expanding market penetration for ZELSUVMI beyond initial launch months through enhanced payer access programs and marketing initiatives targeting affected pediatric and adult populations [S1]. The addition of XEPI and XEGLYZE to the commercial portfolio presents further revenue opportunities contingent on successful market launches.

Longer-term prospects rest on advancing clinical-stage programs focused on NaV1.7 sodium ion-channel blockers pending regulatory milestones.

Capital Structure and Liquidity

To support ongoing operations amid significant cash burn rates associated with commercialization infrastructure build-out and product launches:

- In November 2025 Pelthos issued convertible notes providing growth capital.

- On January 12, 2026 the company entered into a Venture Loan & Security Agreement with Horizon Technology Finance Corporation securing up to $50 million in senior secured term loans; an initial drawdown of $30 million was made to fund commercialization activities including preparation for newly acquired product launches [S4].

Management believes available capital combined with projected revenues provides sufficient runway through at least the next twelve months post-filing [S4][F1].

Returns and Capital Allocation Policy

Pelthos has not generated positive returns or free cash flow given its early commercial stage; net losses translate into an approximate negative return on equity around -111% based on latest annual figures [F1]. No dividends have been declared nor significant share repurchases conducted—capital deployment prioritizes product development, commercialization expansion efforts, regulatory compliance initiatives and intellectual property maintenance [F1][S4].

Regulatory Environment and Risks

The company faces material risks including pricing pressures from government payors such as Medicaid rebate obligations under the Medicaid Drug Rebate Program as well as compliance with complex healthcare laws covering anti-kickback statutes and privacy regulations like HIPAA [S15][S16][S17][S13]. These factors could materially impact financial results if not managed carefully.

Drug pricing scrutiny at federal and state levels alongside evolving reimbursement policies may constrain pricing flexibility limiting revenue visibility.[S15][S16]

Legal Proceedings

There are no current material legal proceedings adversely affecting Pelthos’s business operations. Legacy litigation related to predecessor companies exists but has not resulted in material adverse outcomes to date [S1].

Conclusion

Pelthos Therapeutics operates as an emerging biopharmaceutical company focused on niche dermatological indications supported by its proprietary NITRICIL nitric oxide delivery platform protected by patents extending into the next decade. While initial commercial efforts have generated modest revenue streams since mid-2025 launch of ZELSUVMI alongside acquisitions expanding its product portfolio, the company continues to incur substantial operating losses reflecting investments required to establish market presence.

Capital raised through convertible notes and secured debt facilities underpin near-term liquidity although sustainable profitability depends critically on scaling revenues sufficiently to offset fixed costs inherent in commercialization infrastructure.

Regulatory compliance complexities coupled with evolving payer landscapes represent significant challenges that require continued management focus. Overall, Pelthos exemplifies a specialist bio-pharmaceutical venture navigating the transition from approval to commercial scale within dermatology leveraging differentiated technology platforms.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments