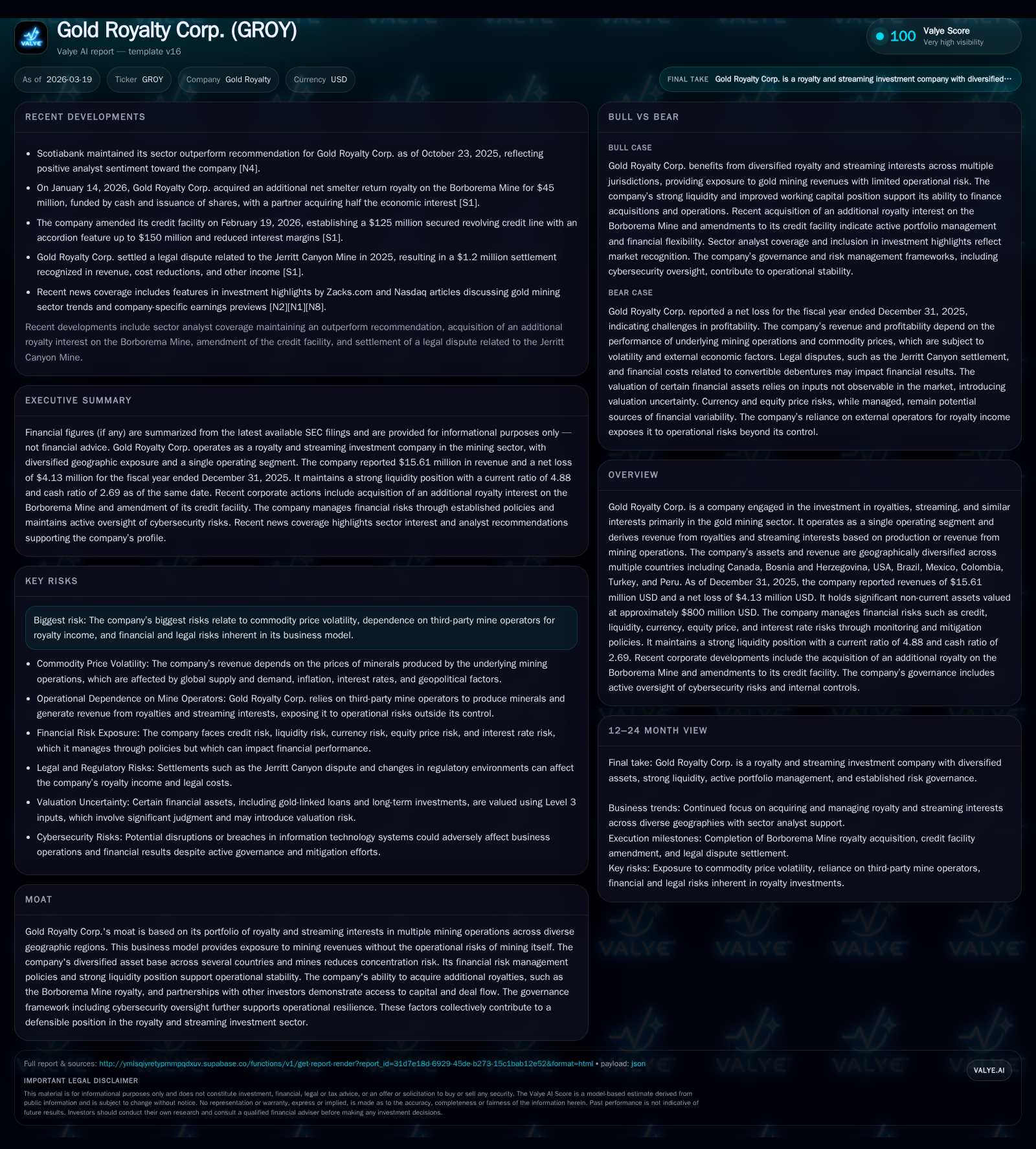

Gold Royalty Corp.’s Growing Portfolio Offsets Ongoing Profitability Challenges

Gold Royalty Corp. has substantially increased its revenue through a diversified royalty portfolio, even as net losses persist due to operating costs and finance expenses.

Gold Royalty Corp. operates a gold-focused royalty and streaming business model, capturing revenues derived from multiple geographically diverse mining operations without direct mining risks. The company’s annual revenue surged from $0.58 million in 2022 to $15.61 million in 2025, fueled by strategic acquisitions such as the Borborema Mine royalty. Despite this top-line growth, GROY has continued to report net losses—$4.13 million in 2025—driven by significant administrative expenses, share-based compensation, and accretion on convertible debentures. Its strong liquidity position, with a current ratio of nearly 4.9, supports operational stability while maintaining prudent capital allocation including steady dividends. Going forward, its amended credit facility and partnerships position it for measured growth while risk management—including cybersecurity oversight—remains a priority.

Revenue Growth Trajectory and Drivers Behind Expanding Asset Base

Gold Royalty Corp.’s revenue trajectory evidences robust expansion from a modest base of $582K in 2022 to an impressive $15.61 million in 2025 [F1]. This nearly 27-fold increase unfolded through both organic royalty income growth across existing streams and marked acquisition activity.

The company’s geographic diversification strategy contributes notably to this performance: revenue sources span Canada (dominant contributor at $5.44M in 2025), Bosnia and Herzegovina ($3.22M), USA ($1.97M), Brazil ($3.63M), Mexico ($1.35M), as well as Colombia, Turkey, and Peru [S14]. This dispersion mitigates concentration risk typical of royalty businesses dependent on limited operators or jurisdictions.

A significant portfolio driver includes the recent addition of the Borborema Mine royalty acquired in early 2026 under an agreement involving $45 million consideration split between cash and shares [S4]. The inclusion of this asset is expected to further fuel top-line growth beyond the latest reported fiscal year.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 16 | -4 | +54.5% | -21.1% |

| 2024 | 10 | -3 | +231.5% | +87.3% |

| 2023 | 3 | -27 | +423.7% | -1114.0% |

| 2022 | 1 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 3 | -0.6 |

| 2024 | 3 | -0.6 |

| 2023 | 3 | -5.1 |

| 2022 | 1 | -0.4 |

Source: SEC companyfacts cache [F1].

Revenue surged particularly between FY22-23 and FY23-24 driven by expansion of streaming interests and new royalties added.

Navigating Persistent Net Losses: Cost Structure and Operational Impacts

Despite rising revenues, Gold Royalty Corp.’s earnings remain negative with net losses narrowing from -$26.76 million in 2023 to -$4.13 million in 2025 [F1]. This trend reflects the interplay of operational expenses and finance charges that offset top-line gains.

General and administrative expenses include salaries ($2.46M in 2025), professional fees (some recoverable via settlements), and non-cash share-based compensation around $2M annually reclassified for clarity [S1][S14]. Finance costs driven by interest on bank loans ($2.38M), convertible debenture interest ($3.82M), plus accretion ($2.05M) present a notable drag on profitability [S7].

The settlement of the Jerritt Canyon dispute contributed additional revenue recognition alongside reductions in G&A expenses through professional fee recoveries—demonstrating embedded cost offsets within legal settlements [S4]. However, these gains have not fully neutralized finance-related expenses.

Return on equity remains negative near -0.6%, consistent with ongoing net losses relative to substantial equity valued at approximately $699 million at year-end 2025 [F1], underscoring challenges turning asset base into net income despite premium royalty holdings.

Diverse Geographic Royalty Interests Adding Stability Amid Mining Volatility

GROY’s portfolio spans multiple countries including established mining jurisdictions like Canada and the USA alongside emerging markets such as Bosnia and Herzegovina and Brazil [S14]. Geographic diversification reduces concentration risk common in royalty businesses reliant on few operators or regions.

By collecting royalties or streaming proceeds based on production or revenue metrics rather than engaging directly in mining operations, GROY reduces exposure to capital expenditure volatility while maintaining leverage to gold price fundamentals—a hallmark characteristic attractive to investors [N1].

This structure effectively mitigates counterparty risk inherent when depending heavily on limited mines or operators.

Future Growth Potential Through Strategic Acquisition and Partnership Pipeline

Following its pattern of acquiring strategic royalties such as the Borborema Mine NSR interest announced in early 2026 for $45 million consideration, Gold Royalty Corp. demonstrates confidence in its deal flow pipeline supported by partnerships like Taurus Mining Royalty Fund which intends to acquire half of the additional royalty interest [S4][N1].

These alliances enhance purchasing power while distributing investment risk across parties enabling access to high-quality assets otherwise capital intensive.

The recent amendment of the revolving credit facility expands borrowing capacity to $125 million plus a $25 million accordion feature under competitive SOFR-linked interest rates providing flexible financing for future acquisitions [S4][S5].

Organic growth prospects remain linked to production increases at underlying mines and gold price dynamics critical for forecasting royalty income streams.

Capital Structure Update: Credit Facility Enhancements and Leverage Profile

Gold Royalty Corp.'s liquidity remains robust supporting operational flexibility amid profit volatility. The amended secured revolving credit facility offers a base availability of $125 million plus a $25 million accordion option; maturity terms remain unchanged; interest margins reduced by approximately 25 basis points reflecting proactive debt cost management aligned with market conditions [S4].

As of December 31, 2025, current assets approximated $22.55 million against current liabilities near $4.62 million yielding a strong current ratio of 4.88—a liquidity metric uncommon among mid-tier royalty companies [F1].

This financial cushion provides resilience against commodity price fluctuations or timing gaps in cash flows while sustaining investment capacity for accretive royalties.

Capital Allocation Focus: Dividends and Return Metrics

Notably, Gold Royalty Corp has maintained consistent dividend payments totaling roughly $2.6 million annually despite operating losses over recent years reflecting disciplined capital stewardship prioritizing shareholder returns [F1][S11].

No share repurchase activity has been reported indicating emphasis on preserving cash reserves over equity buybacks given cash flow constraints [S12].

Trailing return on equity near -0.6% aligns with net loss patterns relative to sizable equity base suggesting room for operational improvements though shareholder value is currently supported more through yield than capital gains.

Robust Risk Management Encompassing Financial and Cybersecurity Exposures

Risk management extends beyond commodity price volatility encompassing credit risk related to banking counterparties; liquidity monitoring ensuring funding adequacy; minimal foreign currency hedging due to low currency exposures; equity price risks tied mainly to short-term investments; plus interest rate sensitivity related to debt instruments—all governed under comprehensive policies reviewed by management committees [S5].

Cybersecurity governance is led by the Audit Committee overseeing implementation of detailed Cybersecurity Policy frameworks addressing information security threats via regular assessments, employee training programs, incident response procedures coordinated with third-party IT experts [S13][S16].

These measures align with industry best practices safeguarding digital assets within global operator networks.

Key Milestones To Monitor: Production Trends, Legal Outcomes And Acquisition Activity

Investors should monitor integration timelines for recent acquisitions like Borborema impacting near-term cash flows; ongoing production reports from operators such as Jerritt Canyon following dispute settlement affecting per ton payments; utilization metrics of amended credit facility reflecting financial flexibility; alongside any litigation or regulatory developments influencing contract enforceability or jurisdictional risks [N1][S3][S4][S2].

Tracking production volume growth supporting royalty calculations will be pivotal for projecting sustainable revenue amidst commodity price variability.

Disclaimer: This document is an informational synthesis prepared without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments