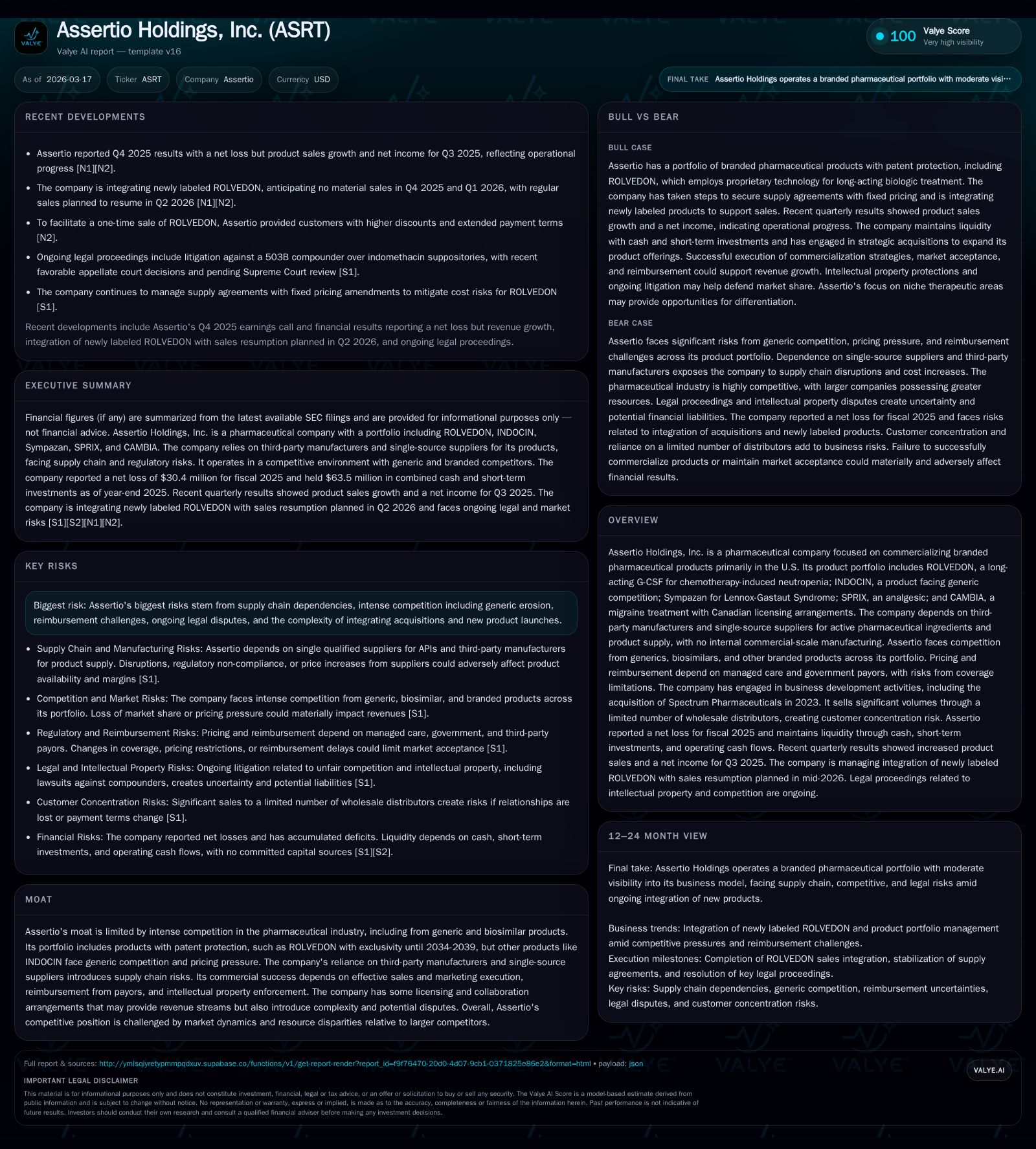

Assertio Holdings Battles Patent Pressures and Supply Risks to Stabilize Growth

Assertio’s financial recovery balances the commercial promise of ROLVEDON exclusivity against significant generic erosion and supply chain vulnerabilities.

Assertio Holdings has faced a volatile financial trajectory from FY2022 to FY2025, driven largely by the transition from legacy products like INDOCIN under generic pressure to the commercialization of the long-acting G-CSF, ROLVEDON, which holds exclusivity through 2034-2039. Despite progress, the company endures sustained operating losses and cash flow declines amid challenges including managed care reimbursement hurdles, reliance on third-party manufacturing, and ongoing legal disputes. Future growth depends on successful execution in payor negotiations, regulatory milestones, and stable supply chains, while capital allocation reflects heightened leverage risk and absent shareholder returns. Legal and regulatory complexities further cloud Assertio’s operating environment as it strives to stabilize and scale revenues.

Turning Points: Historical Financial Performance and Key Drivers

Assertio Holdings' financial performance over the past four fiscal years paints a picture of sharp volatility shaped by both internal portfolio shifts and external market pressures. Operating income—positive at $39.4 million in FY2022 [F1]—collapsed dramatically to an operating loss of $243.5 million in FY2023 as generic erosion especially impacted legacy product INDOCIN, coinciding with restructuring costs linked to integration activities [S1]. This loss narrowed substantially to -$24.5 million in FY2024 before improving further to -$21.5 million in FY2025 [F1], reflecting progress in commercializing ROLVEDON.

Net income trends closely followed operating results, showing a profitable $109.6 million in FY2022 [F1], plunging into a -$331.9 million loss in FY2023, primarily driven by impairment charges tied to intangible assets and portfolio rationalization [S19]. By 2025, net losses narrowed but remained materially negative at -$30.4 million [F1], highlighting ongoing earnings pressure.

Operating cash flows tell a cautionary tale: although robust positive CFO was reported through 2023 ($49.6 million) and into 2024 ($26.4 million), the company suffered a steep reversal reaching -$28.2 million by year-end 2025 [F1]. Capital expenditures were negligible recently ($0 in FY2024), consistent with Assertio’s lack of internal manufacturing investment [F1], underscoring operational cost control amid strained profitability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -30 | -28 | -22 | -40.7% | |

| 2024 | -22 | 26 | -24 | 0 | +93.5% |

| 2023 | -332 | 50 | -244 | 628000 | -402.8% |

| 2022 | 110 | 79 | 39 | 274000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -32.3 | |

| 2024 | 26 | -17.8 |

| 2023 | 49 | -240.5 |

| 2022 | 78 | 48.6 |

Source: SEC companyfacts cache [F1].

This table encapsulates Assertio’s volatile trajectory from profitability toward sustained losses driven by key operational factors including intensified generic competition against INDOCIN and the phased launch of ROLVEDON.

Product Portfolio Under Pressure: Patent Dynamics and Generic Competition

Assertio’s competitive moat is modest given fierce pharmaceutical industry headwinds marked by commoditization risks for legacy products alongside emergent branded exclusivity pockets. The crown jewel of its portfolio is ROLVEDON, a long-acting granulocyte colony-stimulating factor (G-CSF) designed for chemotherapy-induced neutropenia, which retains market exclusivity extended through 2034-2039 thanks to robust patent protection [S1]. This exclusivity window positions ROLVEDON as the primary long-term growth lever providing differentiated pharmacokinetic properties supporting clinical use cases like same-day dosing trials under professional guideline consideration.

Conversely, INDOCIN faces severe generic encroachment with multiple entrants eroding pricing power amidst commoditized NSAID markets [N1][S25]. Other offerings such as Sympazan (for Lennox-Gastaut Syndrome), SPRIX (analgesic), and CAMBIA (migraine treatment with Canadian licensing arrangements) contribute incremental revenue streams but are subject to biosimilar challenges or geographic limitation that restrict scale [S1]. The industry context of aggressive formulary management by payors intensifies pricing pressures across therapeutic classes.

Assertio’s dependence on third-party manufacturers for active pharmaceutical ingredients and final dosage forms magnifies supply chain risk exposure absent internal production capacity—a vulnerability particularly acute given single-source suppliers [S1]. Combined with portfolio patent lifecycles, this constrains Assertio’s pricing power while requiring vigilant IP enforcement amid potential infringement claims.

Future Market Opportunities and Commercial Execution Challenges

Looking forward, Assertio’s near-term revenue prospects hinge critically on several intertwined factors:

Managed Care Reimbursement: Success depends heavily on securing favorable formulary placements within managed care frameworks buttressed by adequate reimbursement levels—conditions complicated by accelerating cost containment policies such as Medicare price negotiations under IRA provisions [S6][S20].

Clinical Guideline Adoption: Recognition of ROLVEDON's same-day dosing efficacy within National Comprehensive Cancer Network guidelines would substantively augment prescriber confidence and catalyze broader patient uptake [S1][N1].

Supply Chain Reliability: Consistent product availability relies on partners’ ability to meet manufacturing timelines without disruption or quality issues given lack of internal fabrication infrastructure [S1].

Sales & Marketing Execution: Maintaining specialized sales force effectiveness targeting clinics and hospitals is essential for converting clinical differentiation into sustainable market share gains [S1].

These conditions collectively define Assertio’s commercial execution landscape where missteps can stall growth or erode volume, particularly given intense competition from established biosimilars or generics.

Critical Milestones Ahead: Regulatory, Reimbursement, and Sales Targets

While explicit guidance on upcoming milestones remains limited, several watch points emerge per recent filings:

The anticipated publication or revision of National Comprehensive Cancer Network guidelines incorporating data from ROLVEDON same-day dosing trials represents an inflection point influencing clinician prescribing behavior [S1][N1]. Such endorsement could mitigate current reimbursement hurdles and accelerate volume growth.

Managed care contracting cycles through mid-to-late 2026 will test Assertio’s ability to defend or enhance coverage terms amid evolving rebate arrangements mandated under new Medicare demonstration models such as GLOBE/ GUARD frameworks [S20].

Monitoring supply chain continuity as partners scale production capability remains crucial given integration complexities flagged post-acquisitions [S8][S12].

Absent concrete forward-looking metrics disclosed publicly, these represent thematic catalysts for potential inflection points shaping Assertio's revenue momentum.

Capital Allocation in Focus: Debt Structure, Cash Flow, and Shareholder Returns

Assertio carries notable financial leverage with $40 million principal outstanding under its 6.5% Convertible Senior Notes maturing September 1, 2027 [S4][S9][F1]. Interest payments occur semiannually with embedded covenants restricting asset pledges or subsidiary guarantees absent pari passu security provision [S9][S27].

Liquidity is constrained by persistent negative free cash flow; operating cash flow dropped sharply into negative territory at -$28.2 million in FY2025 compared to positive inflows of $26.4 million the prior year [F1], while capital expenditures have been minimal reflecting limited investment scope.

Equity declined sequentially over this period from $225.7 million in FY2022 down to just under $94 million by year-end 2025 illustrating impaired balance sheet strength compounded by cumulative net losses (-$30.4 million in FY2025) resulting in an approximate negative return on equity of -32% for the latest annual period computed as net income divided by equity value at year-end [F1].

No dividends or share repurchase programs have been initiated owing to prioritization of restructuring efforts and liquidity preservation [N1][S19]. Refinancing risk persists given tight covenant structures combined with earnings uncertainty—potential refinancing would be sensitive to capital markets conditions.

Legal Battles and Regulatory Risks Influencing Business Strategy

Company disclosures enumerate multiple ongoing legal proceedings encompassing shareholder securities class actions related to Spectrum Pharmaceuticals acquisition integration challenges as well as patent infringement litigation that threaten revenue stability through delayed commercialization or royalty losses [S7][S13][S15].

Regulatory risks extend into compliance uncertainties surrounding off-label marketing restrictions; failure here could attract significant fines or injunctive relief impacting reputational standing and operational focus [S10]. Furthermore, government efforts towards drug pricing reforms including Inflation Reduction Act provisions introduce unpredictability into pricing scenarios with possible additional rebates under Medicare demonstration programs slated for introduction through coming years [S20].

Moreover, complex collaboration agreements underpinning licensing deals raise dispute risks potentially delaying commercialization timelines or diluting contractual revenue share estimates if contested vigorously [S25]. These multifaceted legal/regulatory headwinds require vigilant risk management aligned tightly with strategic planning.

Disclaimer: This analysis is based solely on currently available public filings and news sources; it does not constitute investment advice or recommendations regarding Assertio Holdings or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments