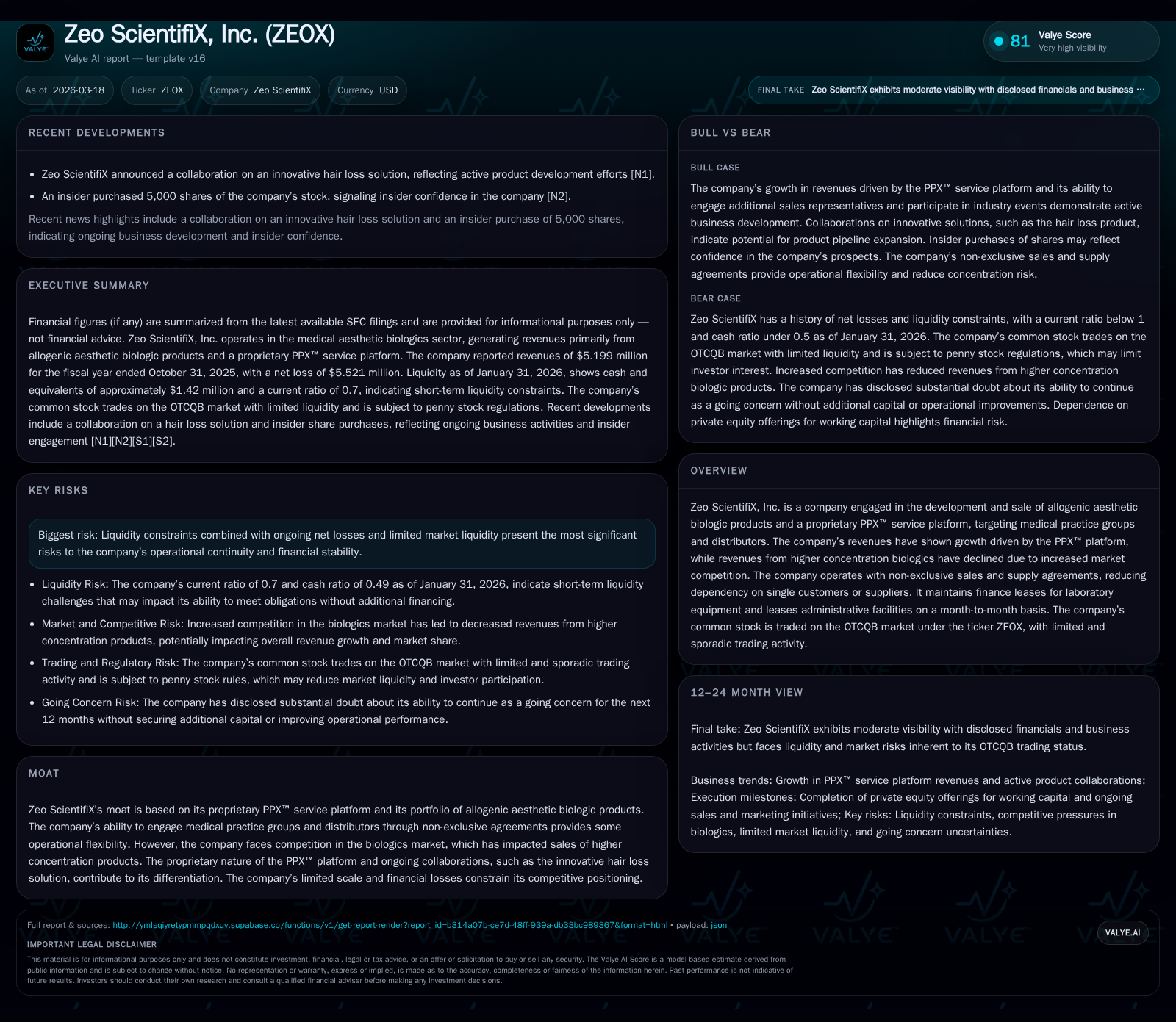

Zeo ScientifiX Emerges from Struggles with PPX™ Platform Growth and Market Challenges

Zeo ScientifiX’s revenue growth is increasingly propelled by its proprietary PPX™ platform, even as biologic product sales face competitive pressures and liquidity constraints persist.

Despite consistent net losses and liquidity challenges, Zeo ScientifiX reported a 12.5% revenue increase in FY2024 driven primarily by strong growth in its PPX™ service platform. This growth contrasts with declines in higher concentration allogenic biologics amid intensifying market competition. The company’s collaboration on innovative hair loss treatments highlights diversification efforts. However, ongoing operating cash flow deficits, reliance on capital raises, and a precarious working capital position highlight substantial risks to financial stability.

Historical Growth Patterns: Revenue Shifts and Underlying Drivers

Over recent years, Zeo ScientifiX has experienced significant shifts in its revenue composition against a backdrop of persistent operating losses. The fiscal year ended October 31, 2025 (FY2024) saw total revenue increase by approximately 12.5% to $5.2 million from $4.62 million in FY2023 [F1][S1]. This topline improvement was driven largely by the continued expansion of the company's proprietary PPX™ service platform, which generated $1.53 million in revenues for FY2024—more than doubling the $614,000 recorded in FY2023 [S1].

Contrasting this growth was a decline in revenues from higher concentration allogenic aesthetic biologic products which fell roughly 5.4%, from $2.42 million to $2.17 million over the same period [S1]. Unit sales of these premium biologics dropped significantly by over one-third (-33%), indicating weak demand amid growing competitive pressure [S1]. Lower concentration biologics saw modest revenue gains but effectively remained flat at around $1.39 million—a narrow increase of just under 1% despite robust unit sales growth (+34%) [S1].

These dynamics illustrate a pronounced pivot in Zeo’s business mix towards its service platform as traditional biologics products battle pricing erosion and market share loss.

Historical Performance Summary: FY2021-FY2024

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2024 | 5 | -6 | -1 | -5 | +14.1% | +21.0% |

| 2023 | 5 | -7 | -2 | -7 | -29.8% | +21.5% |

| 2022 | 6 | -9 | -3 | -9 | +16.0% | +30.3% |

| 2021 | 6 | -13 | -3 | -13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2024 | -1 | 388.0 |

| 2023 | -2 | 563.0 |

| 2022 | -4 | -471.1 |

| 2021 | -3 | 478.6 |

Source: SEC companyfacts cache [F1].

*Note: FY2023 YoY reflects sharp prior-year contraction from elevated FY2022 revenues [F1]

Dissecting Product Segments: Allogenic Biologics versus PPX™ Platform Dynamics

Breaking down the revenue streams reveals the strategic importance of Zeo’s proprietary PPX™ platform against legacy allogenic biologics offerings [S1]. The PPX™ platform accounted for close to 29% of total revenues in FY2024—a significant share enabling the company to offset declines in higher concentration biologic sales.

While higher concentration biologics contributed $2.17 million (about 42%), their value has eroded due to pricing pressures and slowing unit volumes as competitors offer more cost-effective alternatives [S1]. Conversely, lower concentration biologics maintained stable dollar revenues ($1.39 million) supported by strong volume growth (+34%), indicative of market migration toward more affordable products [S1].

These trends underscore Zeo's pivot away from premium biologic units toward services that promise better scalability and less commoditization risk.

Competitive Landscape and Its Impact on Product Sales

The allogenic aesthetic biologics market is becoming increasingly crowded with entrants competing aggressively on price points, eroding incumbents’ traditional margins and volume bases [S1]. Zeo specifically cites intensified competition leading to diminished demand for its higher priced biologics while attracting purchasers towards lower-cost alternatives within its portfolio.

This shift challenges Zeo’s ability to sustain margin-rich sales through legacy offerings but also emphasizes the criticality of expanding differentiated platforms such as PPX™, whose technological novelty and service orientation may provide more defensible economic moats.

Innovation and Recent Initiatives: The Hair Loss Collaboration

In March 2026, Zeo announced a promising collaboration focused on developing novel solutions for hair loss leveraging its proprietary PPX™ service technology [N1]. This partnership aims to diversify Zeo's growth pathways beyond the traditional aesthetics space into adjacent therapeutic areas with significant unmet demand.

Such initiatives symbolize ongoing efforts by management to strengthen the company’s innovation pipeline and reduce dependency on shrinking biologic product lines while exploiting unique technology advantages embedded within its platform.

Operational Challenges: Limited Scale, Losses, and Liquidity Constraints

Despite encouraging revenue developments from the PPX™ platform, Zeo faces substantial operational hurdles characterized by ongoing cash burn and scale limitations [F1][S6][S8]. For FY2024 alone:

- Operating income stood at a negative $5.39 million;

- Net losses totaled approximately $5.52 million;

- Operating cash flow remained negative at $718,000;

- Free cash flow was also negative at approximately $741,000 (operating cash flow minus capex) [F1].

Compounding financial stress is a strained liquidity profile evidenced by a working capital deficit nearing $1.9 million at fiscal year-end with a current ratio hovering around only 0.7 [F1]. Such metrics highlight severe short-term funding gaps necessitating continuous capital injections for operational continuity.

The trading activity for Zeo's common stock remains sporadic on the OTCQB market under ticker ZEOX which impairs equity fundraising prospects and heightens dilution risks when private placements are undertaken [S1]. Additionally, legal proceedings involving former executives may pose reputational or financial uncertainties though material impacts remain undetermined currently [S13].

Capital Allocation Review: Financings, Capex, and Returns Analysis

Recent capital allocation reveals heavy reliance on financing activities for survival rather than internal generation [F1][S6][S9][S27]. Notably:

- In November 2025 through January 2026 timeframe, Zeo raised approximately $1.2 million via private placements involving units comprising common shares and warrants exercisable up to late-2030 at an exercise price of $4 per share [S6].

- Capital expenditures were modest at around $23,000 dedicated primarily toward laboratory equipment purchases indicating limited scope for organic capacity expansion [F1][S22].

- No dividends or share repurchase programs were implemented given constrained cash flow and negative equity position (-$1.42 million) as of FY2024 end [F1][S9].

- Return metrics such as ROE are distorted due to negative equity base despite net losses; approximate calculation shows high distortion (+388%) underscoring financial strain rather than profitability [F1].

These factors collectively point towards capital allocation focused predominantly on maintaining operational runway amidst weak earnings performance.

Future Outlook: Potential Growth Catalysts and Key Risks to Monitor

Looking ahead: The growth trajectory depends heavily on successfully commercializing new developments like the hair loss collaboration utilizing PPX™ technologies alongside expanding sales efforts already underway via increased industry engagement and education programs [N1][S1]. Positive momentum here can potentially insulate Zeo against further erosion in traditional product lines.

Critical risks include persistent liquidity shortages that may force asset divestitures or restructuring absent sufficient external funding; heightened competition within allogenic biologics imposing continued downward pressure on pricing; unresolved legal matters which could impose unforeseen costs; regulatory compliance challenges related to FDA oversight of human tissue-based products; as well as inherent operational risks tied to small scale limiting economies of scope or scale efficiencies [S5][S15]. Monitoring quarterly cash burn rates alongside any shifts in regulatory landscape or competitive positioning will be essential gauges of viability.

This report synthesizes publicly available SEC filings along with recent news releases without speculation beyond stated evidence or explicit company disclosures. It aims to provide an analytical framework balancing innovation-focused developments against pressing financial realities confronting Zeo ScientifiX today.

--- DISCLAIMER --- This document is prepared solely for informational purposes regarding Zeo ScientifiX Inc., based on available data as of March/April 2026 and does not constitute investment advice or an offer to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments