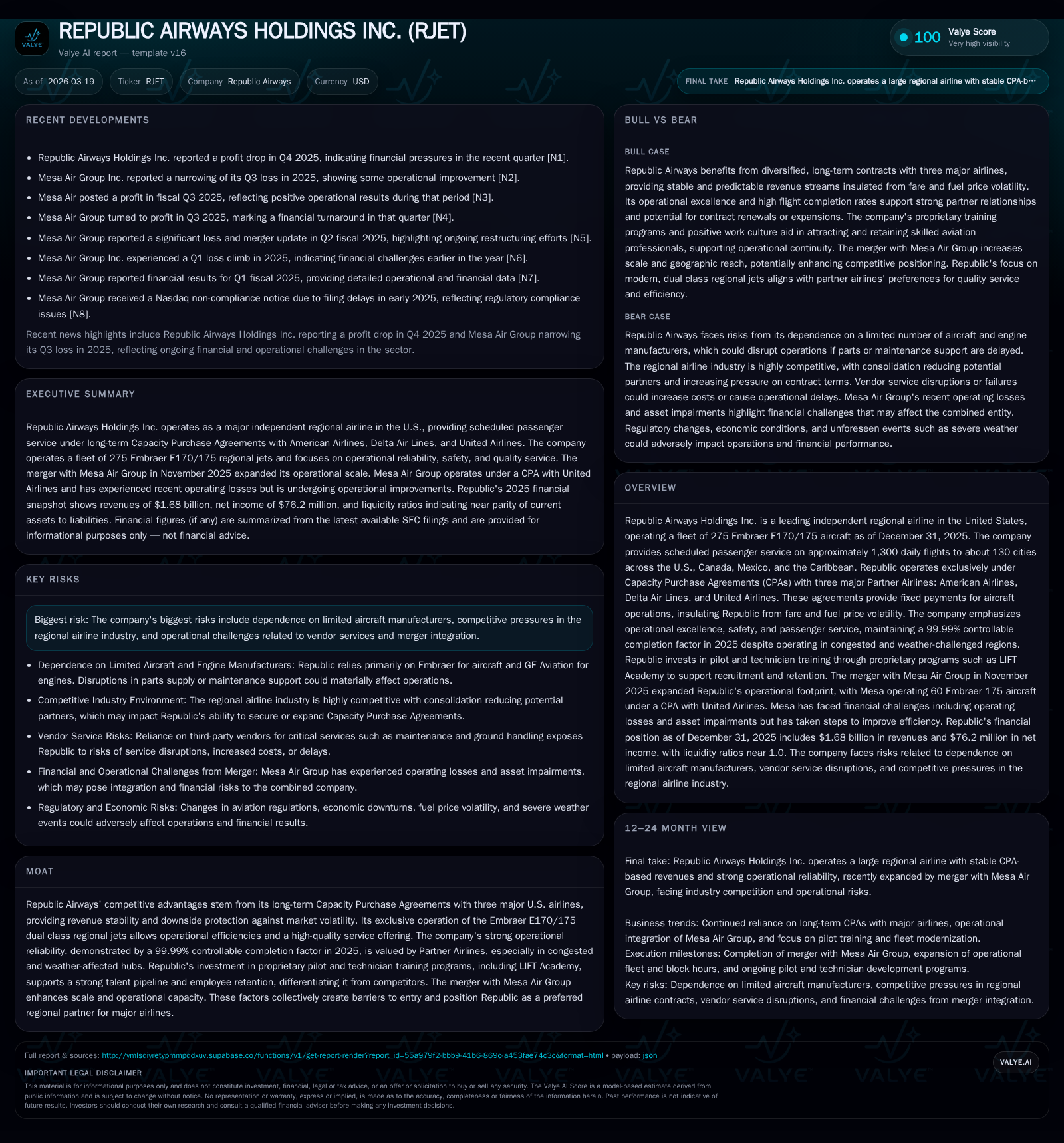

Republic Airways’ Recovery and Expansion Powered by Stable CPAs and Fleet Growth

Long-term contracts and expansion through merger underpin Republic Airways’ robust rebound and strategic positioning in regional aviation.

Republic Airways Holdings Inc. emerged from a challenging multi-year downturn in aviation with significant profitability and cash flow improvements in 2025, driven largely by fixed-fee Capacity Purchase Agreements (CPAs) with major U.S. airlines, a focused Embraer E170/175 fleet, and operational reliability. The company’s merger with Mesa Air Group is set to substantially increase operational scale and fleet utilization in 2026. While the airline benefits from revenue stability and operational excellence, industry risks such as dependence on limited manufacturers, integration challenges, and intense competition remain headwinds.

Historical Performance: Navigating Volatility and Achieving Profitability

Republic Airways faced sustained headwinds post-2022 as industry-wide turbulence pressured regional carriers. Operating losses mounted for several years, with net losses of $182.7M in 2022 tapering to $111.9M in 2024 before dramatically reversing to a net income of $76.2M in 2025 [F1]. Revenue climbed steadily from $1.474B in 2024 to $1.6765B in 2025—a near 14% improvement—reflecting higher flight activity aligned with recovering travel demand [F1]. Operating income swung positively by approximately $279M year over year to $168.3M in fiscal year 2025 [F1], signaling restored operational efficiency.

This performance was bolstered by Republic’s contractual model under Capacity Purchase Agreements (CPAs) that pay fixed fees per block hour flown rather than relying on passenger fares or load factors. This insulated the company from fare volatility and fuel price inflation which frequently distort traditional airline economics [S1][S8][S11]. Hence, revenue growth tracked network expansion more than market pricing changes.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 76 | 322 | 168 | +168.1% |

| 2024 | -112 | -12 | -111 | +6.8% |

| 2023 | -120 | -24 | -84 | +34.2% |

| 2022 | -183 | 13 | -190 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 5.7 |

| 2024 | 7866.8 |

| 2023 | -60.0 |

| 2022 | -59.3 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditures not explicitly itemized annually; buybacks minimal as per historical data [F1].

Growth Drivers and Strategic Positioning

Republic’s core strengths lie in its CPA-backed business model with three major U.S. airlines: American Airlines, Delta Air Lines, and United Airlines [S8][S11]. Each contract embeds minimum aircraft utilization commitments and payment terms extending into the late 2030s (notably United’s contracts), offering durable revenue visibility beyond typical aviation cycles [S11]. This diversification across multiple partners reduces single-customer risk.

The exclusive operation of an Embraer E170/E175 dual-class aircraft fleet totaling 275 planes as of December 31, 2025—the largest global operator of this type—adds an efficiency edge through standardized maintenance regimes and pilot training programs [S11][S18]. The reliance on this homogeneous fleet facilitates pilot scheduling flexibility across partner airlines' networks. Additionally, Republic maintained a near-perfect controlled completion factor of 99.99% for flights in 2025 despite operating hubs challenged by congestion and severe weather conditions regularly encountered within North America’s busiest airports [S18], underscoring operational excellence highly prized by the Partner Airlines.

The November 2025 merger with Mesa Air Group—another United Express contractor operating Embraer E175 jets—increased total operational scale significantly, increasing expected block hours by roughly a quarter in calendar year 2026 alone [S10][S2]. This consolidation aims to leverage cost synergies, expanded route access, improved aircraft utilization rates, and deeper talent pools while creating the second largest regional operator in the U.S.

Republic’s internal pilot development programs such as LIFT Academy are industry-leading initiatives designed to attract and retain skilled pilots—a critical advantage amid widespread pilot shortages constraining many regional operators' growth strategies [S18]. Such holistic commitment to career progression directly aligns with major carrier pipelines.

Financial Health: Liquidity, Capital Allocation & Leverage

Liquidity rebounded strongly throughout fiscal year 2025 with net cash from operations surging to $322 million compared to negative cash flow previously (-$11.6 million in FY24), reflecting healthier core operations boosted by contract revenues and better working capital management [F1][S7][S16]. Despite this improvement, free cash flow remains challenged due to ongoing capital expenditures necessary for fleet maintenance and upgrades; available data imply persistent negative free cash flow estimated around -$75 million after adjusting for capex-related outlays reported separately but not explicit annually [F1].

Total debt including finance leases stood around $1.1 billion at December 31, 2025—predominantly linked to aircraft acquisition financing—and remains a key leverage consideration within the capital-intensive airline sector [F1][S13]. The financial position benefited from loan amendment agreements associated with the Mesa merger that provided temporary relief on interest rates (dropping temporarily to zero percent), deferred maturities, debt forgiveness credits near $12 million, and security pledges enhancing lender confidence [S21]. Improving operational results help service debt amid elevated obligations but financial discipline will be crucial.

Capital return initiatives like share buybacks have been minimal or paused since prior years reflecting liquidity prioritization toward deleveraging and restructuring efforts post-merger integration; dividend payments are not specifically highlighted or disclosed recently [F1].

Risks and Challenges Ahead

Republic’s business model is heavily dependent on limited OEM relationships primarily Embraer (aircraft) and General Electric Aviation (engines) for fleet support continuity—a vulnerability if supply chain or quality issues arise or regulatory actions restrict usage of these aircraft types or components [S1][S29]. Renewed tariffs or trade policy shifts could exacerbate operating costs given substantial foreign equipment imports involved in fleet maintenance parts.

Competitive pressure within the US regional airline space remains keen—with other large incumbent operators partially owned or tightly integrated into major airlines sometimes enjoying preferential access or scale advantages; shifting contract allocations remain an ongoing negotiation dynamic influenced by scope clause limitations imposed by major airline labor agreements [S15][S22].

Risks related to third-party vendors providing critical maintenance services or infrastructure technology could lead to disruptions or increased costs if such suppliers fail financially or face unionization/legal/regulatory hurdles undermining reliability or bargaining power [S1][S29]. Additionally, air traffic control system risks including federal funding uncertainties pose systemic vulnerabilities potentially affecting schedules negatively.

Finally regulatory complexity imposed by DOT/FAA continues evolving around consumer protection mandates (like refund policies), safety oversight tightening post-pandemic industry recoveries, evolving labor force qualifications enhancements via FAA reauthorizations plus potential environmental compliance layers may increase costs unpredictably over time [S6][S12][S24].

Outlook: What to Monitor Going Forward?

While explicit guidance for future quarterly or annual financials was not disclosed recently, key indicators include:

- Integration progress post-Mesa merger driving realization of cost synergies versus one-off expenses related to combining operations,

- Contract renewal negotiations or expansions particularly if any partner airlines recalibrate their regional flying programs,

- Operational metrics such as flight completion ratios maintained despite expanded networks,

- Debt servicing capacity under fluctuating interest rate scenarios,

- Macro impacts related to fuel pricing indirectly transmitted via Partner Airlines’ flight scheduling,

- Labor market developments affecting pilot and technician retention amid industry-wide shortages,

- Regulatory changes impacting cost structures including tariffs or new airworthiness directives.

Republic Airways’ strategy hinges on leveraging its deep CPAs alongside its operational reliability reputation supported by a modern homogeneous jet fleet to maintain an indispensable role feeding major hubs nationwide—a vital piece of North American air travel connectivity that sustains both passenger choice diversity and logistics network density.

Disclaimer: This report is informational only and does not constitute investment advice or recommendations regarding Republic Airways Holdings Inc. It relies strictly on documented sources without speculative assumptions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments