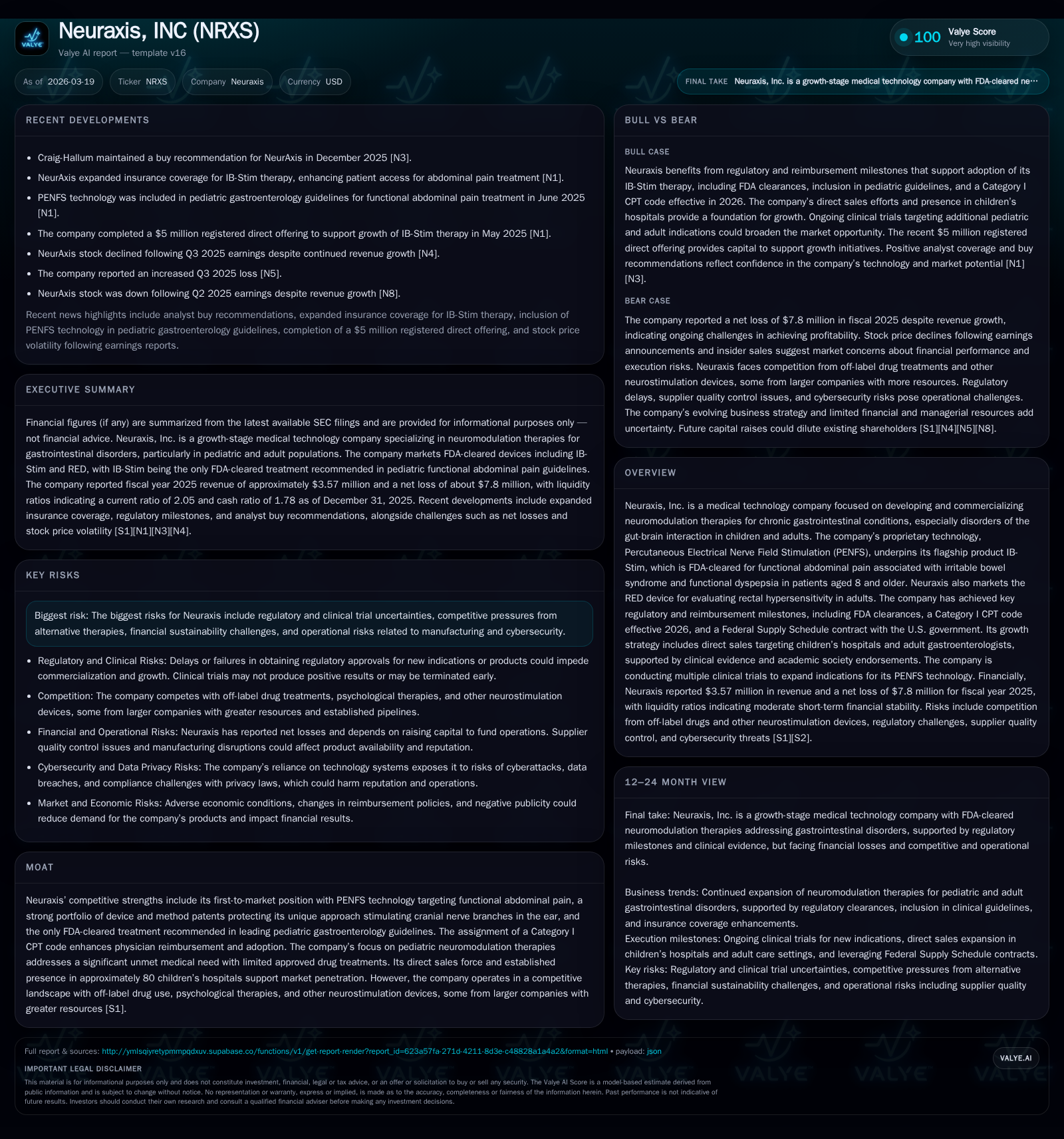

Neuraxis Drives Growth Through PENFS Innovation and Market Access Gains

Neuraxis advances as a pioneer in neuromodulation therapies for chronic gastrointestinal disorders, bolstered by regulatory milestones and focused commercialization amid ongoing financial challenges.

Neuraxis, Inc. demonstrated solid revenue growth with a 32.9% increase to $3.57 million in FY2025, driven primarily by sales of its IB-Stim and RED devices that utilize proprietary Percutaneous Electrical Nerve Field Stimulation (PENFS) technology. The company's competitive edge is supported by FDA clearance of PENFS treatment for functional abdominal pain, reinforced by a Category I CPT code assignment and inclusion in NASPGHAN pediatric guidelines, facilitating improved reimbursement and clinical adoption. Despite these commercial advances, Neuraxis continues to incur significant operating losses and negative cash flows reflecting ongoing research investments and commercialization costs. Key risks include regulatory scrutiny, intellectual property disputes, and reimbursement litigation which create near-term uncertainties. Growth prospects depend on expanded product indications, broader market penetration, and effective management of regulatory and legal challenges.

Historical Performance

Neuraxis has shown consistent growth in revenue over the past three years as it scales commercialization of its neuromodulation devices targeting gastrointestinal disorders. Revenue increased from approximately $2.46 million in FY2023 to $3.57 million in FY2025, representing a compound annual growth trajectory driven by sales of the IB-Stim device and complementary RED diagnostic product [F1]. Despite this top-line growth, the company incurred substantial operating losses which deepened from -$6.7 million in FY2023 to -$7.8 million in FY2025 due to continued investment in research & development and commercial expansion costs [F1], [S1]. Operating cash flows remained negative at -$6.4 million in FY2025 while capital expenditures stayed modest at roughly $31 thousand annually.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4 | -8 | -6 | -8 | +32.9% | +5.4% |

| 2024 | 3 | -8 | -6 | -7 | +9.2% | +43.7% |

| 2023 | 2 | -15 | -7 | -7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -229.5 |

| 2024 | -6 | -398.6 |

| 2023 | -7 | 1042.4 |

Source: SEC companyfacts cache [F1].

Neuraxis continues to invest ahead of profitability while expanding clinical adoption within targeted gastroenterology markets.

Product Portfolio and Technology

The company's core offering is IB-Stim®, an FDA-cleared Class II medical device utilizing proprietary Percutaneous Electrical Nerve Field Stimulation (PENFS) technology intended for patients aged eight years and older suffering from functional abdominal pain associated with irritable bowel syndrome (IBS) and functional dyspepsia (FD) [S1]. This technology modulates cranial nerve branches via percutaneously placed electrodes on the ear to provide non-pharmacological pain relief distinct from conventional drug or psychological therapies.

The RED™ device complements IB-Stim by providing diagnostic evaluation of rectal hypersensitivity—a relevant physiological marker in certain disorders of gut-brain interaction (DGBIs)—and is intended for use by trained healthcare providers in adult populations [S1]. Together these products address unmet clinical needs through evidence-based neuromodulation approaches.

Crucially, IB-Stim holds the unique distinction as the only FDA-cleared PENFS device recommended within the North American Society of Pediatric Gastroenterology Hepatology and Nutrition (NASPGHAN) functional abdominal pain guidelines published in May 2025—a critical validation enhancing prescriber confidence beyond regulatory clearance alone [S1].

Regulatory Milestones and Market Access

Significant regulatory achievements underpin Neuraxis’ commercial progress: notably the American Medical Association's assignment of a Category I Current Procedural Terminology (CPT) code (64567) specific to PENFS procedures in 2024 with effect from January 1, 2026 [S1]. This coding facilitates streamlined physician billing through recognized Relative Value Units (RVUs), incentivizing procedural adoption by compensating physician time.

Furthermore, Neuraxis secured a Federal Supply Schedule contract with the U.S. government in December 2025 enabling procurement of IB-Stim for its approved indications—strengthening institutional access channels [S1]. The company employs a direct sales approach targeting approximately eighty children’s hospitals alongside adult gastroenterologists specializing in DGBIs to enhance market penetration.

Financial Position and Capital Allocation

As of FY2025 year-end data shows cash and equivalents totaling approximately $4.97 million alongside current assets of about $5.73 million against current liabilities near $2.79 million yielding a current ratio of roughly 2.05x—indicating adequate short-term liquidity amidst ongoing operational losses [F1]. Equity improved significantly year-over-year reaching nearly $3.4 million compared to prior negative equity balances reflecting capital raises or retained earnings adjustments.

Operating cash flow remains negative at around -$6.43 million while capital expenditures have been minimal (~$31K annually), indicating focus on operational investment rather than asset expansion currently [F1]. Free cash flow approximates negative $6.46 million illustrating continued cash burn aligned with growth-stage dynamics.

Legal Proceedings and Risks

Neuraxis faces legal challenges primarily related to billing practices and intellectual property claims: a tentative settlement agreement was reached in April 2025 resolving prior litigation concerning alleged misrepresentations about billing the NeuroStim device under Medicare programs for $750 thousand payable over twelve months commencing January 2026 [S3], [S6], [S7]. However unresolved patent assertions pose ongoing legal uncertainties potentially impacting future operations.

Other key risks include dependence on maintaining FDA clearances amid regulatory oversight; reimbursement uncertainties tied to private and government payors influenced by evolving healthcare policies; potential adverse outcomes from product liability claims; compliance with extensive healthcare laws governing marketing practices; and possible impacts from data privacy regulations such as HIPAA and GDPR given sensitive health information handling obligations documented extensively in risk disclosures [S1], [S4]–[S19].

Outlook Considerations

Future growth hinges on successful expansion into additional therapeutic indications through ongoing clinical trials targeting pediatric and adult DGBI populations employing PENFS technology as well as geographic market expansions contingent upon regulatory clearances [S1]. Adoption acceleration is anticipated following implementation of the CPT code from January 2026 which lowers procedural billing barriers for physicians.

Investors should monitor trial outcomes that may broaden label claims alongside evolving reimbursement landscapes shaped by healthcare reform initiatives potentially affecting coverage levels or pricing pressures [S4]. Navigating regulatory compliance rigorously alongside managing ongoing legal exposures will be critical to sustaining commercial momentum.

Neuraxis represents a medical technology innovator balancing promising clinical differentiation and market access gains against persistent financial losses inherent to early-stage commercialization.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments