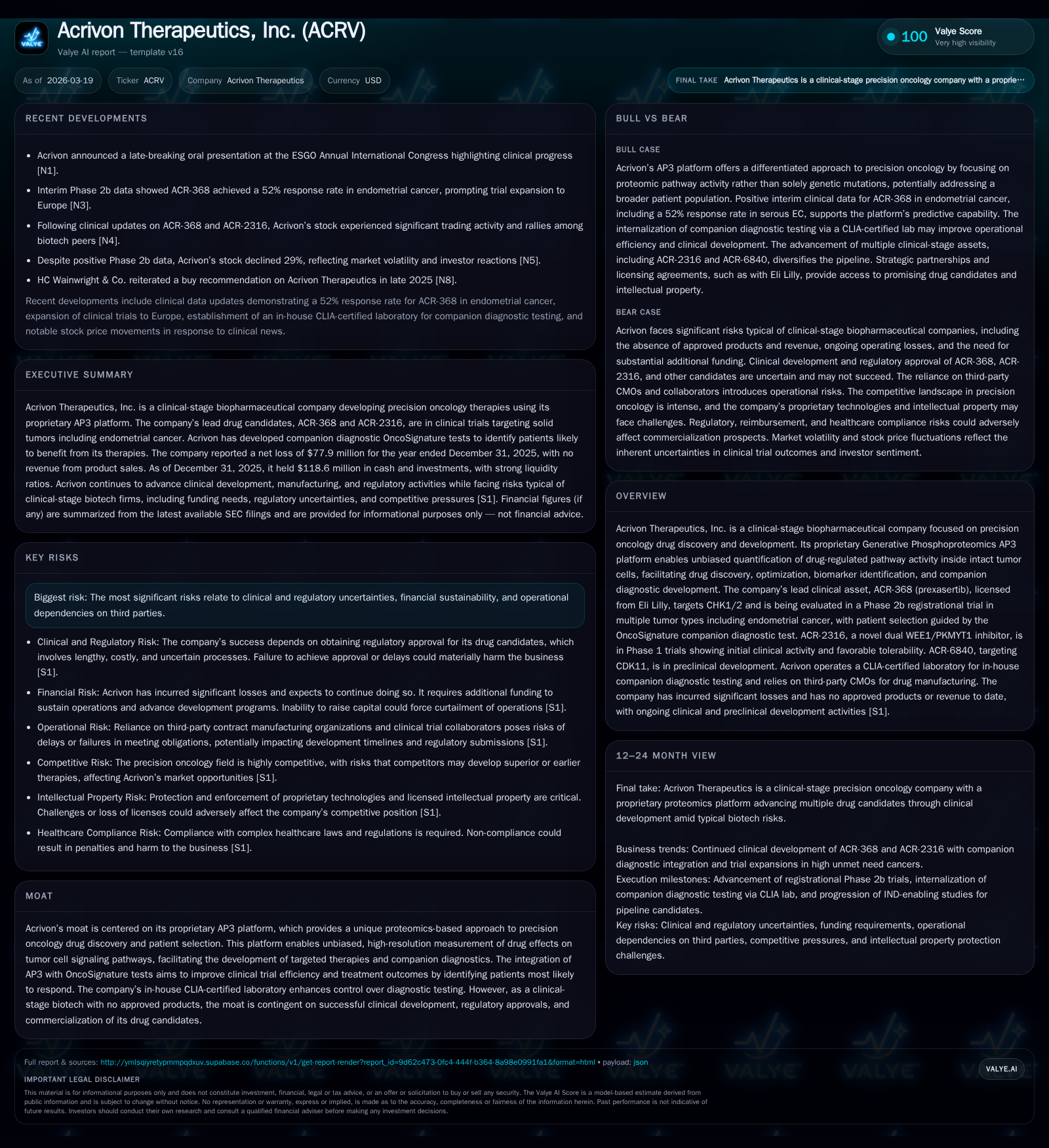

Capital Efficiency and Clinical Advances Define Acrivon Therapeutics’ Growth Prospects

Acrivon Therapeutics is leveraging its proprietary AP3 proteomics platform to advance precision oncology drugs amid ongoing clinical development and disciplined capital management.

Acrivon Therapeutics, a clinical-stage biotech, centers its drug discovery on the innovative AP3 phosphoproteomics platform, enabling pathway activity profiling within tumor cells for precision oncology. While it has sustained operating losses characteristic of its early development stage, the company shows disciplined cash management with a strong liquidity position as of year-end 2025. Clinical progress, particularly in the registrational Phase 2b trial of ACR-368 and Phase 1 activity of ACR-2316, underpins future value creation but is subject to regulatory and companion diagnostic approval risks. Monitoring upcoming trial data readouts and adequate funding rounds will be crucial for sustaining its developmental runway.

Unpacking Historical Financial Performance and Operating Dynamics

Acrivon Therapeutics’ financial trajectory between fiscal years 2022 and 2025 paints a vivid picture of a clinical-stage biopharmaceutical company focused heavily on R&D maturation ahead of commercialization. Operating losses deepened from -$32.7 million in FY2022 to -$84.1 million in FY2025 [F1], reflecting scaling clinical activities predominantly in oncology drug candidates. Net losses mirrored this trend with a near doubling over the same span from -$31.2 million to approximately -$77.9 million [F1]. These figures align with the outflow profile typical for companies yet to generate commercial revenue or achieve product approvals.

Operating cash flow exhibited consistent negative outflows ($-30.1M in FY2022 increasing to $-63.7M in FY2025) paralleling operational burn rates primarily due to escalating clinical trial expenditures and preclinical research efforts [F1]. In contrast, capital expenditures remained modest (around $1.7M in FY2025), indicating limited fixed asset investments relative to R&D spend, consistent with reliance on external manufacturing and laboratory services.

The company’s liquidity position presents a healthy buffer for continued development: as of December 31, 2025, cash and equivalents stood at $41.5 million against current liabilities of $15.7 million yielding a strong current ratio of roughly 7.7x [F1]. Such solvency suggests prudent cash stewardship amidst accelerated clinical activities yet underscores an imperative for ongoing capital raises given the negative free cash flow estimated at about $65 million [F1]. Equity declined between FY2024 and FY2025 reflecting cumulative deficits but remains supportive at over $112 million.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -78 | -64 | -84 | 2 | +3.3% |

| 2024 | -81 | -66 | -89 | 3 | -33.4% |

| 2023 | -60 | -43 | -67 | 1 | -93.8% |

| 2022 | -31 | -30 | -33 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -65 | -69.2 |

| 2024 | -68 | -45.6 |

| 2023 | -44 | -49.8 |

| 2022 | -32 | -18.3 |

Source: SEC companyfacts cache [F1].

Data reflects intensifying R&D investment dynamics typical for a pre-commercial biotech advancing multiple oncology candidates.

AP3 Platform: The Core Moat Driving Acrivon’s Precision Oncology Campaign

Central to Acrivon's strategic playbook is its proprietary Generative Phosphoproteomics AP3 platform that uniquely quantifies dynamic pathway activity inside intact tumor cells at high resolution [S1]. This enables unbiased measurement of phosphorylation states that govern key cancer signaling networks—an advancement beyond traditional genomics or bulk proteomics approaches.

This single-cell phosphoproteomic quantification allows detailed mapping of drug-induced effects on CHK1/2 or WEE1/PKMYT1 pathways targeted by their leading candidates (e.g., ACR-368 and ACR-2316). By integrating AP3-derived insights with OncoSignature companion diagnostics developed internally under CLIA certification [S18], the company pursues enhanced patient stratification accuracy increasing likelihood of clinical responders—a major value driver mitigating typical heterogeneity challenges in oncology trials.

In sector context terms: this proteomics-based pathway profiling expands precision beyond mutation presence towards functional modulation of cell cycle checkpoint kinases critical in DNA damage response—an area gaining momentum for synthetic lethality strategies with chemotherapy or PARP inhibitors.

Therefore, AP3 acts not only as an enabling R&D technology but also spells potential commercial synergy via co-development of requisite biomarkers facilitating regulatory submissions with contemporaneous companion diagnostic approvals [S18]. However, execution risk concentrates around ensuring regulatory alignment for test-drug co-approval pathways—mandatory under FDA guidelines for some therapies reliant on predictive diagnostics.

Clinical Milestones Centered on ACR-368 and ACR-2316: Progress and Challenges

Acrivon's lead clinical asset ACR-368 targets checkpoint kinases CHK1/2 integral to cell cycle control and DNA damage repair fidelity—exploiting vulnerabilities in cancers such as endometrial carcinoma where replication stress is high [N1][S1]. The ongoing registrational Phase 2b trial incorporates the OncoSignature companion diagnostic test enabling biomarker-guided patient selection aiming to enhance efficacy signals necessary for FDA accelerated approval pathways.

ACR-2316 is distinguished as a novel dual WEE1/PKMYT1 inhibitor currently assessed in Phase 1 studies [N1][S1]. Early data indicate initial clinical activity coupled with favorable tolerability profiles—a critical bottleneck often encountered by kinome-targeting agents requiring strict dose optimization due to hematologic toxicity risks characteristic of cell cycle checkpoint inhibitors.

These programs demonstrate strategic focus on kinase inhibitors modulating the DNA damage response axis—a therapeutic modality increasingly validated by regulatory successes in similar targets. Still challenging remains the inherent uncertainty around demonstrating sufficient benefit-risk balance amid competitive pipelines targeting overlapping mechanisms [S13][S19].

Regulatory complexity intensifies as approval depends not only on robust efficacy/safety endpoints but also parallel verification of companion diagnostic performance—a dependency elevating operational interlocks between drug and biomarker teams for coordinated submissions [S18]. Furthermore, any delay or denial in diagnostic clearance could stall drug commercialization regardless of intrinsic pharmacological merits.

Strategic Capital Deployment Amid Elevated R&D Investments

Financial evidence underscores how capital allocation priorities skew heavily toward research and clinical development expenditures necessary to propel pipeline assets through regulatory inflection points [F1][S2]. The company’s operating income loss widened minimally year-over-year by approximately 5.7%, indicating some stabilization even amid expanded trial activities.

No dividend distributions or share repurchase programs exist—consistent with biotech sector norms where preserving cash runway supersedes capital returns during high-risk development phases [F1]. Capital expenditure levels remain restrained below $3 million annually reflecting minimal investment in tangible property likely outsourcing manufacturing and laboratory analyses.

With free cash flow approximated at negative $65 million as of FY2025 end (operating cash flow less capex) [F1], sustained capital raising via equity or convertible securities remains essential given no revenue inflows to offset burn rate—also corroborated by management commentary forecasting ongoing needs to fund trials and regulatory milestones [S2]. ROE is deeply negative (~-69%), again reflecting investment-stage status without earnings generation.

Management’s stewardship appears calibrated toward balancing aggressive R&D momentum while safeguarding liquidity as reflected by a strong current ratio near 7.7x signifying ample short-term assets against liabilities as of year-end [F1]. However sustained access to financing markets remains critical depending on upcoming data catalysts that may influence investor appetite.

Regulatory Landscape and Companion Diagnostic Interdependency Risks

Navigating USFDA approval pathways involves multilayered regulatory hurdles encompassing both investigational new drug applications progressing through phased trials plus complex requirements governing In Vitro Diagnostics when deployed as companion tests [S18][S24]. For Acrivon's lead candidates relying on OncoSignature diagnostics co-approval constitutes a synchronous milestone imposing additional procedural timing risks.

Compounding this are compliance obligations under multiple healthcare statutes such as anti-kickback laws and false claims statutes impacting marketing/sales practices post-launch along with rigorous privacy regulations around patient data handling embedded within clinical trial conduct frameworks [S4][S5][S15]. Ensuring conformity across these domains entails significant operational burden potentially escalating costs or causing sanctions if inadequately managed.

Pricing pressures accentuated by recent legislation like the Inflation Reduction Act introduce further uncertainty through potential reimbursement limitations tied to Medicare pricing negotiations affecting commercial viability forecasts [S23][S26]. Global regulatory heterogeneity beyond US borders also poses market access complexities if expansion pursued following initial approvals highlighting geopolitical variability in acceptance criteria [S16][S21].

What Investors Should Watch: Upcoming Trials, Data Readouts, and Funding Catalysts

Looking forward into mid-to-late 2026 horizons key value inflections revolve around several pivotal events: completion and analysis from Phase 2b registrational trial patients receiving ACR-368 stratified by OncoSignature assay results; interim or final Phase 1 safety/efficacy disclosures related to ACR-2316 dosing regimens; progression milestones related to preclinical candidate development; plus anticipated regulatory review submissions tied directly or indirectly to companion diagnostics validation processes reported in SEC filings and media commentary [N1][S3].

Parallelly attention should be paid to financing developments given substantial burn identified over preceding years combined with absence of operating revenues requiring periodic equity or debt issuances essential for extended runway sustainability [S2]. How management sequences trial initiation scales alongside capital raises will affect risk perception.

Beyond mere developmental calendar arrivals monitoring FDA feedback tone regarding co-developed diagnostics regulation trends could forecast event-driven volatility associated with future labeling claims breadth or REMS impositions impacting commercial strategies.

This analysis aims solely at providing an informed overview based on currently available public filings without conveying investment advice or recommendations concerning any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments