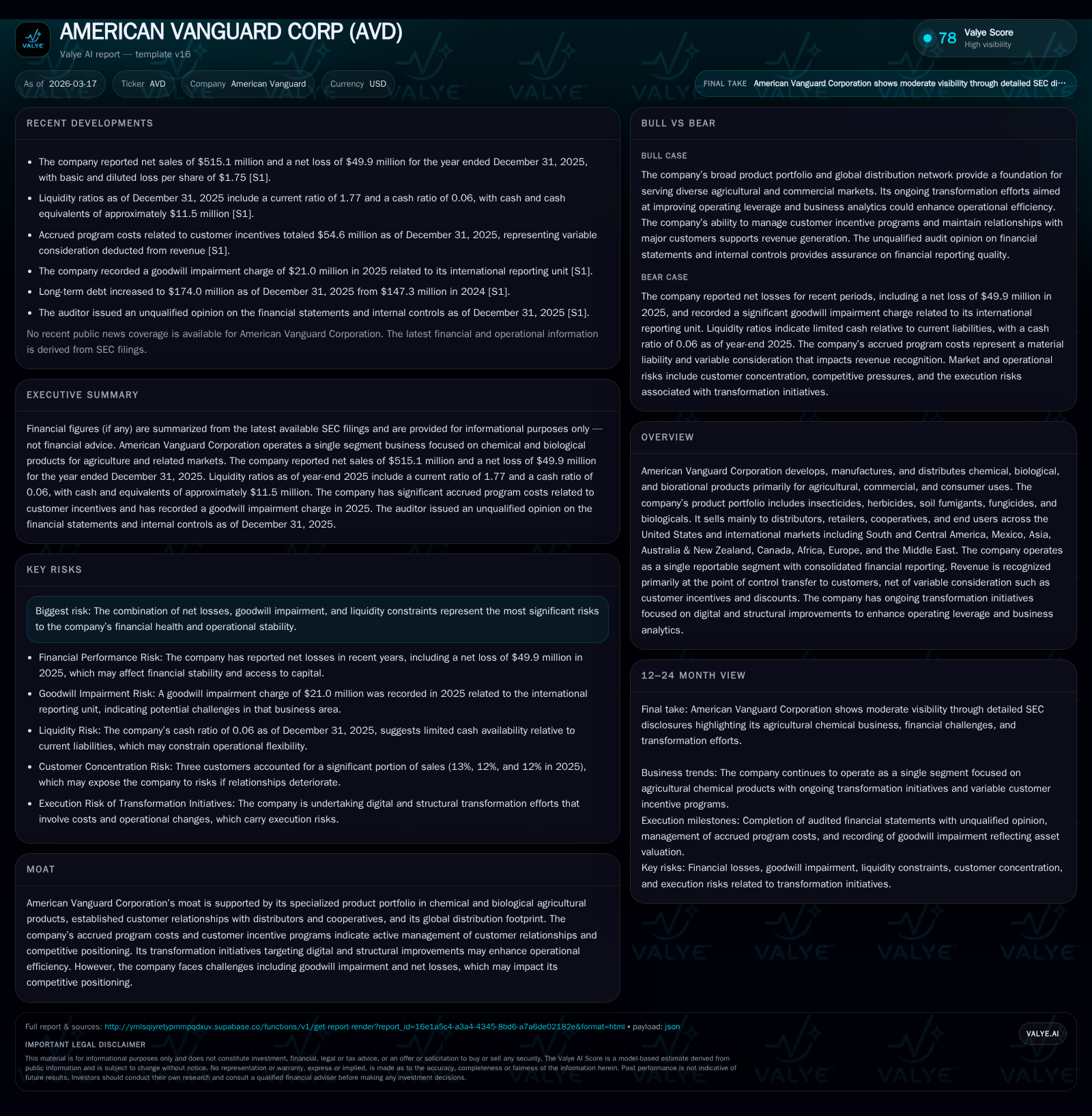

American Vanguard Corp Faces Profitability Challenges Despite Revenue Recovery and Operational Restructuring

The company is navigating operational losses and financial headwinds while pursuing a global agricultural chemical business transformation.

American Vanguard Corporation operates in a specialized niche of agricultural chemicals and biological products with sales spanning multiple continents. After sharp net losses and goodwill impairments in recent years, revenue rebounded by over 30% recently, yet operating losses persist as the company undertakes structural and digital transformation efforts. Heavy debt and liquidity covenants shape capital allocation decisions, precluding share buybacks or dividends for now. The firm's future growth hinges on stabilizing operations, managing legacy legal risks, and optimizing its diverse product portfolio across geographies.

Company Overview

American Vanguard Corporation (AVD) develops and markets chemical, biological, and biorational products primarily targeting agricultural applications alongside commercial and consumer uses. Its product range spans insecticides, herbicides, soil fumigants, fungicides, and microbial-based biologicals. The firm sells predominantly through distributors, cooperatives, retailers, and direct end-users across broad geographic regions including the United States, South and Central America, Mexico, Asia Pacific territories such as Australia/New Zealand, Canada, Africa, Europe, and the Middle East [S8], positioning it as a global player within its specialty agrochemical sector.

The company's operations are reported under a single segment due to integrated management oversight emphasizing consolidated performance metrics by the Chief Executive Officer acting as the Chief Operating Decision Maker (CODM) [S6], [S11]. American Vanguard's business model hinges on its specialized product portfolio and established relationships within its distribution channels.

Historical Financial Performance

Annual financial data reveals an uneven profitability trajectory over recent years. Revenue grew steadily from $77.6 million in 2014 to $116.5 million by 2017 but recent data shows increased volatility attributed to operational setbacks:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -50 | -21 | -28 | +60.5% |

| 2024 | -126 | 4 | -102 | -1780.3% |

| 2023 | 8 | -59 | 23 | -72.6% |

| 2022 | 27 | 57 | 41 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) |

|---|---|---|

| 2025 | 0 | 0 |

| 2024 | 3 | 0 |

| 2023 | 3 | 16 |

| 2022 | 3 | 34 |

Source: SEC companyfacts cache [F1].

Source: [F1]

The stark swings reflect periods of impairment charges seen notably in goodwill write-downs associated with underperforming assets or acquired businesses; for instance, impairment charges reached upwards of $14 million linked to SIMPAS assets in former years [S21], highlighting challenges absorbing past acquisitions into profitable operations.

Cost pressures including manufacturing overheads contribute significantly; depreciation expenses hovered near $6-8 million annually while advertising spend declined markedly from peaks exceeding $5 million towards under $3 million by recent years as part of cost containment strategies [S6], [S13].

Cash flows reveal seasonal stress: negative cash flow from operations of $21 million in the latest fiscal year contrasts with intermittent positive inflows illustrating fluctuating working capital demands influenced by inventory and receivables dynamics given global client spread.

Growth Prospects

The firm’s growth outlook currently centers on leveraging its ongoing transformation program—focused on deploying digital solutions to streamline data accessibility across business units alongside structural redesigns intended to unlock operating leverage via analytics-driven improvements across production processes and pricing strategies [S6].

Geographically diversified sales underpin revenue resilience: South and Central America contribute substantial sales volume internationally while markets like Mexico, Asia Pacific regions including Australia/New Zealand along with smaller but strategic presences in Canada, Africa, Europe and the Middle East complete the footprint [S24]. This international scope offers buffer potential from localized market disruptions though segments like Africa have experienced volatility impacting short-term sales.

However, lingering legal risks from product liability claims linked to a recall involving insecticide contamination have necessitated accruals approximating $7.6 million with ongoing litigation against third-party formulators potentially extending resolution timelines and financial exposure [S20]. Additionally, residual effects from discontinued products involving DBCP-related litigations spanning Latin American jurisdictions introduce unpredictable contingent liabilities.

Risks Capping Growth

- Persisting net losses indicate challenges achieving sustainable profitability despite revenue recovery.

- High leverage coupled with restrictive debt covenants limits financial flexibility for reinvestment or shareholder returns [S4], [S7].

- Exposure to environmental regulatory scrutiny due to product line nature poses compliance risks.

- Competitive pressure within specialty agrochemicals requiring continuous innovation investment despite recent declines in R&D spend (approximately $8.9 million in latest year from over $12 million prior) may hamper long-term product pipeline vitality [S13].

Capital Structure & Liquidity

American Vanguard carries significant indebtedness stemming from a senior credit facility originally aggregating a revolving credit line up to $275 million plus accordion features that have been amended multiple times since inception in August 2021 [S3], [S7]. Recent amendments extended maturity dates into late 2026 before an early-2026 refinancing replaced prior facilities with a senior secured term loan of $225 million featuring a five-year tenor accompanied by stepped covenant requirements tracking leverage ratios tightening progressively toward fiscal Q4 2028 targets [S4].

Interest rates remain elevated given market conditions: initial SOFR floor plus margin yielding starting rate above approximately 11%, reflecting heightened credit costs for covenant-heavy lending arrangements conditional on quarterly EBITDA targets ranging up to approximately $37.5 million trailing twelve months by early next fiscal quarter end [S4], consistent with private credit market dynamics for highly leveraged industrial businesses.

Liquidity provisions mandate maintaining minimally defined cash balances between $20-$50 million varying monthly through early calendar years ahead while necessitating prepayments if held cash exceeds thresholds designed to mitigate default risk exposure by lenders.

No dividends were paid in the most recent fiscal year reflecting both operating losses alongside restrictions enforced by credit agreement amendments prohibiting share repurchases since late calendar year 2023; last repurchases occurred during fiscal year ending December 2023 totaling about $15.5 million at average prices near $17 per share prior to covenant impositions curtailing capital return programs ongoing presently [F1], [S17].

Operational Challenges & Legal Environment

Ongoing environmental compliance programs relate partly to historical legacy liabilities such as DBCP production cessation dating back decades but still subject to multiple lawsuits connected with alleged health impacts on Latin American agricultural workers; management disfavors current loss recognition for these suits pending further developments given uncertainty around causation claims against American Vanguard specifically within consolidated litigation proceedings slated for trial phases starting mid-2026 onwards [S22].

Recent product recall involving contaminated insecticide batches resulted in validated customer claims exceeding two dozen settlements totaling approximately $2 million paid so far while reserving nearly $7.6 million for outstanding validated claims related but unresolved fully at year-end reflecting robust provisioning aligned with standard industry practices concerning reputational risk mitigation efforts amid supply chain quality control failures at outsourced formulation providers triggering legal disputes between American Vanguard and implicated third parties for indemnification claims ultimately affecting cost absorption profiles going forward into fiscal cycles commencing beyond December calendar year-end close preparation dates reported herewith [S20].

Outlook & What To Watch

Explicit forward guidance has not been issued formally yet per disclosures; keeping track of upcoming quarterly EBITDA trends against lender covenant thresholds will be essential to monitor shifts toward improved earnings trajectories or further pressure leading potentially either to refinancing complexity or restructuring triggers beyond existing amendment reliefs. Also observe progress on trimming transformation costs post initial severance/program expense spikes alongside any profitable stabilization manifested via shrinking operating losses quarter-over-quarter given the company's emphasis on digital infrastructure improvements aimed at operational efficiency gains which could be pivotal turning points supporting mid-term viability. Finally pay attention to resolution updates on major litigation including plant injury suits filed internationally which remain material contingencies affecting balance sheet strength assessed through provisions analysis changes reported periodically together with disclosures around insurance recoveries involved concurrent with legal action outcomes pursued against suppliers/formulators implicated in contamination events.

Conclusion

American Vanguard stands at a crossroads balancing improving top-line momentum against persistent bottom-line deficits exacerbated by legacy asset impairments, operational inefficiencies, high leverage costs, and contingent legal liabilities common among legacy specialty chemical manufacturers operating globally amidst evolving regulatory landscapes.The firm is redirecting focus toward structural transformations signaled by ambitious internal initiatives coupled with heavy refinancing maneuvers designed to offer runway for turnaround prospects though concrete results hinge heavily on execution pace plus external factors influencing market reception of crop input products across geographically diverse agrarian economies.Without meaningful improvements on all fronts—including working capital management optimizing cost structures resolving legal exposures—the path back toward consistent profitability remains guarded though not implausible given specialized product niche characterizing company's technical moat supported by entrenched distributor partnerships worldwide.

This analysis is based solely on publicly available information as of March 17, 2026, including SEC filings and verified news sources without providing investment advice or predictions regarding security performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments