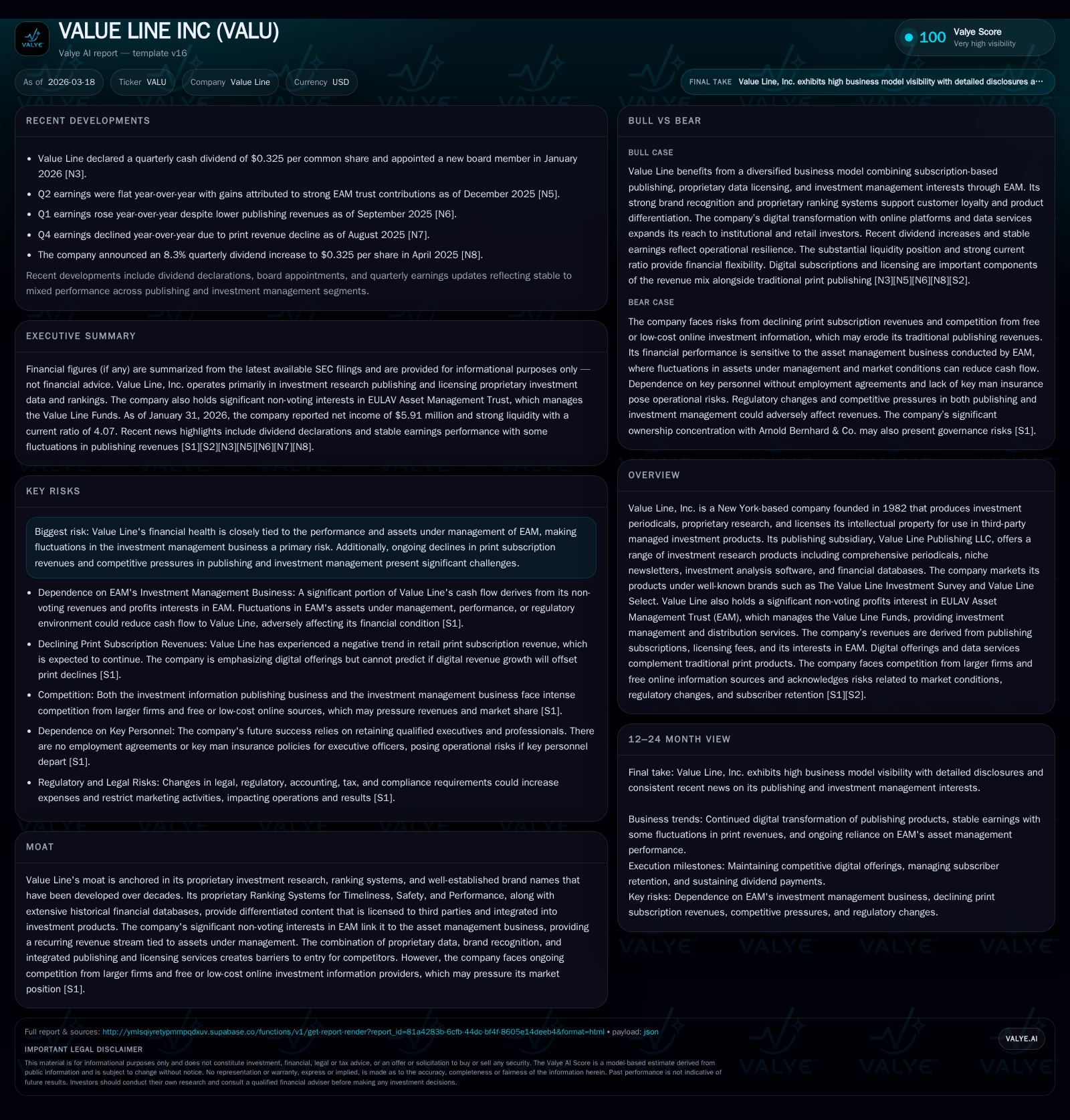

Value Line Inc. Leverages Proprietary Research Amid Shifting Publishing and Asset Management Dynamics

The company maintains steady top-line revenue supported by subscription and licensing models, while its earnings reflect pressures from competitive markets and asset management fluctuations.

Value Line Inc., operating since 1982, blends traditional investment publishing with proprietary research licensing and asset management interests. Historical financials indicate relatively stable revenue, tempered by declining operating income due to rising costs and market challenges. Its significant non-voting stake in EULAV Asset Management Trust ties Value Line’s cash flow closely to fund performance and assets under management, a factor contributing both revenue stability and volatility risk. The company’s strong brand equity and proprietary ranking systems underpin its moat but face pressure from free online information providers and changing investor behaviors. Capital allocation favors shareholder returns, although buybacks have tapered recently.

Company Overview

Founded in 1982 and headquartered in New York City, Value Line Inc. has forged a niche as a provider of premium investment research through multiple channels including periodicals, newsletters, software tools, historical financial databases, and licensed intellectual property embedded in third-party managed investment products. The company operates a wholly owned publishing subsidiary offering flagship services such as The Value Line Investment Survey—a weekly print periodical supplemented by daily digital updates—and a suite of specialized newsletters targeting dividends, ETFs, special situation stocks, M&A opportunities, and climate-conscious investments [S18][S23][S25].

Since its establishment of EULAV Asset Management Trust (EAM) in 2010, Value Line has held significant non-voting interests entitling it to revenues tied to assets under management within the Value Line Funds family. This structure offers a recurring cash flow stream linked to fund performance but exposes the company to market volatility risks inherent in asset management [S1][S24].

Historical Financial Performance

Value Line’s revenue performance over recent years has been relatively steady with recorded revenue at approximately $36.3 million in FY2019 [F1]. Despite this presumed stability in top-line figures — supported primarily by subscription fees and licensing income — the operating income trajectory shows noticeable contraction from $11.5 million in FY2023 down to $5.985 million in FY2025, representing a decline of about 34.5% year-over-year [F1]. This shrinkage is likely attributable to intensified competition—especially from online platforms providing free or low-cost investment research—and cost inflation factors impacting content creation and distribution.

Net income for FY2025 registers around $20.7 million, an increase of nearly 8.8% compared to the previous fiscal year. This divergence between operating profitability compression and net income improvement suggests effective management of non-operating items or benefits from other income sources such as the company's stakes in investments or EAM operations [F1].

Operating cash flow follows a healthier uptrend at approximately $20.2 million for FY2025 (up nearly 13% year-over-year), reaffirming operational cash generation capability despite margin pressures [F1]. Capital expenditures remain modest relative to overall cash flows with about $178k spent in FY2025 reflecting limited investing needs for physical infrastructure or technology relative to peers [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 21 | 20 | 6 | 178000 | +8.8% |

| 2024 | 19 | 18 | 9 | 15000 | +5.2% |

| 2023 | 18 | 18 | 11 | 30000 | -24.1% |

| 2022 | 24 | 25 | 11 | 11000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 11 | 0 | 20 |

| 2024 | 11 | 1 | 18 |

| 2023 | 9 | 5 | 18 |

| 2022 | 8 | 2 | 25 |

Source: SEC companyfacts cache [F1].

Note: Revenue numbers are limited to available fiscal year-end data; YoY percentages computed only where applicable.

Business Model Nuances

Value Line’s core competitive advantage hinges on its proprietary ranking systems — notably Timeliness™, Safety™, and Performance™ — which provide quantitative frameworks for evaluating equities over short-to-intermediate horizons based on fundamental financial criteria integrated with analytical oversight [S23][S26]. These rigorously maintained datasets form the backbone not only for subscriber-facing publications but also serve as licensed inputs into third-party funds such as ETFs and unit investment trusts.

Supplementing direct subscriptions are institutional licensing agreements where proprietary ranks are embedded in investment products distributed broadly through brokerage networks—this multi-channel monetization helps diversify revenue beyond traditional publishing cycles.

The company's publishing products have a bifurcation: comprehensive surveys like The Value Line Investment Survey appeal to broader professional/institutional investors covering thousands of stocks; whereas targeted newsletters (e.g., dividend-focused or climate-investing themes) cater to niche segments seeking specialized insights [S25][S29]. Digital transformation efforts have focused on accessibility through online platforms like the Value Line Research Center, featuring enhanced screening tools, charting capabilities, model portfolios backing quantitative strategies seeded by their ranks, plus thematic equity services aligned with ESG trends [S26][N1][N2].

Future Growth Prospects

Value Line faces both growth headwinds and opportunities that will shape its near- to medium-term trajectory:

Digital Subscription Expansion: Although print revenues show structural decline manifestations typical across periodicals (partly due to free online alternatives), the company intensifies efforts on digital product innovation aiming for higher penetration among retail investors and professional advisory channels via tiered digital packages and data service enhancements [S17][S29]. Whether these gains can offset print attrition remains the pivotal growth constraint.

Licensing Fee Upside: As more ETFs and unit investments rely on quantitative ranking criteria reflecting Value Line’s proprietary data sets—especially under rising demand for systematic strategies—licensing fee income could benefit from growing AUM in third-party vehicles utilizing their intellectual property [S19][S24]. This depends on maintaining superior efficacy of rankings versus competing rating agencies.

Investment Performance Sensitivity: The extent of recurring cash flow tied to EAM’s results implies positive performance relative to benchmarks could bolster fees via increased assets under management; conversely, underperformance risks lead to rapid redemptions or rating downgrades adversely impacting fee receipts for both EAM and consequently Value Line’s distributable profits portion [S1][S24].

Product Innovation: Niche offerings like the Climate Change Investing Service launched recently offer potential for differentiated content addressing emerging segments motivated by ESG integration trends which may grow investor interest amid regulatory shifts favoring sustainability disclosures [S23][N2].

Forecasts and Expectations

While explicit forward-looking guidance is not provided publicly beyond narrative disclosures, upcoming milestones warrant monitoring:

- Renewal rates for both print and digital subscriptions indicating subscriber retention trajectories.

- Assets under management trends within Value Line Funds managed by EAM affecting recurring cash flows.

- Development pace of digital platform usage including active user growth metrics across The Value Line Research Center.

- Responses of competitors enhancing free or low-cost investment data offerings which could erode pricing power.

- Regulatory landscape impacting EAM’s fund fees or distribution capabilities given SEC oversight intensity on investment advisers.

Returns and Capital Allocation

Value Line exhibits a disciplined approach toward capital allocation with sustained dividend growth reflecting confidence in underlying cash flows; dividends reached $11.3 million in FY2025 marking incremental increases over prior years [F1][S9]. Share repurchase activity has been modest recently (~$0.45 million FY2025), signaling cautious deployment amid uncertain industry disruption.

The company generates strong free cash flow (~$20 million estimated as CFO less capex) supporting liquidity buffers (current ratio approximately above fourfold as per January 2026 balance sheet) ensuring operational flexibility during market stress events [F1][S8]. Equity capital has steadily grown surpassing $99 million at latest fiscal year end indicating retained earnings accumulation without dependence on external financing.

Return on equity approximates just over twenty percent (20.8%) evidencing efficient use of capital relative to profitability measures typical for specialized publishing-cum-financial data firms balancing content-intensive expense structures against high-margin intellectual property licensing streams [F1].

Risk Factors Summary

Critical risk exposures include:

- Heavy dependence on EAM’s investment management performance as fee-related revenues directly correspond with market valuations and investor inflows/outflows impacting funds under management volume [S1][S16].

- Competitive threats from larger scale research providers benefiting from technological advantages or deeper pockets potentially diminishing Value Line subscriptions/licensing shares particularly amid proliferation of fintech platforms aggregating free equities data sets online [S7][S12].

- Intellectual property rights enforcement challenges that may dilute brand recognition or reduce monetization opportunities if infringement occurs unchecked or litigation expends disproportionate resources.

- Loss of key executive talent given absence of employment contracts or "key man" insurance adding execution risk against operational continuity assumptions especially pertinent given specialized analytics skills requisite for maintaining proprietary ranking reputations.

- Regulatory scrutiny risks involving compliance with Investment Advisers Act rules governing EAM’s fund advisory arrangements potentially altering fee structures or contract terms undermining future earnings predictability.

- Declining print subscription revenues due partly to secular media consumption shifts despite concurrent increases in select digital markets requiring effective marketing channel adaptations for maximum subscriber acquisition.

Conclusion

Value Line stands as a venerable institution within investment research circles leveraging decades-old institutional knowledge embedded within proprietary ranking methodologies respected among investors globally. Stable subscription bases combined with diversified licensing arrangements underpin a moat resilient against commoditization but not immune amid acceleration toward digitization post-pandemic combined with evolving client demand profiles seeking real-time advanced analytics ahead of traditional periodic surveys.

Strategic emphasis on expanding digital footprints across retail/professional segments alongside sustained commercialization of IP through third-party fund sponsors represents balanced responses targeting volume growth while preserving reputation-driven pricing power potential.

Nevertheless, investor-watchers should remain attentive to market environment shifts influencing asset management inflows at EAM along with regulatory developments bearing on fee economics that jointly govern major portions of Value Line’s financial outcomes beyond core publishing revenues.

This analysis synthesizes publicly available financial statements filed with the SEC along with company disclosures as well as sector context without constituting any recommendation or solicitation related to ownership or trading decisions regarding Value Line Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments