Taysha Gene Therapies’ Clinical Progress and Financial Strain Highlighted by TSHA-102 FDA Breakthrough

Taysha Gene Therapies advances in neurological gene therapies but faces escalating operating losses and regulatory uncertainties.

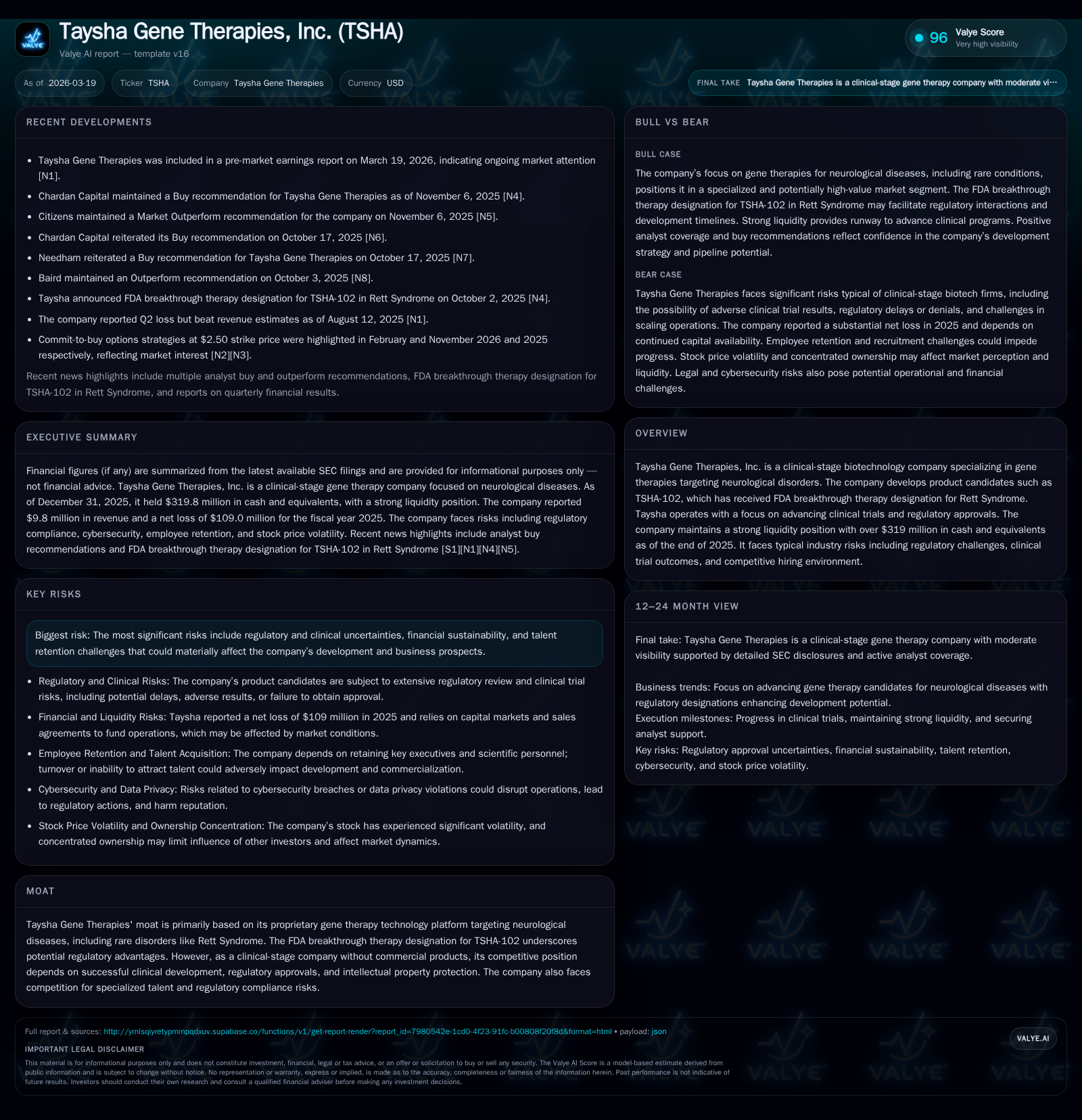

Taysha Gene Therapies remains a clinical-stage biotech devoted to gene therapies for rare neurological diseases, notably Rett Syndrome via TSHA-102, which secured FDA breakthrough therapy designation. While revenue growth of over 17% in 2025 reflects clinical development momentum, the company incurred increasing losses amid sizable operating expenses. Its balance sheet shows a robust cash position to support ongoing trials, yet challenges including regulatory risks, legal proceedings, and talent retention pose significant headwinds. Monitoring trial data readouts and regulatory milestones will be critical to assessing future value creation prospects.

Company Overview

Taysha Gene Therapies, Inc. is a clinical-stage biotechnology firm focusing on developing gene therapies for debilitating neurological disorders. This includes rare diseases such as Rett Syndrome, for which its lead candidate TSHA-102 has received a coveted FDA breakthrough therapy designation [N1][S1]. The designation highlights potential expedited regulatory review pathways that could differentiate Taysha within the crowded gene therapy developmental space.

The company operates out of Dallas, Texas with leased administrative and manufacturing facilities appropriate for its current scale of operations [S25]. Its business model centers on advancing multiple clinical trials aimed at securing regulatory approvals before commercial launch. Currently, Taysha does not generate meaningful product sales revenue but derives revenue primarily from collaborations and potentially milestone payments associated with its pipeline progress.

Historical Performance and Financial Trends

Over the trailing four years, Taysha’s top-line trajectory has been variable but growing overall from $2.5 million in FY2022 to $9.8 million in FY2025 — a compound build driven by incremental progress in clinical development activities [F1]. The table below summarizes key financial metrics:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 10 | -109 | -93 | -110 | +17.3% | -22.1% |

| 2024 | 8 | -89 | -81 | -91 | -46.1% | +20.0% |

| 2023 | 15 | -112 | -73 | -72 | +517.5% | +32.8% |

| 2022 | 3 | -166 | -88 | -162 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -94 | -44.1 |

| 2024 | -82 | -124.8 |

| 2023 | -77 | -148.9 |

| 2022 | -109 | -17493.6 |

Source: SEC companyfacts cache [F1].

*Note: Revenue decline from FY2023 to FY2024 of approximately -46% reflects variability likely tied to milestone recognitions or partnership revenues typical in early-stage biotechs.

Despite rising revenues reflecting maturation of development programs, operating losses have deepened year-over-year (increasing operating expenses tied largely to clinical trial execution) culminating in an operating loss of $110 million for FY2025 [F1]. Negative net income closely follows this trend as R&D and G&A expenditures remain substantial without offsetting commercial revenues.

Cash flow from operations remains highly negative (approximately $93 million outflow in FY2025), consistent with a clinical-stage biotech's investment phase; conversely, capital expenditures have declined markedly from peak levels seen in FY2022 when facility investments were more prominent [F1].

Shareholder equity saw a significant increase by the end of FY2025 ($247 million), boosted presumably through capital raises during the period despite ongoing losses [F1]. This influx maintains ample runway funding near $320 million cash balance at end of calendar year 2025.

Growth Catalysts and Development Pipeline

TSHA-102's breakthrough therapy status for Rett Syndrome positions it as a central value driver through anticipated faster FDA review timelines [N1][S1]. Successful advancement through pivotal trial phases would represent a transformative milestone enabling commercialization opportunities.

Beyond TSHA-102, Taysha continues preclinical or early-stage efforts across neurological indications leveraging its proprietary gene therapy platform [S23]. Innovations include next-generation AAV vector technologies targeting CNS delivery obstacles—a key challenge for systemic gene therapies addressing brain disorders.

Future growth catalyzers depend fundamentally on positive clinical trial readouts leading to NDA submissions and eventual approvals [N1][S3]. However, risks remain substantial given typical uncertainties surrounding safety, efficacy data interpretation, patient enrollment dynamics, and regulatory feedback cycles common to gene therapy pipelines.

Regulatory Environment and Legal Risks

The company's risk profile includes inherent regulatory unpredictability amplified by an ongoing SEC investigation related to fundraising activities executed during August 2023 private placements; while document production was completed in April 2025, no wrongdoing has been adjudicated [S5]. Parallel derivative litigation concerning these financings continues without a current resolution [S25].

Taysha also articulates heightened exposure to cybersecurity incidents that might disrupt sensitive intellectual property management or clinical data integrity with potential reputational damage or operational delays [S1][S9][S19]. The board’s audit committee actively oversees cybersecurity risk protocols.

Compliance with evolving global data privacy laws—including HIPAA, GDPR and CCPA—adds complexity around patient data handling given multinational trial footprints and partnerships [S6][S18]. Failure in adherence could impair trial continuity or trigger fines.

Capital Allocation and Returns Profile

As a pre-commercial entity generating negative operating cash flows (-$93 million CFO minus ~$0.7 million capex = roughly -$93 million free cash flow), Taysha currently prioritizes reinvestment into development over shareholder distributions [F1][S21]. There are no dividends declared or share repurchase programs underway due both to liquidity conservation strategy and restrictions embedded within the company's term loan agreement from the 'Trinity Term Loan' financing secured in early 2025 [S21].

ROE calculated as net income divided by equity stands near negative 44% reflecting continued unprofitability despite an improving equity base post-capital raises [F1].

Investors will gauge capital stewardship success based on progression toward proof-of-concept validation of lead candidates rather than traditional return metrics at this development stage.

Industry Context Considerations (Analysis)

The gene therapy field targeting neurological disorders sits at the intersection of biotechnology innovation hurdles—particularly CNS delivery challenges—and stringent regulatory scrutiny due to safety concerns stemming from durable gene modifications . Competition spans established players advancing proprietary AAV capsids alongside newer entrants utilizing non-viral gene editing modalities.

Talent acquisition is particularly acute here where expertise must amalgamate virology, neurology, genetic engineering, manufacturing scale-up capabilities plus regulatory sophistication—a multi-disciplinary skillset that commands premium compensation packages amid tight labor markets .

Consequently, Taysha's emphasis on retaining key executives amid recent team changes is critical; unexpected turnover could impede clinical timelines or strategic execution integrity [S13][S27].

What To Watch Forward (Analysis)

Key upcoming milestones include:

- Interim or final results from Phase I/II studies of TSHA-102 that may validate safety/efficacy claims warranting advancement toward registration-enabling studies.

- Regulatory interactions including potential FDA meetings to clarify requirements or respond to complete response letters where applicable.

- Progression addressing derivative litigation outcomes that may affect governance perceptions or distract management.

- Capital deployment efficiency observed through quarterly burn rates relative to clinical program activity ramp-up.

- Evolving cybersecurity compliance posture especially given recent legislative tightening around health data security.

Monitoring financial burn versus runway available funds alongside newsflow on these fronts will offer insight into operational sustainability until therapeutic product commercialization is feasible.

Conclusion

Taysha Gene Therapies embodies typical attributes of an emerging biotech specializing in cutting-edge treatments for unmet neurological needs: promising scientific platform validated recently by breakthrough designation juxtaposed against steep losses reflecting intensifying R&D investment and operational complexity constraints.

Maintaining financial health through prudent cash management while progressing TSHA-102’s pivotal trials constitutes the primary challenge ahead alongside navigating regulatory checkpoints amidst macro compliance pressures on data security and governance transparency.

This positions Taysha as a company still firmly “investing” with anticipated return profiles hinging heavily on binary success/failure outcomes inherent in advanced biopharma innovation cycles.

This report is intended solely for informational purposes based on publicly available information as of March 19, 2026. It does not constitute investment advice or recommendation regarding any security mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments