Mereo BioPharma Confronts Clinical and Financial Hurdles with Rare Disease Pipeline

Clinical-stage focus on osteogenesis imperfecta and alpha-1 antitrypsin deficiency drives ongoing investment amid regulatory and funding challenges.

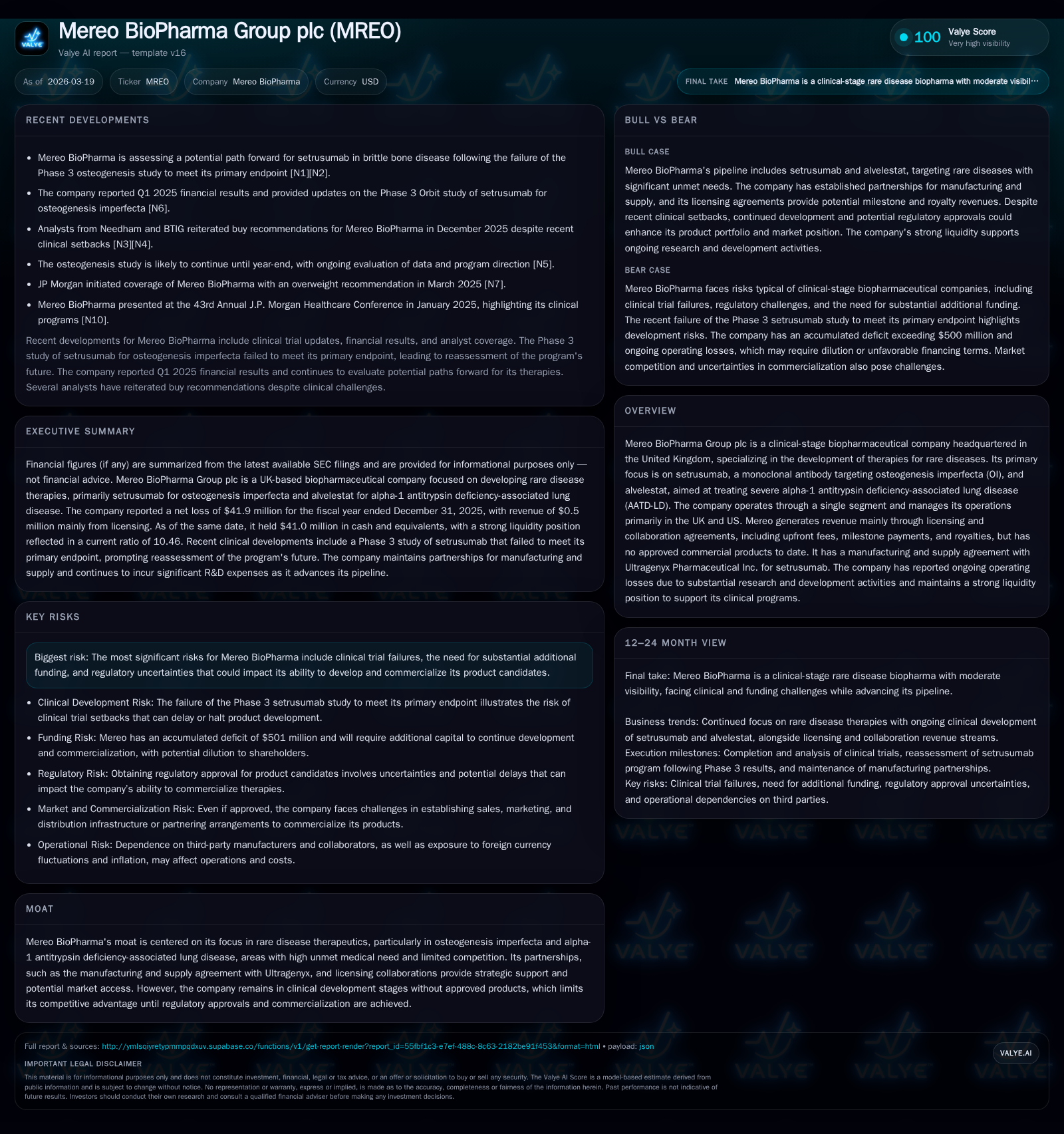

Mereo BioPharma Group plc specializes in developing therapies for rare diseases, chiefly setrusumab for osteogenesis imperfecta and alvelestat for alpha-1 antitrypsin deficiency lung disease. The company remains pre-commercial, generating modest revenue from licensing and collaborations but continues to operate at significant losses driven by its R&D expenditure. Strong liquidity extends into mid-2027, yet sustaining development requires raising additional capital while navigating clinical risks and Nasdaq listing pressures. Strategic manufacturing partnerships provide some operational leverage, but commercialization hinges on upcoming trial outcomes and regulatory approvals.

Company Overview

Mereo BioPharma Group plc is a clinical-stage biopharmaceutical entity headquartered in the UK focused exclusively on rare disease therapeutics. The company's portfolio centers on two late-stage candidates: setrusumab, a monoclonal antibody targeting osteogenesis imperfecta (OI), and alvelestat for severe alpha-1 antitrypsin deficiency-associated lung disease (AATD-LD). These indications represent areas of significant unmet medical need with limited approved treatment options.

The firm operates predominantly in the UK and US markets through a singular business segment dedicated to drug development. It currently does not have any approved commercial products but generates limited revenue primarily through licensing agreements entailing upfront payments, milestone achievements, and royalties contingent on future product sales.

Historical Performance and Growth Drivers

Financially, Mereo has exhibited persistent operating losses consistent with its stage of development. Revenue generation is nascent; notably, after registering $10 million in billings in FY2023 linked to licensing milestones, reported revenue fell sharply to $500,000 in FY2025 as those milestone events waned or delayed ([F1]). This volatile revenue pattern underscores the reliance on episodic payments rather than product sales.

Operating income improved modestly yet remained negative at -$40.1 million for 2025 compared to -$47.4 million for 2024 as research and development (R&D) expenses stabilized ([F1]). The net loss followed a similar trajectory indicating that cost containment efforts offset some but not all expenditures.

R&D expenditures have been the primary driver of operating losses given ongoing clinical trial commitments and pipeline advancement costs ([S23]). Operating cash flow also remained negative at approximately -$31 million for 2025 reflecting these heavy investment activities ([F1]).

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1 | -42 | -31 | -40 | +3.2% | |

| 2024 | 0 | -43 | -33 | -47 | -100.0% | -46.8% |

| 2023 | 10 | -29 | -21 | -28 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -31 | -102.4 |

| 2024 | -70.9 | |

| 2023 | -21 | -58.3 |

Source: SEC companyfacts cache [F1].

Notably, capex remains minimal highlighting the company's asset-light model focusing mostly on externalized R&D services; all figures are sourced from F1.

Future Growth Prospects

Mereo's growth prospects hinge predominantly on the progress of its lead clinical assets reaching critical milestones. Setrusumab’s advancement toward potential regulatory approvals in Europe via collaboration with Ultragenyx—who manages manufacturing supply—constitutes a key near-term catalyst ([S14]). Similarly, alvelestat’s clinical trials for AATD-LD hold promise but require further validation.

Achieving successful clinical outcomes could unlock milestone payments from partners as well as eventual royalties upon commercialization ([S22]). However, no explicit guidance has been provided regarding timing or magnitude of such events; accordingly, these factors represent speculative upside.

Expanding intellectual property rights and pursuing additional rare disease opportunities through licensing or acquisitions could supplement pipeline breadth but also require substantial capital input ([S1]). Regulatory challenges remain substantial owing to inherent complexities around orphan disease pathways.

Financial Outlook and Milestones to Monitor

While Mereo does not provide explicit public guidance due to typical early-stage biotech uncertainties, attention should focus on:

- Clinical trial readouts for setrusumab’s OI indication.

- Progression or initiation of pivotal studies for alvelestat.

- Updates on collaborations or licensing agreements unlocking milestone revenues.

- Regulatory filings or approvals granting marketing authorization.

- Structural negotiations with Ultragenyx surrounding manufacturing scale-up.

Monitoring cash burn rates against liquidity targets will be essential as the company guides that current funds support operations into mid-2027 only ([S1]). Given this runway constraint without significant revenue inflows or additional fundraising, financing strategy execution will be critical.

Returns and Capital Allocation

Return measures currently illustrate typical high-risk biotech profiles: approximate return on equity for FY2025 is about -102%, primarily due to sustained net losses over moderate equity capital committed ([F1]). Free cash flow remains negative near -$31 million reflecting ongoing development expenses exceeding any incoming cash inflows.

No dividends or share buyback programs exist given pre-commercial status and capital conservation priorities ([F1]). Capital allocation continues to prioritize internal R&D spending along with patent maintenance and public listing expenses ([S1]).

The company’s balance sheet reflects prudent liquidity management with cash and equivalents totaling approximately $41 million at year-end 2025 ([F1]), complemented by a strong current ratio exceeding ten times due to low current liabilities relative to assets ([F1]). However, equity declined from ~$61 million at end-2024 to about $41 million in 2025 signaling capital erosion from net losses ([F1]).

Industry-Specific Considerations

Rare disease drug development often commands high clinical complexity surrounded by limited patient populations complicating trial enrollment and endpoint clarity—a challenge that Mereo faces acutely given its focus areas. Pricing pressures are somewhat muted by orphan drug exclusivity incentives but reimbursement debates remain nontrivial especially across varied healthcare systems regionally within Europe versus U.S.

For manufacturing dependent biotechs like Mereo relying on third-party vendors such as Ultragenyx represents strategic leverage but also operational risk if delays occur or contractual conditions shift unfavorably—a noted exposure here ([S14]).

Another domain nuance is regulatory predictability; while accelerated pathways might exist for rare diseases via agencies like EMA or FDA under breakthrough therapy designations, uncertainties persist around post-marketing requirements which could inflate costs unexpectedly.

Risks Summary

Risks center around clinical development failures or delays which would carry profound financial consequences given concentrated pipeline exposure ([S4]). Additional funding needs pose material concerns given burn rates outpacing revenues and incomplete capital markets access given Nasdaq listing compliance issues linked to ADS price declines noted recently with August 2026 deadline looming ([S4]).

Regulatory challenges including potential safety findings or complex trial results could stall progress undermining commercial viability expectations ([S4]). Market competition though modest due to rarity may still emerge which could impact eventual pricing power or adoption curves.

Conclusion

Mereo BioPharma embodies a high-risk high-reward profile typical of specialized clinical-stage biotech firms narrowly focused on rare diseases lacking approved products or dependable commercial revenues today. Its path forward relies heavily on progression of key assets through critical late-stage development milestones backed by collaborative partnerships that mitigate some operational burden but leave strategic execution challenges unresolved.

Investors and stakeholders should closely watch forthcoming clinical data releases, capital raising initiatives, regulatory interactions, and stock market developments including Nasdaq listing compliance efforts—all pivotal in determining whether Mereo can translate promising science into sustainable value creation amid inherent industry headwinds.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments