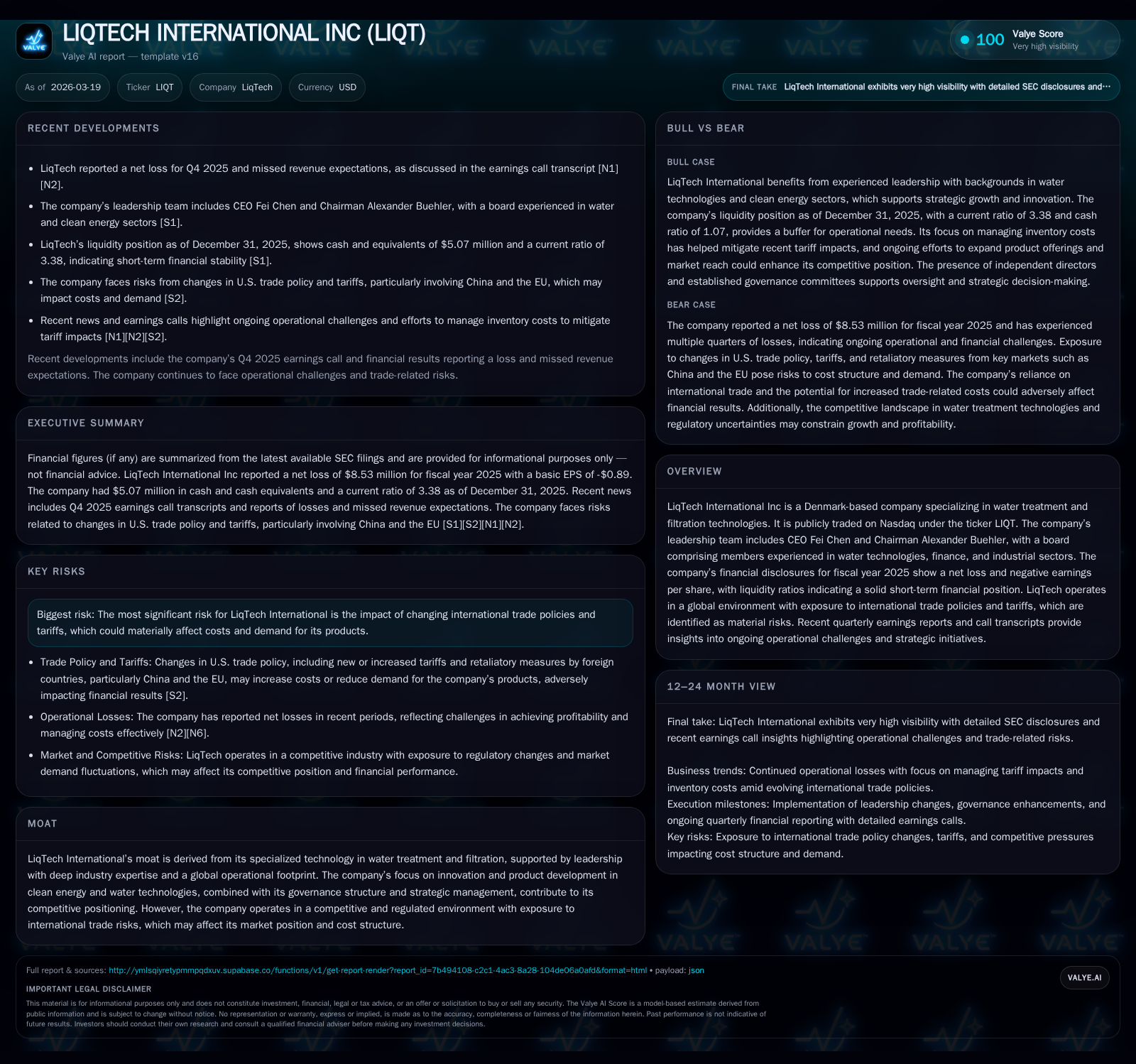

LiqTech International's Struggle to Reverse Losses Amid Tariff Pressures

The company faces ongoing deficits despite technological strengths and operational improvements, challenged by escalating trade tensions affecting cost structures and market access.

LiqTech International operates at the intersection of advanced water filtration technology and a volatile global trade environment. While FY2025 shows a contraction in operating losses compared to prior years, persistent negative margins and cash flow deficits highlight enduring operational challenges. The introduction of increased tariffs and retaliatory measures in key markets like the US, China, and EU have strained costs and sales potential, partially offset by strategic inventory management. The firm’s innovation pipeline targets sustainable water treatment solutions, but growth remains capped by geopolitical risks and fixed cost absorption hurdles. Capital allocation focuses on preserving liquidity without dividends or buybacks amid continued losses.

Innovative Foundations and Historical Financial Performance

LiqTech International bases its competitive advantage on proprietary water treatment and filtration technologies primarily involving ceramic membranes engineered for diverse industrial applications. This technological moat is supported by a management team with strong domain expertise positioning the firm within a highly specialized niche focused on water purification, wastewater treatment, and sustainability-driven markets [S1].

Financially, LiqTech has experienced persistent net losses over recent years but shows signs of gradual improvement reflecting operational scale effects and cost control initiatives. Operating income losses shrank from approximately -$12.5 million in FY2022 to -$8.3 million in FY2025—a year-over-year improvement of roughly 12.4% [F1]. Similarly, net income losses contracted from about -$14.2 million in FY2022 to -$8.5 million in FY2025 (a 17.6% improvement YoY) illustrating partial absorption of fixed costs through expanded operations or efficiency gains.

However, the company continues to operate with negative margins driven by the capital intensity of its R&D-heavy product development cycle alongside structural challenges typical for filtration membrane innovators that require sizable initial investments before scaling revenues mitigate overhead burdens.

Historical Financial Performance Summary (FY2022-FY2025)

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -9 | -6 | -8 | 0 | +17.6% |

| 2024 | -10 | -8 | -9 | 1 | -20.7% |

| 2023 | -9 | -4 | -8 | 3 | +39.5% |

| 2022 | -14 | -12 | -13 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -81.7 |

| 2024 | -9 | -62.1 |

| 2023 | -7 | -49.6 |

| 2022 | -14 | -60.8 |

Source: SEC companyfacts cache [F1].

Figures are drawn directly from SEC filings summarizing LiqTech’s continued struggle with profitability while demonstrating incremental financial stabilization through modest margin recoveries [F1].

Decoding the Recent Operating Loss Trends and Margins

Q4 2025 earnings revealed revenue shortfalls relative to expectations accompanied by continuing operating losses despite some sequential improvements [N2],[N1]. The company's ability to generate profitable operating leverage remains hindered by several factors:

- Persistently high fixed manufacturing overheads which dilute gross margin recovery given uneven order flow typical of industrial filtration projects.

- Cost inflation introduced through tariff escalations impacting imported raw materials essential for ceramic membrane fabrication.

- Product mix adjustments towards newer technologies sometimes compressing margins temporarily as scale advantages have yet to materialize fully.

The backlog trend discussed during recent conference calls signals cautious optimism but also underscores timing uncertainties around converting orders into revenue streams amidst current market turmoil [N1]. Inventory valuation changes due to tariff-influenced cost variability have further compressed reported gross margins—an aspect that bears watch as it reflects both supply chain complexity and exposure to geopolitical shifts.

Trade Policy Turbulence: Impact on Supply Chain and Market Access

Since mid-2025, LiqTech has faced intensified international trade headwinds stemming from U.S., Chinese, and European Union tariff escalations alongside reciprocal retaliatory measures that collectively raise costs and constrain export opportunities [S2],[S4],[S5],[S6]. These geopolitical frictions manifest specifically in:

- Elevated input costs for specialized filtration components sourced globally.

- Constraints on market access particularly in critical regions such as China and the U.S., affecting sales volume potential.

- Increased complexity in supply chain planning prompting strategic stockpiling maneuvers aimed at insulating operations from cost spikes—though these buffer strategies have finite effectiveness over time.

Tariff impact subsidization becomes an acute challenge as it forces either price increases risking competitive positioning or margin absorption undermining profitability benchmarks—a tension materially shaping LiqTech’s near-term financial condition [S4]. The company’s risk disclosures highlight this regard as their foremost commercial vulnerability going forward.

Innovation Pipeline and Strategic Initiatives for Future Growth

LiqTech maintains an active R&D agenda focused on refining advanced ceramic filtration membranes applicable across both conventional water treatment utilities as well as emerging clean energy sectors where ultra-pure water processing is vital [N1],[S1]. This innovation moat underpins longer-term growth aspirations by aligning products with sustainability megatrends increasingly prioritized by regulatory environments worldwide.

Key strategic initiatives include expanding capacity for next-generation products with enhanced durability and efficiency characteristics that can command premium pricing or open new applications within industrial wastewater treatment or hydrogen fuel cell markets—segments benefiting from rising environmental standards.

Despite these growth levers being well articulated publicly, the timeline for meaningful top-line revenue inflection remains uncertain given current operating deferrals caused largely by external trade policy shocks plus capital discipline constraints restricting aggressive expansion spending.

Liquidity Position, Capital Allocation, and Shareholder Returns

Reflecting conservative financial stewardship amid negative earnings trajectories, LiqTech reported a robust current ratio of approximately 3.38 at FY2025 end reflecting ample short-term asset coverage against liabilities [F1]. Cash & equivalents stand near $5 million—providing a liquidity buffer foundational for weathering continued operational deficits.

Capital expenditures declined precipitously from $1.37 million in FY2024 to just under $0.40 million in FY2025 (down over 70%), signaling tight spending control while freezing discretionary investments until clearer demand visibility emerges [F1]. This capex moderation is consistent with management’s broader capital discipline strategy outlined in governance materials emphasizing prudent resource deployment without engaging in dividend payouts or share repurchases amid sustained loss-making periods [S13],[S14],[S17],[S23].

Return on equity remains deeply negative at about -82%, reflecting cumulative net losses eroding shareholder base value despite incremental operating improvements [F1]. Free cash flow remains negative around $-6.5 million when accounting for capex reductions but is trending favorably compared to significantly larger outflows in recent years—indicating slow progress toward positive cash generation fundamentals.

Key Milestones to Watch in 2026 – Outlook and Risks

Looking forward into calendar year 2026, several critical performance indicators warrant monitoring:

- Adjustments or rationalizations of international tariffs impacting input costs or customer pricing flexibility remain pivotal uncertainties capable of materially swinging earnings outcomes [N1],[N2],[S2].

- Conversion rates of the existing sales backlog into recognized revenue will provide insight into commercial momentum recovery prospects amid ongoing industry headwinds.

- Progression of innovation solutions through commercialization phases could catalyze fresh revenue streams if successfully aligned with growing environmental regulation demands.

- Cash flow trajectory modifications including potential financing activity or working capital shifts would reveal management’s agility handling liquidity headwinds.

Geopolitical trade risk continues to dominate the operational outlook given global friction levels—implying that investors must closely watch not only corporate fundamentals but also broader macroeconomic developments shaping tariff landscapes [S4],[S6].

This analysis synthesizes audited financial data alongside recent regulatory disclosures and earnings commentary to present an integrated view of LiqTech International’s current situation without offering investment advice or predictions regarding future stock performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments