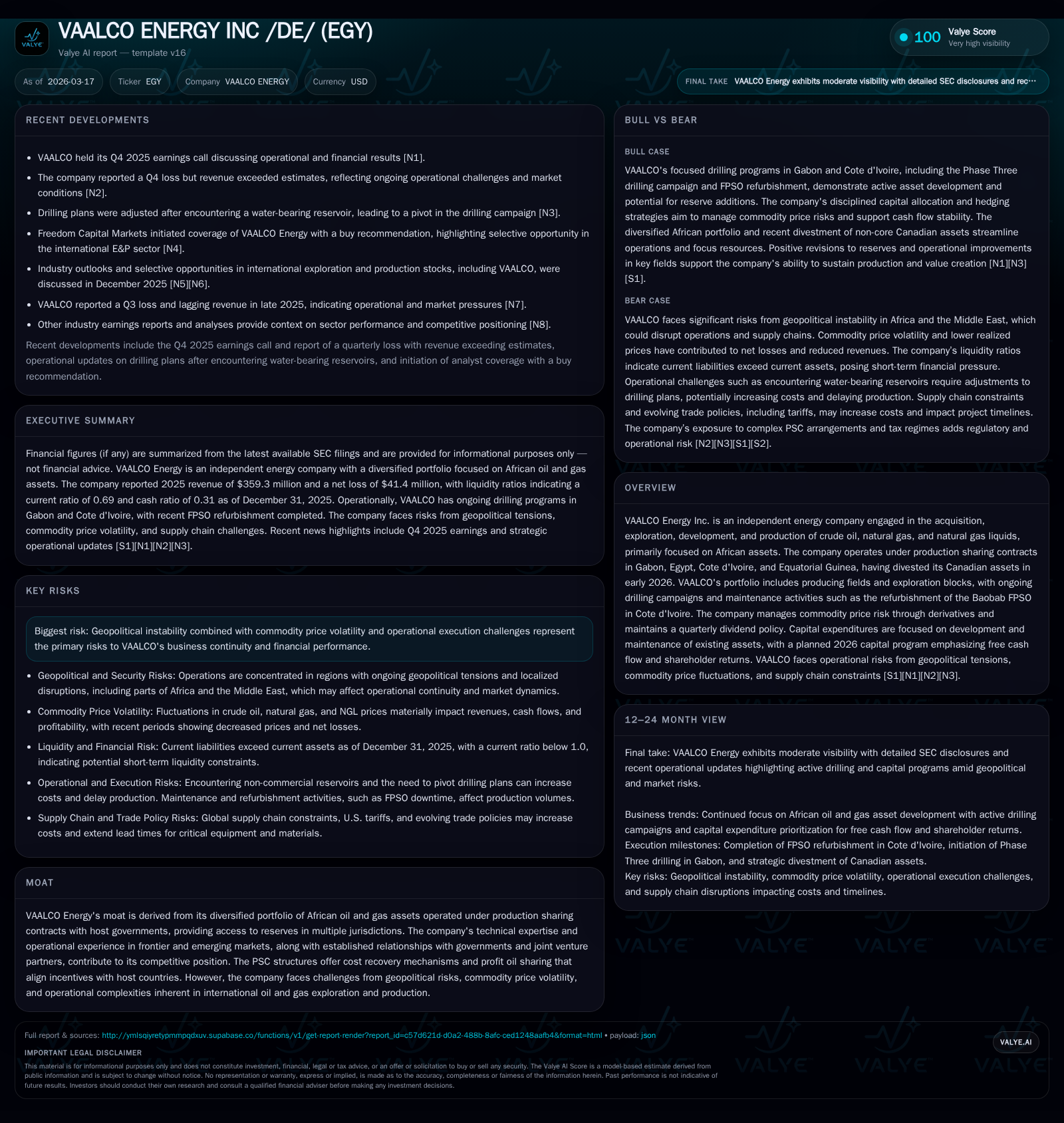

VAALCO Energy’s Shift to African Core Amid Canada Divestment and Capital Discipline

VAALCO Energy pursues organic growth and shareholder returns through focused African operations and controlled capital spending.

VAALCO Energy Inc. has refocused exclusively on African oil and gas assets after divesting its Canadian operations in early 2026. The company reported a significant revenue decline in 2025 driven by lower production volumes and commodity prices, alongside an operating loss primarily due to impairments and restructuring costs. Despite these headwinds, VAALCO is investing heavily in development programs across Gabon, Côte d'Ivoire, Egypt, and Equatorial Guinea with a sizeable capital budget planned for 2026 that prioritizes free cash flow and dividend distributions. Operational execution risks remain elevated given geopolitical tensions in its main operating regions, but the company's portfolio under production sharing contracts provides contractual protections and aligns incentives with host governments.

Historical Performance and Growth Drivers

VAALCO Energy operated both African and Canadian upstream oil & gas assets until early 2026 when it completed the divestiture of its Canadian portfolio for an adjusted price of approximately $25.5 million [S1][S21]. Historically, the Canadian segment contributed modest production volumes but faced recent impairment losses due to sustained declines in forward strip prices which significantly impacted the disposal valuation [S11].

Over the last three years (2023-2025), VAALCO's revenues showed volatility linked predominantly to fluctuations in production volume and global commodity prices ([F1]). Production volumes dropped by about 17% year-over-year from 7.3 million Boe in 2024 to approximately 6.0 million Boe in 2025, compounded by a roughly 14% decline in realized commodity prices per Boe ($65.64 to $56.11) [F1][S19]. These factors resulted in a revenue decrease from nearly $479 million in FY24 to about $359 million in FY25.

The fall in revenue combined with a large impairment charge on assets held for sale ($67.2 million) led VAALCO into an operating loss of ~$20.6 million and a net loss of over $41 million for FY25—reversing profitability achieved previously (net income of $58 million FY24) [F1][S19]. Despite this near-term softness, the company sustained robust operating cash flow generation at $213 million (up 87% YoY) supported by favorable movements in working capital components [F1][S11]. Capital expenditures totaled approximately $236 million in 2025 with major investments across key African producing regions including Egypt, Gabon, and Côte d'Ivoire [F1][S17][S23].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 359 | -41 | 213 | -21 | -25.0% | -170.8% |

| 2024 | 479 | 58 | 114 | 136 | +5.3% | -3.1% |

| 2023 | 455 | 60 | 224 | 159 | +4524.2% | +16.3% |

| 2022 | 10 | 52 | 129 | 171 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 26 | 1 | -9.3 |

| 2024 | 26 | 7 | 11.7 |

| 2023 | 27 | 24 | 12.6 |

| 2022 | 9 | 4 | 11.1 |

Source: SEC companyfacts cache [F1].

Operating cash flow excludes changes in working capital; dividends are consistent while buybacks taper significantly.

Business Portfolio and Strategic Focus

Following the Canada divestiture, VAALCO's asset portfolio is concentrated entirely on Africa comprising producing fields and exploration opportunities located offshore/inshore Gabon (Etame Marin block operator), Côte d'Ivoire (CI-40 block operator plus recent CI-705 acquisition), Egypt (under the Merged Concession Agreement with EGPC), Equatorial Guinea, and Nigeria [S1][S26]. The company operates primarily under Production Sharing Contracts (PSCs) which provide mechanisms for cost recovery before profit oil sharing with governments—a structural advantage offering some insulation against price volatility but exposing operational complexity.

Notably, the Phase Three drilling campaign commenced at Etame Marin block starting late 2025 with partial success amid water-bearing zones encountered requiring sidetrack adjustments [N3][S17]. In Côte d'Ivoire, VAALCO completed the Baobab FPSO refurbishment ahead of schedule with re-commissioning slated for Q2-2026 which is critical for resuming production following an offline period impacting revenues [S10]. The company's entry as operator with a farm-in to CI-705 block offshore Côte d'Ivoire represents strategic expansion adjacent to existing fields [S21].

Future Growth Prospects

Growth catalysts hinge on operational execution of multi-well drilling programs across Gabon, Egypt developments under the Merged Concession Agreement requiring minimum work commitments met as of end-2025, successful FPSO redeployment in Côte d'Ivoire resuming production mid-2026, and exploration upside from new seismic campaigns under BWE Consortium partnership on Niosi Marin and Guduma Marin blocks [S17][S23].

However, growth could be capped by geopolitical risks including ongoing regional tensions impacting supply chains primarily around Eastern Mediterranean affecting Egyptian fields [S1][S16], commodity price volatility—a systemic challenge despite hedging programs utilizing collars/swaps with major counterparties like Glencore—and operational setbacks such as earlier drilling challenges needing adaptive strategies [N3][S15]. Additionally, PSC provisions including consent requirements for asset transfers may impede swift capital redeployment or acquisitions within current territories [S13][S14].

Capital Allocation and Returns

Capital discipline is central to VAALCO’s strategy moving forward with planned capex between $290 million to $360 million targeting primarily oil & gas development activities: notably $110–135 million for Gabon, $170–210 million for Côte d'Ivoire development including post-FPSO refurbishment ramp up, $9–12 million for Egypt projects, plus minimal spend for Equatorial Guinea and corporate costs [S1][S21]. This outlook underscores an emphasis on organic reserve growth balanced with free cash flow generation.

The company’s strong operating cash inflows coupled with modest capex spending has enabled meaningful shareholder returns via dividends maintained quarterly at an expected rate of $0.0625/share since Q1-2023 aggregating near $26–27 million annually [S12], while share repurchases have declined materially reflecting shifting focus or liquidity management.

Approximate ROE slipped into negative territory at about -9% for FY25 driven by net losses despite solid equity levels above $443 million reflecting retained earnings buffer [F1]. Sustaining positive returns will depend heavily on successful project executions enabling improved profitability beyond volatile short-term pricing conditions.

Operational Risks and External Factors

The primary risks remain geopolitical instability within operating regions—localized conflicts can disrupt operations or logistics—and ongoing global trade tensions including tariffs increasing equipment procurement costs or lead times as noted regarding U.S.-imposed duties on energy-related industrial goods affecting supply chains routed through Houston hubs where VAALCO is headquartered [S15][S16]. Commodity price risk is partly mitigated by derivative hedging instruments but remains a potent factor influencing earnings variability.

Additionally, environmental obligations including asset retirement costs require continual funding adherence under PSC terms monitored by government authorities—estimated abandonment obligations nearing ~$78 million undiscounted nationally within Gabon reflecting extended decommissioning commitments [S23]. Compliance complexities linked to expanded regulatory scrutiny also necessitate elevated internal governance resources.

What To Watch (Analysis)

Key indicators moving forward include first-half production recovery rates post-FPSO maintenance especially from Côte d’Ivoire fields; drilling outcomes from Gabon Phase Three program’s sidetracked wells; integration progress within newly farmed CI-705 block; trends in commodity prices notably Brent crude linked global benchmark; hedging effectiveness extending through March/December 2027 coverage horizons; adherence to capital expenditure targets aligned with free cash flow generation; dividend sustainability amidst operational volatility; potential further divestitures or acquisitions activity given stringent PSC assignment restrictions; plus monitoring geopolitical developments affecting regional stability.

Summary

VAALCO Energy has decisively transitioned into a pure-play African upstream energy company after exiting Canada early in 2026 underpinning efforts focused on project development and reserve base expansion underpinned by PSC frameworks balanced against political complexity inherent to frontier markets. The revenue and earnings contraction experienced recently owes chiefly to cyclical commodity winds tempered partially by rigorous operational cash flow management enabling ongoing capital investment programs coupled with shareholder-friendly dividend policy.

How effectively VAALCO navigates technical challenges such as water-bearing reservoirs encountered during drilling campaigns while leveraging infrastructure upgrades like FPSO refurbishments will be pivotal points determining near-term growth momentum as it continues risk mitigation measures amidst geopolitical uncertainties affecting its core field areas.

This analysis is based solely on available financial statements filings dated March 16, 2026 ([F1],[S1]-[S29]) supplemented by related earnings releases ([N1]-[N3]) without making investment recommendations or forecasts beyond provided disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments