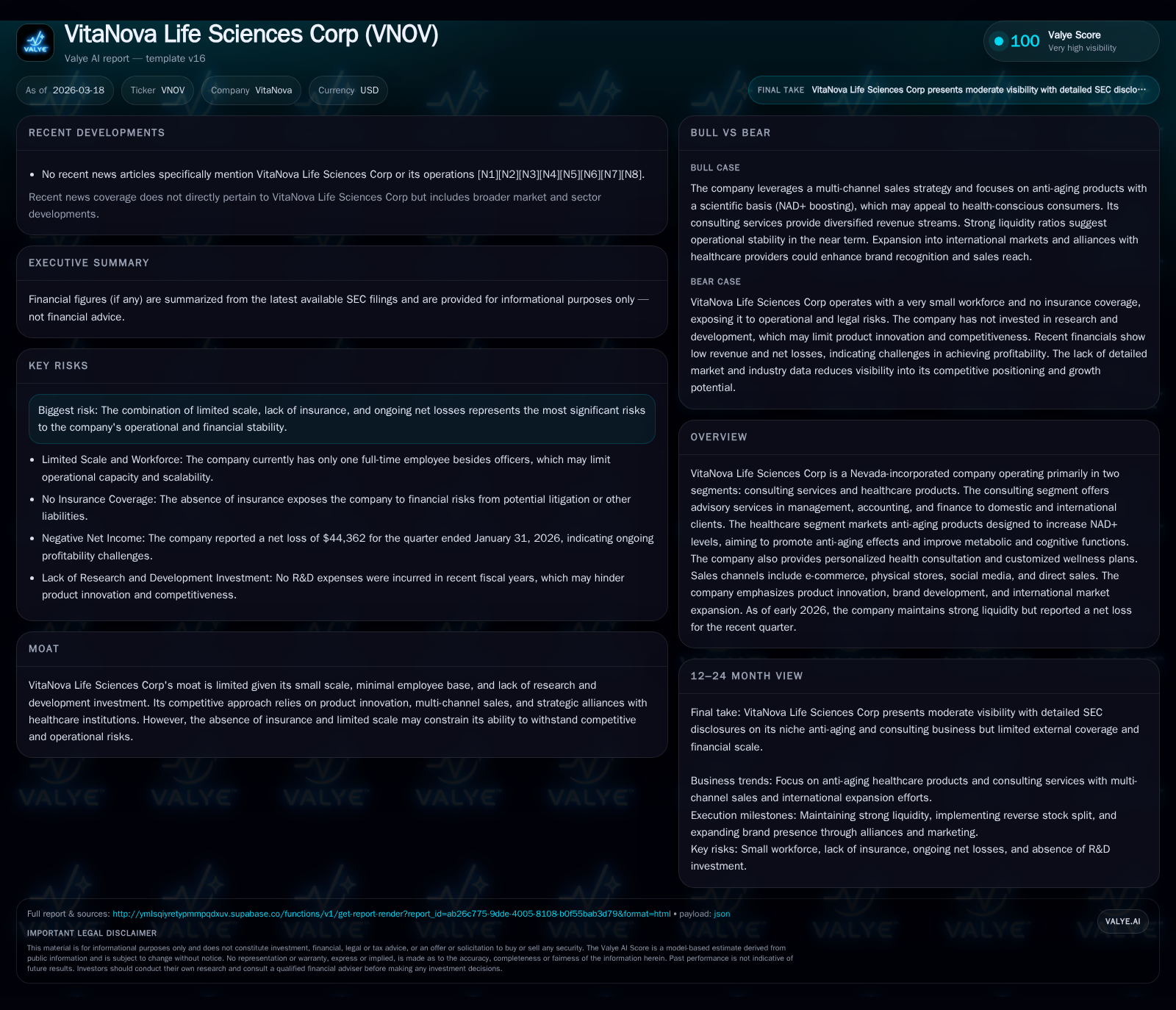

VitaNova Life Sciences' Strategic Pivot in Health and Consulting Markets

VitaNova Life Sciences evolves its dual-segment operations to counter scale limitations and losses, leveraging innovation and multi-channel sales.

VitaNova Life Sciences Corp, originally operating at losses with limited scale, achieved a striking turnaround with a 487.6% increase in operating income by FY2025 despite a sharp 68.3% revenue decline. The company’s business spans consulting advisory services and anti-aging healthcare products focused on NAD+ level enhancement, marketed via a diverse multi-channel strategy including e-commerce, physical retail, and direct sales. While operational leverage and margin expansion have driven recent profitability gains, growth is tempered by scale constraints, absence of insurance coverage, and reliance on brand development rather than R&D. Monitoring international expansion progress and sustaining cash flows will be crucial for VitaNova's future trajectory.

From Startup Losses to Positive Operating Income: Historical Growth Trajectory

VitaNova Life Sciences Corp’s financial journey reflects early-stage volatility marked by sharp swings between losses and profitability gains within a condensed timeframe. The fiscal years ending April 30 illustrate this contrast:

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 850746 | 192774 | 1208314 | +503.9% | ||

| 2024 | 140865 | -375880 | 205629 | +681.4% | ||

| 2023 | 38000 | -24227 | -18375 | -24227 | -68.3% | -117.3% |

| 2022 | 120000 | 139682 | 4061 | -13367 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 44.6 |

| 2024 | 13.3 |

| 2023 | 40.9 |

| 2022 | -399.2 |

Source: SEC companyfacts cache [F1].

Revenue figures for FY2024-25 are not explicitly detailed but the precipitous fall of revenue between FY2022 and FY2023 (-68.3%) is notable [F1]. This contrasts with an extraordinary rebound in operating income by nearly fivefold from FY2024 to FY2025 (+487.6%), marking an inflection point from prior losses to substantive profitability.

Net income follows this pattern with a similar magnitude change (+503.9%), while operating cash flow reversed from deep negative in FY2024 to positive territory in FY2025 (+151.3%). These dynamics indicate effective operational leverage despite revenue contraction. Equity rose accordingly reflecting accumulated earnings [F1].

This trajectory underscores an underlying paradox seen in some startups: shrinking top-line juxtaposed with expanding profitability driven largely by margin improvements rather than topline growth.

Dual-Segment Business Model: Consulting and Anti-Aging Healthcare Products

VitaNova operates two main segments: consulting advisory services in management business practices as well as accounting and finance across domestic and international clients; alongside healthcare products focused on anti-aging solutions designed to increase intracellular NAD+ levels—a biochemical target linked with cellular repair and metabolic enhancement [S4][S5].

Complementing product sales are personalized health consultations offering tailored wellness plans based on customers' physical conditions and lifestyles [S5].

Distribution channels include e-commerce platforms (company website plus third-party sites), brick-and-mortar stores for physical retail presence, social media engagement for brand awareness, and direct sales approaches fostering customer relationships [S4][S5].

Competitive positioning relies heavily on continuous product innovation through marketing efforts rather than formal R&D investment; brand building is pursued via advertising campaigns, trade show participation, public welfare sponsorships, and strategic partnerships with hospitals and clinics [S4]. Pricing flexibility through promotions such as coupons and discounts supports customer acquisition amid intense competition.

Operational Leverage and Margin Expansion Driving Profitability Gains

The sharp acceleration in operating income amid declining revenues reflects operational leverage effects typical when fixed costs dominate variable expenses—accentuated here by lean staffing of only one full-time employee beyond officers [S4].

Notably absent are research & development expenditures that often burden life sciences companies; this absence constrains scientific innovation but aids near-term margin expansion [S4].

Such financial discipline allowed absorption of fixed overhead over reduced revenue bases without pushing losses deeper but generating scalable profit growth.

Net income gains mirror these effects along with possible favorable non-operating items contributing positively as seen in the switch from net loss to substantial profit within two years [F1][S1]. This leanness also reflects the knowledge-intensive nature of consulting services relative to capital intensity.

Nonetheless operational scalability remains constrained due to minimal human capital resources limiting broader client servicing or product pipeline development.

Key Drivers Behind Volatile Revenue Trends and Customer Acquisition Strategies

Revenue volatility—particularly the slide from $120k in FY2022 down to $38k in FY2023—is tied not only to demand fluctuations but also strategic pricing aimed at market penetration under intense sector competition [F1][S4][S5].

Flexible pricing regimes involving promotions like coupons target price-sensitive consumers; while necessary for early traction such strategies can suppress top-line growth or elongate profitable volume ramp-up periods.

Multi-channel sales efforts span online portals optimizing digital reach combined with offline presence through physical stores; social media platforms enhance brand visibility engaging health-conscious demographics accustomed to influencer recommendations typical in wellness industries.

These factors reflect an attempt to address fragmented consumer demand patterns but expose top-line growth sensitivity due to competitive discounting pressure.

Brand development expenditures accompanying these moves have yet to translate into consistent scaled revenue streams which could cap near-term growth potential absent alternative acquisition vectors [S4].

Future Outlook: Innovation Focus and International Expansion Amid Competitive Risks

While VitaNova emphasizes continued product innovation it has no recorded R&D expenses suggesting innovation efforts are largely marketing-based or incremental improvements within existing formulations rather than disruptive breakthroughs [S4]. This positions the firm more as a consumer health brand than a traditional pharmaceutical developer.

International expansion represents a core growth pillar intended to diversify reliance on domestic markets but involves execution complexity especially under resource constraints.

Strategic alliances forged with health entities may aid access but competition remains fierce from established nutraceutical players and emerging digital-native brands.

The company does not require government regulatory approvals easing commercialization hurdles but lacks insurance coverage adding operational risk [S4].

Growth depends heavily on successful brand building aligned with global anti-aging consumer trends while managing thin structural defenses versus competitive encroachments.

Capital Structure and Shareholder Returns: Navigating Thin Liquidity but No Dividends

Recent governance maneuvers include a reverse stock split at a ratio of 1-for-3 implemented January 2026 alongside increases in authorized common stock shares up to 200 million plus creation of preferred stock classes enhancing funding flexibility [S11][S13]. These moves typically serve purposes of improving share price stability or preparing capital raise initiatives.

Cash reserves remain modest but sufficient given low operational burn rates; end-of-period current ratio stood robustly at approximately 5.05 indicating substantial short-term asset coverage over liabilities [F1][S16].

No dividends or share repurchase programs exist reflecting retention of capital for reinvestment or operational support rather than shareholder distribution [S11][S13].

Approximate return on equity surged impressively to about 44.6% in latest fiscal year capturing efficient equity utilization albeit off very small equity bases characteristic of early-stage entities [F1]. This signals profitable scaling within invested capital thus far.

Risk Factors: Limited Scale, Insurance Gaps, and Litigation Exposures

A defining vulnerability is VitaNova’s constrained headcount comprising one full-time employee beyond officers limiting capacity for scaling operations or enforcing rigorous quality controls expected in healthcare domains [S4].

More critical is the complete absence of any insurance policies shielding against liability risks inherent when marketing health-related products—a rare exposure uncommon among healthcare firms where insurance is standard practice—even if not mandatory here [S4][S6].

No material litigation proceedings are currently pending per filings but uninsured status remains an unusual risk factor potentially threatening ongoing operations if legal actions arise.

Scale limitations restrict competitive positioning against larger nutraceutical or biotech rivals possessing deeper pockets for product development or marketing diffusion.

What Investors Should Monitor Next: Market Expansion Execution and Cash Flow Sustainability

Key indicators for investors include:

- Progress on international expansion gauged through disclosures reflecting increased foreign sales penetration.

- Ability to stabilize or grow revenues beyond promotional dependency signaling underlying demand strength.

- Operating cash flow trends sustaining positive liquidity allowing flexibility without dilutive financing.

- Any new product launches or consulting diversification broadening revenue mix easing concentration risks.

- Corporate actions signaling shifts in capital allocation priorities around funding innovation or partnerships enhancing competitive moat.

- Developments regarding adoption of insurance policies reducing legal risk exposure improving governance standards. These factors collectively illuminate VitaNova’s path balancing innovation-driven brand building against financial discipline essential for sustainable growth outside traditional heavy R&D models.

This report synthesizes VitaNova Life Sciences Corp's SEC filings ([S#]) alongside numeric financial evidence ([F1]) up to early 2026 without projecting unconfirmed clinical developments or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments