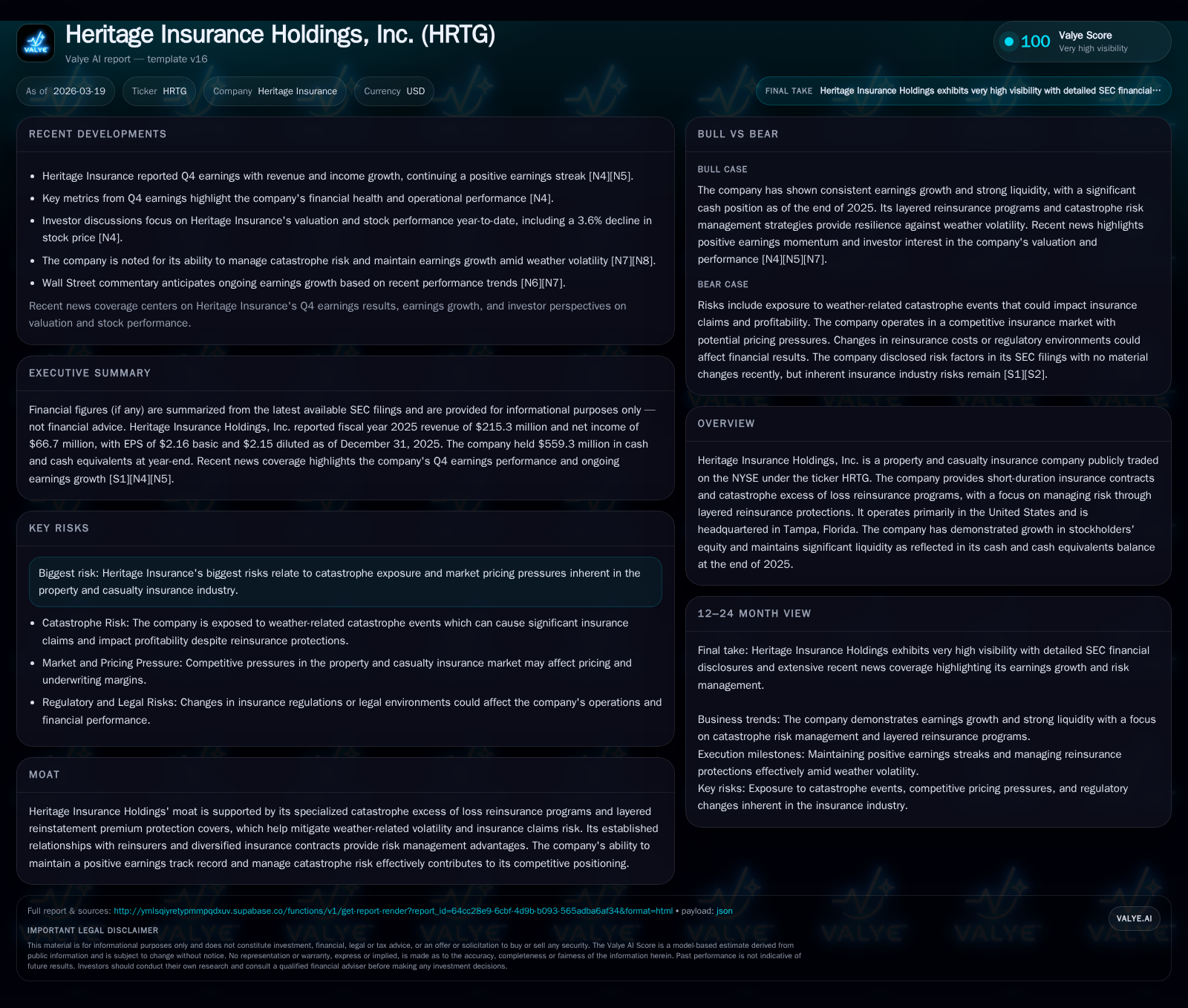

Heritage Insurance Holdings Conquers Catastrophe Risk with Reinsurance Innovation

The company leverages layered catastrophe excess of loss reinsurance and reinstatement premium protections to enhance financial resilience and equity growth.

Heritage Insurance Holdings has built consistent growth through innovative catastrophe risk management, utilizing multi-layered reinsurance structures that have stabilized underwriting performance amid volatile property and casualty markets. The company's 2025 results reflect strong top-line progression combined with outsized operating and net income expansion, supported by substantial cash flow generation and solid return on equity. While market pricing pressures remain a risk, Heritage’s disciplined underwriting and diverse reinsurer relationships underpin its competitive moat. Liquidity and capital structure remain robust, positioning the company for measured growth despite inherent catastrophe exposure.

Strong Historical Growth Anchored by Reinsurance Expertise

Heritage Insurance Holdings has demonstrated steady top-line momentum over the recent four-year span, with revenues advancing from approximately $174.6 million in fiscal year 2022 to over $215.3 million in fiscal year 2025, representing a compounded annual growth trajectory augmented by focused underwriting discipline (see [F1]). Notably, the company achieved a 2.4% year-over-year revenue increase during 2025 alone amid challenging P&C industry dynamics.

This steady revenue expansion belies a more pronounced operational leverage: operating income leapt from about $14.9 million in 2022 to nearly $89.7 million in 2025 — an impressive increase of roughly 184.5% year-over-year in the most recent period (see [F1]). This disparity between top-line growth and operating profit reflects Heritage’s success in optimizing underwriting margins through its specialized risk mitigation frameworks.

Net income mirrored this trend, soaring from just over $20 million in 2024 to nearly $66.7 million in 2025 — a gain of approximately 228.6% year-over-year (see [F1]). This performance underscores effective catastrophe risk management and cost controls that have helped stabilize earnings despite exposure to weather-related volatility inherent to property casualty insurance.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 215 | 67 | 182 | 90 | +2.4% | +228.6% |

| 2024 | 210 | 20 | 87 | 32 | +12.5% | -34.4% |

| 2023 | 187 | 31 | 70 | 36 | +7.1% | |

| 2022 | 175 | -34 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 174 | ||

| 2024 | 0 | 79 | |

| 2023 | 0 | 0 | 61 |

| 2022 | 5 | 7 | -36 |

Source: SEC companyfacts cache [F1].

The surge in operating income alongside modest revenue growth signals sizeable improvement in underwriting efficiency attributed largely to innovative reinsurance structures.

Assessing the Influence of Catastrophe Programs on Operating Performance

Fundamental to Heritage’s operating prowess is its sophisticated catastrophe excess of loss reinsurance program coupled with layered reinstatement premium protection covers . These constructs are designed to limit first-loss exposure per event while enabling multi-event protection within a policy year through triggering reinstatement premiums upon claims.

Layered catastrophe excess of loss coverage entails transferring losses above certain retention thresholds across multiple strata to reinsurers, effectively capping maximum net retained losses per event or aggregate periods [S1]. The reinstatement premium protection further buffers against unexpected increase in losses during successive catastrophes by requiring premium payments from reinsurers for each layer recovery — thereby limiting Heritage's gross retention spikes.

By structuring these protects as multi-layered and tailored excess of loss retrocessions with well-established reinsurers, Heritage stabilizes loss experience volatility typical of P&C insurers with hurricane and weather-related liabilities [N9]. This stable loss evolution supports tighter underwriting margins.

In industry parlance, this approach reduces earnings volatility stemming from single catastrophic occurrences while enabling sustainable profitability across underwriting cycles — an advantage reinforced by Heritage’s longstanding reinsurer institutional relationships facilitating favorable contract terms .

2025 Financial Snapshot: Marked Earnings and Equity Expansion

The fiscal year ended December 31, 2025 was notable for pronounced financial strength across multiple metrics:

- Net income reached $66.7 million, over three times its level two years prior ([F1]).

- Operating cash flow vaulted to $182 million accompanied by conservative capital expenditures ($8.1 million), yielding free cash flow around $174 million — a level indicative of robust internal capital generation capacity ([F1]).

- Shareholders' equity expanded sharply from $291 million at end-2024 to approximately $505 million at end-2025 — roughly a +74% surge reflecting net profits retained within the business (see [F1]).

- The consequent return on equity approximated a healthy ~13.2%, attesting to effective capital deployment amid insurance risk-retention strategy ([F1]).

These figures depict an insurer efficiently converting underwriting gains into sustained balance sheet augmentation without resorting heavily to external capital infusions.

Navigating Market Pricing Pressures and Underwriting Discipline

The property & casualty insurance sector is notoriously cyclical, experiencing periods where intense competition compresses pricing — forcing insurers like Heritage to apply strict underwriting criteria or bear margin erosion risks [S5][S6].

Heritage acknowledges that pricing pressure is among its principal threats alongside inherent catastrophe exposure variability [S5]. Compounding this is the sector’s sensitivity to regional hazard shifts impacting expected loss probabilities.

However, Heritage's focused geographic footprint and niche product offerings enable nuanced pricing models exploiting actuarial insights unique to its markets [N14]. The company’s ongoing commitment to disciplined underwriting standards acts as a counterweight against commoditization threats.

Hence, while headline price challenges exist, Heritage seeks offsetting benefits via selective policy issuance aligned with its reinsurance protections—ensuring earned premiums adequately reflect assumed risks amidst evolving market dynamics [S6].

Evaluating Capital Allocation: Cash Flows, Buybacks, and Return on Equity

In its capital strategy, Heritage demonstrates prioritization of balance sheet strength over shareholder distributions.

Dividend payments have been nominal recently (only $11K paid in FY2023; none indicated thereafter per [F1]), reflective of cautious preservation stance given catastrophe risk environment.

Share repurchases ceased entirely after fiscal year 2022 when modest buybacks near $7.3 million occurred; no repurchases reported beyond that (see [F1]). This restraint suggests capital allocation geared toward natural organic growth financing rather than aggressive return enhancements via repurchases.

Robust operating cash flows generated annually fuel strong reinvestment potential while sustaining conservative leverage metrics (discussed below), collectively underpinning an efficient ROE near double digits backed by profitable core operations ([F1]).

This measured approach acknowledges the episodic nature of claim payouts typical in P&C lines while maintaining flexibility for opportunistic future deployments if conditions merit.

Liquidity Strength and Debt Position Amidst Cat Risk Exposures

Liquidity is a cornerstone amid heavy reinsurance engagement; Heritage reported cash & cash equivalents exceeding $559 million at December 31, 2025 — ample relative to annual premiums written ([F1]).

Supplementing liquid assets are committed credit facilities comprising revolving credit lines and senior secured loans structured under amended agreements protecting against draw restrictions triggered by adverse loss development or covenant breaches [S7][S8][S9][S10]. These debt instruments include variable rate components indexed largely to SOFR plus defined spreads ensuring market competitiveness yet balanced cost containment.

Additionally noted are borrowings from Federal Home Loan Banks which provide collateralized liquidity cushions supporting day-to-day operations even under stress scenarios ([S17][S18][S19]).

This diversified credit profile combined with conservative liability structuring positions Heritage well for navigating large cat loss events without compromising solvency or operational continuity.

Forward Expectations: Revenue Drivers and Potential Constraints

While explicit company guidance remains absent (typical in filings reviewed), management commentary coupled with analyst expectations signal cautious optimism for top-line expansion driven by:

- Continued policy renewals underpinned by disciplined price adequacy ensuring margin preservation [N8].

- Targeted new business volume expansions leveraging brand recognition within core geographies.

- Sustained effectiveness of layered catastrophe programs curtailing net loss volatility bolstering profitability forecasts [N9].

Conversely evident risks include potential degradation of market terms amid cyclical softening pressures or heightened cat event frequency/severity elevating incurred costs surpassing current reinsurance cushions [N13].

Overall thematic view posits monitoring emerging trends closely alongside reinsurance market evolutions as critical determinants shaping near-term revenue/earnings trajectories.

What Investors Should Monitor Next

For stakeholders tracking Heritage Insurance Holdings' progression, several key indicators warrant close attention:

- Quarterly underwriting results consistency assessed through combined ratio trends reflecting claims frequency/intensity versus earned premiums [N9].

- Evolving patterns in catastrophe occurrence impacting triggering frequencies for layered reinstatement premiums—directly influencing net retained losses and margin stability.

- Renewal timing and terms for major catastrophe excess loss programs offering insight into cost structure adjustments or coverage expansions/reductions ahead.

- Regulatory changes relevant to Florida-focused insurers given their material impact on operational frameworks though currently stable as per filings [S5][S6].

- Capital allocation decisions including any shifts towards dividends or share buybacks indicating confidence levels regarding future earnings visibility.

Such factors collectively capture the core mechanics driving valuation underpinnings beyond headline earnings beats recorded recently [N14]. Vigilant reassessment aligned with operational updates can sharpen perspectives on the durability of Heritage’s competitive advantages amidst industry cyclicality.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available data as cited without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments