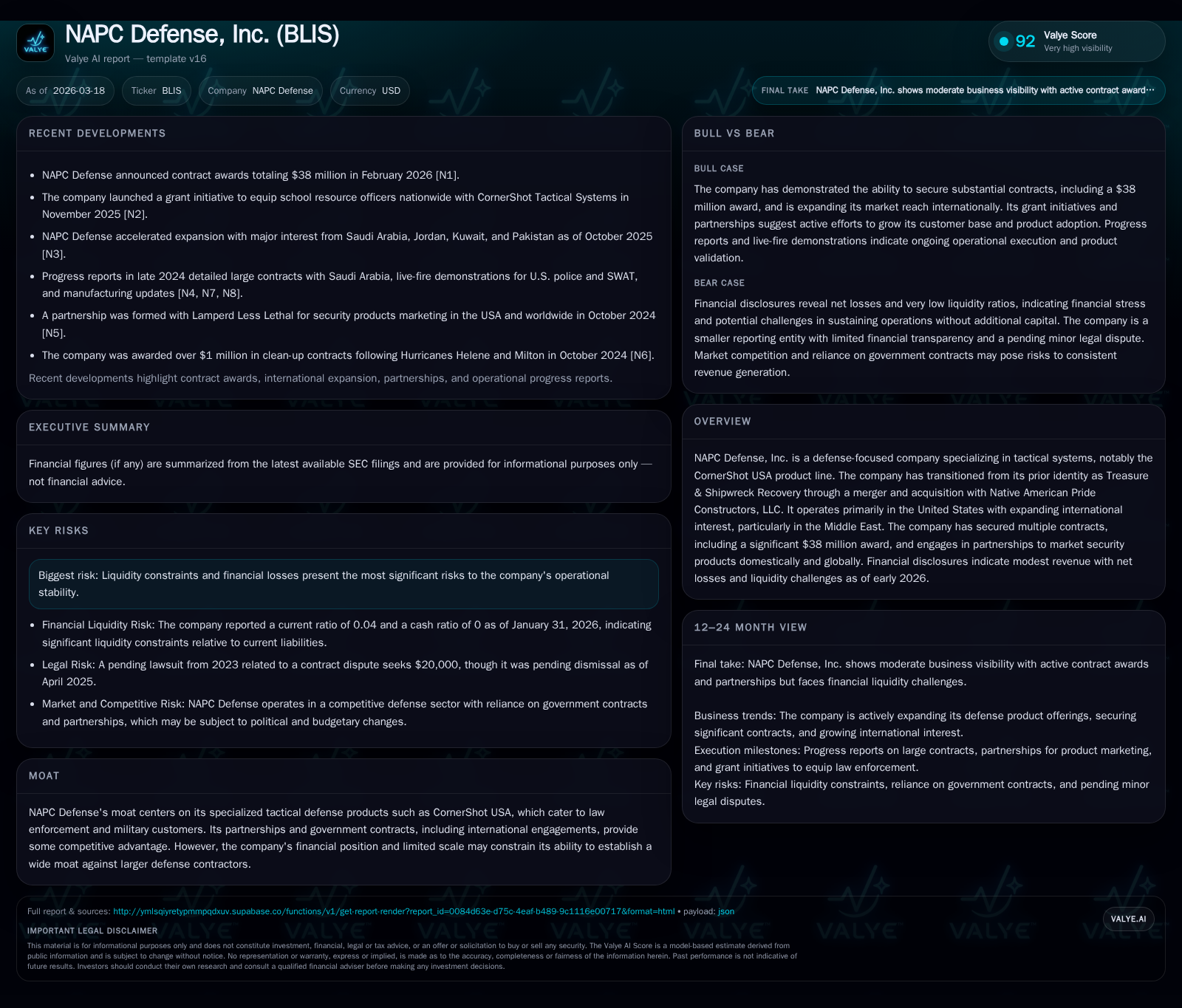

CornerShot USA Powers NAPC Defense’s Tactical Expansion and Capital Challenges

NAPC Defense leverages its niche tactical product lines and recent multi-million-dollar contracts while contending with significant liquidity shortages and operational losses.

NAPC Defense, Inc. has secured $38 million in contracts highlighting demand for its CornerShot USA tactical products. Despite stable revenues near $85,000, operating losses widened sharply to nearly $2.5 million in fiscal 2025, reflecting increased expenses amid limited sales growth. The company faces severe liquidity constraints with a current ratio around 0.04 and negative equity but has taken corporate actions including expanding authorized shares and creating a Voting Control Preferred stock class to maintain governance control during strategic initiatives. International expansion and school safety advocacy complement commercial prospects, yet financial stability remains a key challenge.

Historical Revenue and Operating Performance

NAPC Defense has shown relatively stable revenue of approximately $85,000 during fiscal years ending April 30, 2023 and 2024, indicative of steady but limited top-line traction within its niche tactical defense market [F1]. However, operating income deteriorated sharply from -$583,720 in FY2024 to -$2,484,960 in FY2025, signaling escalating costs likely due to increased R&D, marketing efforts tied to contract pursuits, or product development expenses without proportional revenue gains.

Net income followed a similar trajectory, worsening from -$711,986 in FY2024 to -$3,376,999 in FY2025, underscoring profitability challenges common among emerging defense contractors navigating early-stage contract ramp-up phases [F1]. Negative operating cash flow expanded from -$340,738 in FY2024 to -$797,225 in FY2025 with no recent capex increases recorded, reflecting operational cash burn rather than investment spikes.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -3 | -797225 | -2 | -374.3% | ||

| 2024 | 85000 | -1 | -340738 | -1 | 0.0% | +24.3% |

| 2023 | 85000 | -1 | -424056 | 0 | +54.5% | |

| 2022 | -2 | -613758 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 294.5 |

| 2024 | -99.6 |

| 2023 | 117.8 |

| 2022 | 237.6 |

Source: SEC companyfacts cache [F1].

Table: NAPC Defense Historic Financial Summary (in USD)

This financial profile illustrates the typical "runway compression" scenario where companies face increasing liquidity pressures while investing upfront for future contract fulfillment.

Contract Awards and Growth Prospects

In February 2026, NAPC Defense announced contract awards totaling $38 million related to its CornerShot USA product line [N1]. This sizable backlog represents a substantial increase compared to historical revenues and highlights institutional confidence in the company’s tactical defense technologies across law enforcement and military applications.

Successful execution of these contracts will be critical for translating backlog into recognized revenue growth. However, such conversion depends on effective program delivery timelines and sustained procurement activity.

International Expansion and School Safety Initiatives

The company is actively pursuing international partnerships focused on Middle Eastern security markets [N2], aiming to diversify beyond domestic government contracts. Concurrently, NAPC Defense advocates for CornerShot USA’s role in school safety via engagements with Congress members and presentations at NASRO events dedicated to school resource officers [N2][N3].

These efforts may open new commercial avenues but also introduce complexities related to export regulations and geopolitical risks.

Financial Position and Capital Structure

As of January 31, 2026, NAPC Defense reported current assets of approximately $69,166 against current liabilities of about $1.72 million resulting in a current ratio near 0.04—a sign of acute liquidity constraints [F1][S13][S14]. Shareholders’ equity stood negative at roughly -$1.15 million due to accumulated losses [F1].

To address these challenges while supporting growth initiatives, the Board approved an increase in authorized shares from 500 million to 2 billion shares along with the creation of a Voting Control Preferred stock series comprising seventy shares that collectively hold 70% voting power but carry no dividend or liquidation rights [S7][S9][S11].

This capital structure adjustment aims to preserve governance control during potential equity financings or strategic transactions critical for sustaining operations.

Outlook and Monitoring Points

Absent formal guidance disclosures:

- Progress on converting the $38 million contract backlog into revenue will be key for near-term performance;

- Development of international partnerships may diversify revenue but faces regulatory and geopolitical uncertainties;

- School safety advocacy could provide incremental commercial opportunities;

- Liquidity improvement strategies including potential financings will be vital for maintaining operational continuity;

- Upcoming shareholder meetings (e.g., July 1st per [N2]) may reveal strategic updates or recapitalization plans.

Collectively these factors suggest that while NAPC Defense possesses promising product-driven growth potential supported by recent contract wins and market expansion efforts, it must navigate significant financial headwinds requiring disciplined execution and capital management.

This report is prepared solely for informational purposes based on publicly available data sources as noted; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments