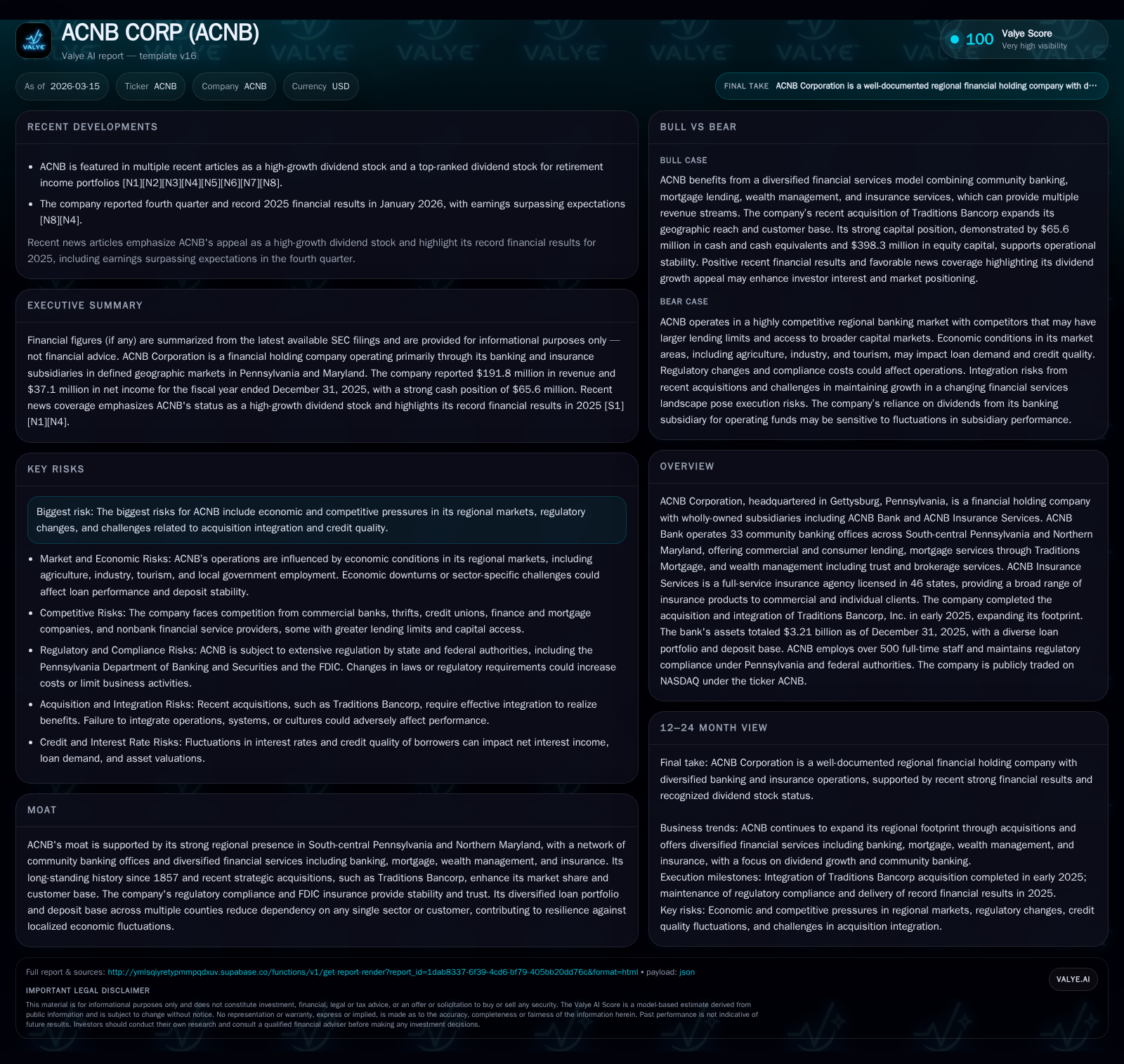

From Community Roots to Expanded Markets: ACNB's Strategic Transformation

ACNB Corporation’s acquisition of Traditions Bancorp and diversification into mortgage and insurance services have reshaped its regional footprint and financial profile while sustaining shareholder returns.

ACNB Corporation, rooted as a community bank since 1857 in Gettysburg, Pennsylvania, underwent a transformational expansion by acquiring Traditions Bancorp in early 2025. This acquisition enhanced its branch network, introduced mortgage operations via Traditions Mortgage, and broadened service offerings to include wealth management and insurance licensed in 46 states. The company's 2025 financials reflect a significant revenue leap driven by acquisition and organic growth, supporting increased dividends and share repurchases. With assets surpassing $3.2 billion and a diversified loan portfolio across multiple sectors in its core regional market, ACNB balances growth prospects with the challenges of integration, credit quality, and regulatory changes.

Heritage and Historical Growth: From Local Bank to Regional Player

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 192 | 37 | 54 | 1076000 | +45.1% | +16.3% |

| 2024 | 132 | 32 | 40 | 960000 | +0.5% | |

| 2023 | 32 | 41 | 1168000 | -11.4% | ||

| 2022 | 36 | 39 | 1811000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 14 | 11 | 53 |

| 2024 | 11 | 0 | 39 |

| 2023 | 10 | 2 | 39 |

| 2022 | 9 | 7 | 37 |

Source: SEC companyfacts cache [F1].

ACNB Corporation traces its origins back to 1857 as a community bank headquartered in Gettysburg, Pennsylvania. It has cultivated a strong presence across South-central Pennsylvania and Northern Maryland with an emphasis on commercial and consumer banking tied closely to local economies such as agriculture, education, healthcare, tourism, and local government sectors [S1; S4]. This foundation established ACNB as a trusted institution with deep community relationships.

Before recent acquisitions, ACNB exhibited steady financial growth with revenues at $132.2 million in FY2024 and net incomes consistently near $31–36 million from FY2022 through FY2024 [F1]. Its diversified loan portfolio spans commercial real estate projects, construction financing, consumer loans including home equity lines of credit (HELOCs), and business loans tailored for regional market needs [S7]. The bank's footprint included offices primarily in key counties such as Adams, York, Cumberland in Pennsylvania plus Carroll and Frederick Counties in Maryland.

Acquisition Impact: Integrating Traditions Bancorp and Expanding Footprint

The strategic expansion came with the acquisition of Traditions Bancorp effective February 1st, 2025 [S1; S4]. Traditions operated eight community banking offices in South Central Pennsylvania which were consolidated into ACNB’s existing network during Q2 2025 to optimize branch coverage [S4]. This brought total branches to 33.

Besides physical expansion, the acquisition incorporated Traditions Mortgage as a dedicated lending arm focused on residential construction loans and investment mortgages—complementary to ACNB’s traditional banking offerings [S7]. Mortgage production offices enhance origination capabilities beyond standard branch channels.

Operationally, IT systems were integrated while retaining "Traditions Bank" branding for continuity. The acquisition also bolstered cross-selling opportunities among ACNB Wealth Management services and its insurance subsidiary licensed nationally across 46 states [S4].

2025 Financial Performance: Revenue Growth and Profitability

Driven by the acquisition combined with organic growth initiatives across lending and fee-based segments, ACNB reported FY2025 revenue of $191.8 million—a notable increase of approximately 45% year-over-year compared to FY2024 [$132.2M] [F1]. Net income rose over 16% year-on-year to $37.1 million.

Operating cash flow increased nearly 35% to approximately $53.6 million despite integration-related expenses including elevated general costs associated with transaction execution [F1].

The earnings uplift was fueled primarily by increased loan volumes generating higher yields post-acquisition alongside non-interest income streams from mortgage servicing fees via Traditions Mortgage and commissions from the insurance business operating broadly across the U.S. states [N6; N8; S4].

Loan Portfolio and Deposit Base Dynamics Post-Acquisition

As of December 31st, 2025 total assets stood at $3.21 billion with net loans around $2.33 billion after adjustments for unearned income related fees [S4; F1]. The loan portfolio remains diversified:

- Commercial real estate reflecting development projects,

- Expanded residential mortgages through Traditions Mortgage,

- Consumer lending including home equity lines,

- Various commercial loans supporting local businesses [S7; S13; S24].

Deposits totaled approximately $2.48 billion supported by core deposits from a broad client base spanning nine counties across two states [S4; S24]. The region's economic diversity mitigates concentration risk given no single sector dominates employment or commerce.

Loan production offices located strategically in West Lawn (PA) and Hunt Valley (MD) complement branch networks enhancing origination efficiency.

Dividend Strength and Shareholder Returns Amid Growth

Despite capital deployed for acquisition activities, ACNB increased dividends paid by about 34% year-over-year to $14.38 million in FY2025 [F1]. This dividend growth aligns with analyst commentary highlighting ACNB as a compelling high-growth dividend stock within financial services sectors [N4; N7; N1].

Share repurchases accelerated substantially with buybacks totaling $11.16 million in FY2025 versus only about $249k the prior year—reflecting confidence in capital adequacy following the merger [F1]. This disciplined capital return strategy leverages free cash flow generation (approximately $52.57 million calculated as operating cash flow minus capex) without impairing liquidity or solvency metrics.

Capital Structure and Liquidity: Managing Debt and Equity for Expansion

On March 12th, 2026 ACNB issued subordinated notes totaling $15 million bearing a fixed-to-floating rate coupon maturing in March 2036—providing long-term liquidity buffers supporting future growth plans [S3].

Equity capital expanded sharply from roughly $303 million at end-2024 to about $420 million at end-2025 driven by retained earnings retention alongside strategic equity contributions aligned with growth objectives [F1; S4]. This translates into an estimated return on equity near 8.8%, balancing funding needs while delivering returns consistent with peers in regional banking [F1].

Capital expenditures remain modest at around $1.08 million annually for facility upgrades—typical for banks of this scale—ensuring infrastructure keeps pace without excessive spending [F1]. Dividends paid derive mainly from distributions received from the bank subsidiary per regulatory holding company frameworks [S4].

Future Growth Drivers: Navigating Regional Market Opportunities and Risks

ACNB’s core market spans diverse economies across South-central Pennsylvania counties plus Northern Maryland areas characterized by agriculture alongside growing sectors such as healthcare services, tourism linked to historical sites like Gettysburg, educational institutions employing locals—all contributing multifaceted economic drivers supporting stable loan demand over cycles [S24; S4].

The insurance business licensed in forty-six states offers scalability potential beyond geographic confines extending fee income streams somewhat insulated from interest rate fluctuations impacting lending margins.

Risks include evolving federal regulations affecting capital requirements (e.g., Basel III), competitive pressures from larger banks or fintech entrants compressing margins especially on loan products, plus credit quality concerns during acquired portfolio integration amid inflationary headwinds affecting borrower repayment capacity [S5; S16; S4].

Success hinges on disciplined underwriting standards alongside leveraging cross-selling opportunities across insurance and wealth management segments anchored locally but amplified via new mortgage platforms fueling deposit growth.

Analyst’s Lens: What To Monitor Next for ACNB

Key metrics warranting monitoring include:

- Progress on post-acquisition integration focusing on cost synergy realization timelines including branch consolidations,

- Loan portfolio quality trends assessed through nonperforming loans trajectories particularly within newly acquired portfolios,

- Regulatory developments potentially reshaping capital buffers or liquidity disclosures necessitating adaptive capital strategies,

- Competitive positioning regarding mortgage market share gains attributable to Traditions Mortgage effectiveness relative to regional peers,

- Sustainability of dividend payouts vis-à-vis free cash flow amid macroeconomic uncertainties including interest rate cycles.

Maintaining robust credit risk assessments is critical as geographic reach slightly extends beyond historic core while preserving the community banking ethos established since inception.

Disclaimer: This analysis relies exclusively on publicly available information as of March 15th, 2026 ([F1], SEC filings [S#], news reports [N#]) without forward-looking statements constituting investment advice or forecasts beyond stated company disclosures or verifiable data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments