CoastalSouth Bancshares’ Strategic Loan Growth and Interest Risk Management Drive 2025 Results

CoastalSouth achieved notable net interest income growth in 2025 through targeted loan portfolio expansion coupled with disciplined derivative hedging and robust capital management.

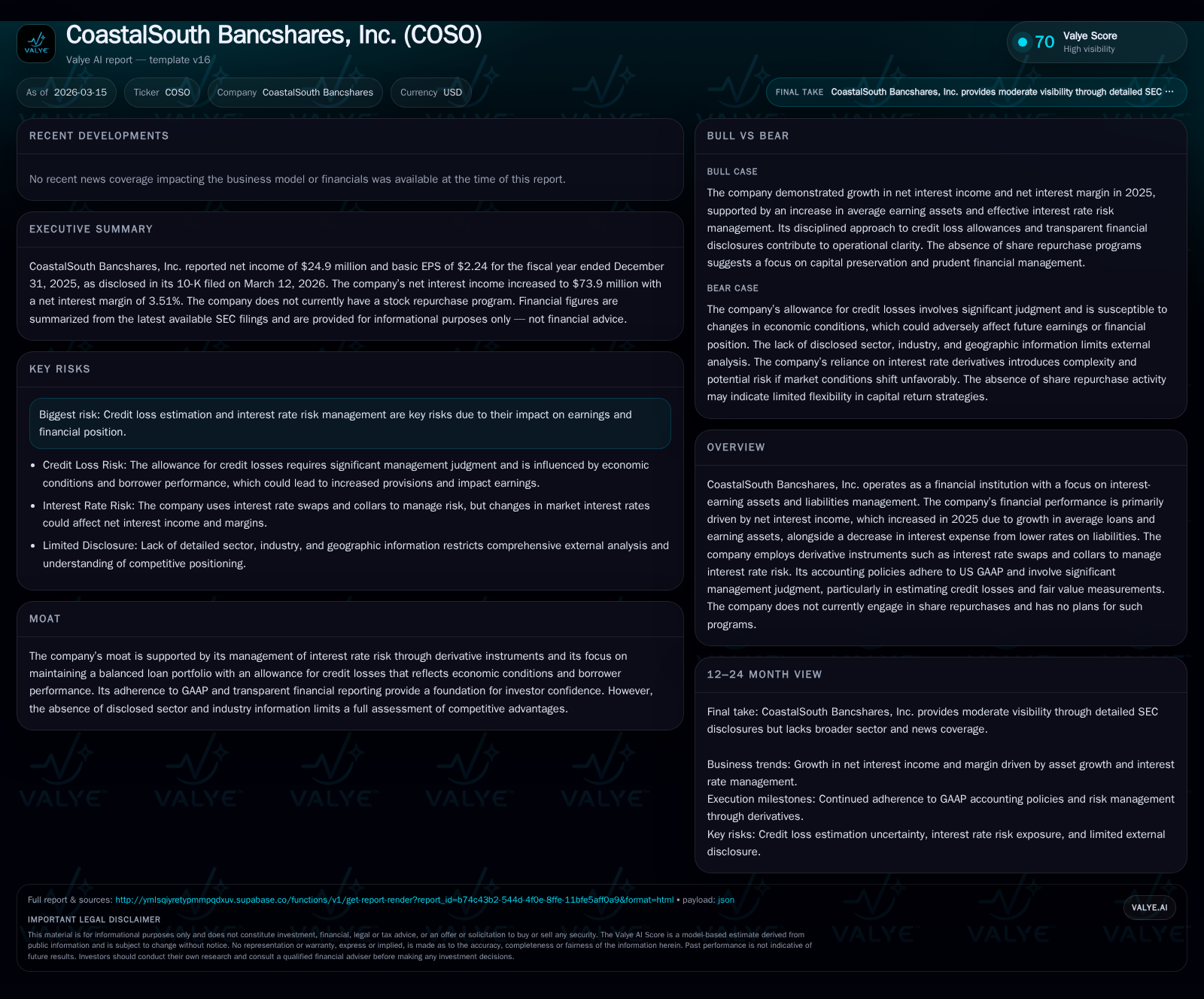

In 2025, CoastalSouth Bancshares, Inc. delivered strong financial results driven by a 12.9% increase in gross loans, supporting enhanced net interest income alongside effective use of interest rate derivatives to manage risk. The company’s loan portfolio growth was primarily fueled by commercial and retail lending segments underpinned by rigorous credit approval standards. CoastalSouth maintained capital adequacy ratios well above regulatory minimums, supported diverse liquidity sources, and sustained dividends without share buybacks. Looking ahead, loan demand remains a key growth lever amid interest rate volatility and evolving credit risks tied to economic conditions.

Surge in Loans Fueling Interest Income Growth in 2025

CoastalSouth Bancshares recorded robust growth in its loan portfolio during fiscal year 2025, with total gross loans rising by $204.8 million or 12.9% to reach approximately $1.79 billion [F1][S7]. This advance was primarily anchored in increased originations within commercial and retail lending sectors, illustrating strong client demand across core markets that CoastalSouth serves. The firm’s gross loans held for investment (LHFI) surged by roughly 14.7% to $1.62 billion as of December 31, 2025, up from about $1.41 billion a year prior [S7]. Meanwhile, loans held for sale (LHFS) slightly declined to $170.9 million from $174 million.

The composition of the loan book remained diversified yet focused within specific sectors: income-producing commercial real estate (CRE) constituted about 23.4% of LHFI ($378 million), senior housing loans accounted for 16% ($260 million), with meaningful exposures also in marine vessels and commercial & industrial (C&I) segments [S19]. The Company maintains systematic credit approval procedures guided by underwriting standards designed to evaluate cash flow sufficiency under stressed interest rate scenarios and enforce covenants to mitigate deteriorations in borrower quality [S10]. Such disciplined lending frameworks underpin the stability of earnings derived from interest income.

Average loans comprised nearly 80% of total earning assets in 2025 versus approximately 77.7% the previous year, highlighting the Company's strategic emphasis on expanding its core interest-earning asset base [S7]. Consequently, net interest income—the key driver of profitability—benefited from this loan growth.

Derivative Instruments and Risk Management Framework

CoastalSouth implements a formal asset-liability management strategy that employs derivative financial instruments like interest rate swaps and collars as primary tools for hedging exposure to interest rate fluctuations [S24]. These derivatives are accounted for under ASC 815 principles regarding hedge accounting, where qualifying hedges protect net interest income against adverse movements in rates over specified horizons.

The governance surrounding these activities is robust: the Credit and Risk Committee of the Board holds primary oversight responsibility for risk management programs, including periodic reviews of hedging strategies and cybersecurity measures linked to operational resilience [S1]. Management also relies on comprehensive modeling—including immediate shock scenarios—to assess the sensitivity of net interest revenue over twelve-month timeframes under various rate environments [S25].

This derivative-driven risk posture supports margin resilience despite uneven repricing speeds between assets (loans) and liabilities (deposits). Fair value measurements of these instruments utilize discounted cash flow approaches incorporating current market yields while adhering strictly to US GAAP valuation frameworks that involve significant managerial judgment particularly when observable market data is limited [S15].

Outlook: Lending Demand Versus Interest Rate Headwinds

Looking forward, CoastalSouth's ability to sustain loan growth rests on continued client demand juxtaposed against potential constraints imposed by the broader interest rate climate . While the strong pipeline evidenced during 2025 bodes well, variable-rate instruments within the portfolio may pressure net interest margins if market rates experience volatility inconsistent with hedging assumptions.

Furthermore, credit loss provisions are sensitive to economic developments influencing borrower creditworthiness—a key point emphasized by management’s dynamic allowance methodology integrating reasonable forecasts alongside qualitative risk factors [S27]. These factors collectively form a balancing act between promoting earnings growth via asset expansion while maintaining risk controls.

Capital Position, Liquidity, and Regulatory Compliance

CoastalSouth exhibits a solid capital foundation evidenced by robust CET1 and Tier 1 risk-based capital ratios respectively at approximately 12.3% as of December 31, 2025—well exceeding regulatory minimums required for classification as "well-capitalized" under Federal banking guidelines [S8][S17]. Correspondingly the leverage ratio stood around 11.18%, reinforcing capital adequacy relative to total assets.

The bank's liquidity management framework leverages various cash flow sources including substantial balances of cash equivalents (interest-bearing deposits), federal funds sold, and pledged investment securities serving as collateral for borrowing facilities [S5][S6]. Access to external funding lines remains ample with undrawn unsecured federal funds lines totaling $69.5 million and FHLBA advances increasing to $30 million outstanding against a borrowing capacity upwards of $176 million at year-end [S4][S6]. No borrowings were outstanding against the Federal Reserve discount window during this period.

Operating lease liabilities are well-managed with right-of-use assets balanced against commitments over multiple years, contributing controlled fixed costs [S20]. Importantly, CoastalSouth adheres consistently to capital conservation buffer requirements which regulate dividend declarations and restrict discretionary payouts without sufficient capital cushions [S8][S16].

Capital Allocation: Dividends without Share Repurchases

While CoastalSouth has instituted a steady dividend policy aligned with maintaining its capital conservation buffer requirements [S16], it notably abstains from share repurchase programs, explicitly stating no plans or programs exist as of latest reports [S1]. This approach aligns with prudent capital stewardship typically advisable within mid-sized banking institutions facing regulatory scrutiny.

By retaining earnings rather than distributing via buybacks, CoastalSouth preserves flexibility for reinvestment into organic growth initiatives or bolstering reserves against unforeseen downturns—an increasingly relevant posture amid uncertain macroeconomic conditions.

Credit Quality Focus Amid Economic Uncertainties

The allowance for credit losses expanded by approximately $1.6 million or nearly 9.5%, reaching $18.7 million at year-end reflecting portfolio growth along with heightened provisioning activity which totaled about $3.2 million in fiscal 2025 versus just $553 thousand prior year [S10][S27].

Credit loss estimation employs sophisticated modeling incorporating loss rate methods combined with qualitative overlays addressing industry concentrations (notably commercial real estate segments like senior housing), geographic exposure, underwriting standards evolution, collateral valuations, and emerging borrower trends [S27]. Stress testing debt service ability under higher rate environments further underscores conservative assumptions embedded within lender assessments [S10].

While no material litigation or adverse regulatory issues emerged during the period [S14], management acknowledges inherent uncertainties tied to credit risk forecasting requiring ongoing review and adjustment.

Monitoring Key Milestones: What Investors Should Watch

Absent explicit guidance from management on future financial targets or milestones beyond routine disclosures [N*], observers should prioritize monitoring several critical facets:

- Sustainability of double-digit loan growth amid competitive pressures and shifting borrower demand dynamics.

- Effectiveness of derivative hedging strategies evaluated through sensitivity analyses reported periodically.

- Trends in allowance for credit losses reflecting any signs of increasing delinquencies or concentration risk emergence.

- Movement in capital ratios vis-à-vis evolving regulatory standards potentially impacting dividend capacity.

- Liquidity status benchmarks including access utilization rates on borrowing facilities alongside deposit inflows/outflows.

- Market environment shifts influencing cost of funds which could exert margin compression outside modeled scenarios.

Such metrics provide insight into CoastalSouth’s operational discipline balancing growth ambitions against financial resilience imperatives.

Historical Financial Performance Summary (FY2024-2025)

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Data sourced from company filings reflecting audited figures as of December 31 each year [F1][S7].

This analysis synthesizes publicly available data without endorsing investment decisions or providing explicit forecasts beyond documented disclosures. Readers should consider broader market conditions alongside institutional developments when forming perspectives on CoastalSouth Bancshares’ ongoing trajectory.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments