Ames National Corp’s Iowa-Centric Banking Model Faces Growth and Credit Risk Challenges

Ames National Corp leverages regional expertise but must manage credit and economic risks impacting its loan portfolio and capital returns.

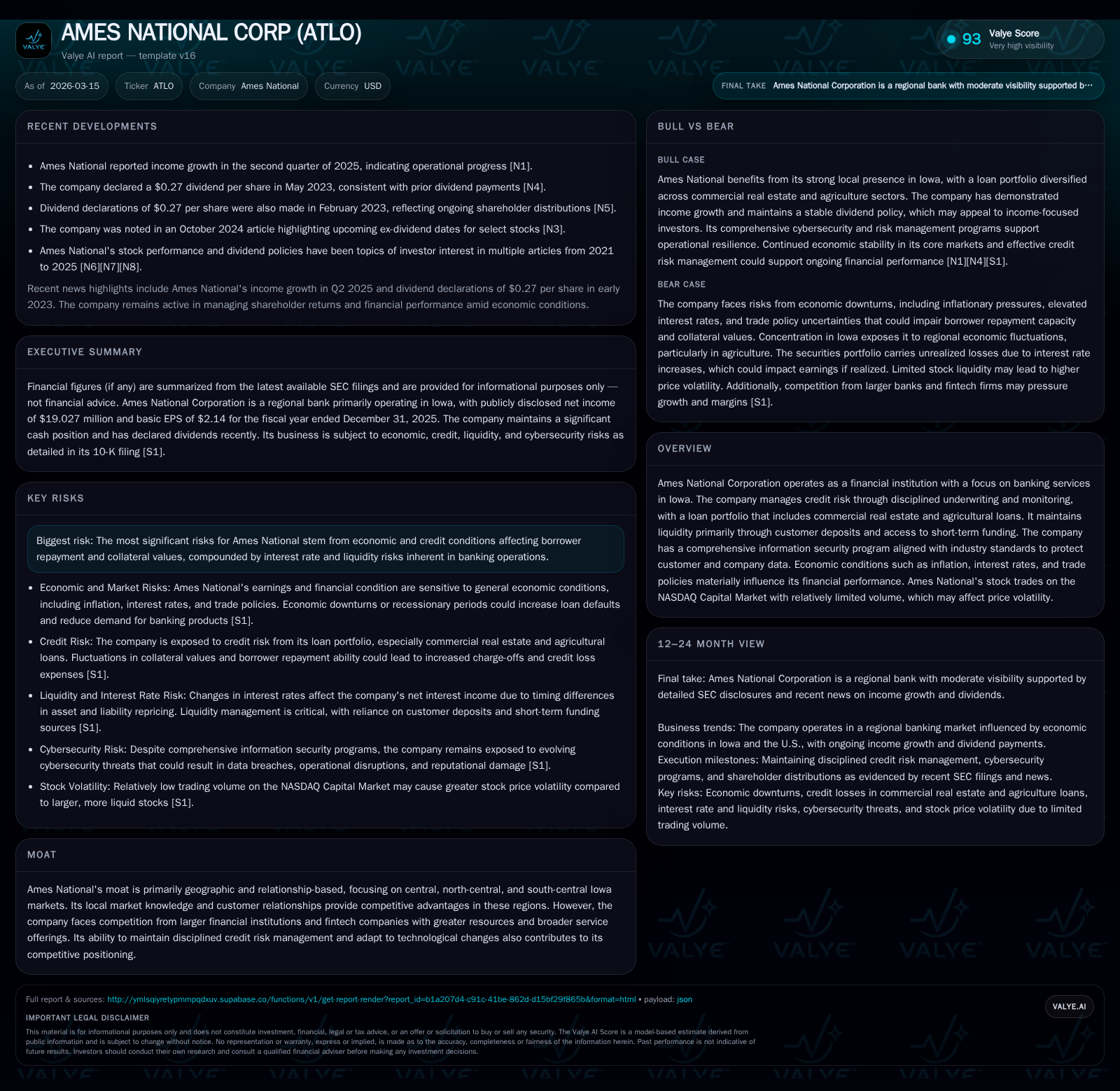

Ames National Corporation operates primarily within Iowa, focusing on relationship-driven banking with significant exposure to commercial real estate and agriculture loans. While the company's disciplined credit risk management and local market knowledge underpin its moat, growth prospects are constrained by geographic concentration, economic volatility, and evolving competition. Recent financials show a strong rebound in net income supported by operational cash flow growth and modest capital expenditures. However, credit risk from fluctuating collateral values, interest rate pressures, and regulatory constraints may limit future expansion. The company has maintained steady dividends and initiated small share buybacks, reflecting a cautious capital allocation approach amid ongoing tightening in monetary policy.

Company Overview

Ames National Corporation operates as a financial institution serving local communities throughout central, north-central, and south-central Iowa. Its banking model centers on cultivating enduring customer relationships within these geographically focused markets, establishing a moat based on local knowledge and personalized service. The company's loan portfolio is weighted notably toward commercial real estate and agriculture-related borrowers, sectors inherently sensitive to regional economic conditions.

Historical Financial Performance

Financial results for fiscal years 2022 through 2025 reveal variability influenced by macroeconomic factors but culminating in a strong performance rebound in 2025:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 19 | 21 | 1 | +86.2% |

| 2024 | 10 | 14 | 0 | -5.5% |

| 2023 | 11 | 19 | 5 | -43.9% |

| 2022 | 19 | 21 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 7 | 2 | 21 |

| 2024 | 9 | 1 | 14 |

| 2023 | 10 | 0 | 14 |

| 2022 | 10 | 2 | 18 |

Source: SEC companyfacts cache [F1].

The sharp increase in net income in FY2025 was supported by strong cash flow generation and contained capital expenditures which doubled from the prior year but remained modest overall. Dividends were reduced relative to prior years suggestive of a cautious stance on shareholder returns amid uncertain conditions; small-scale share repurchases resumed after hiatus in prior year.

Business Drivers & Risk Factors

Loan Portfolio Concentration & Credit Risk

Commercial real estate accounts for a significant proportion of the loan portfolio; this sector's vulnerability to swift collateral value swings due to localized market conditions impacts risk profile materially [S19]. Agriculture loans also form a major pillar with distinct cyclical exposure to commodity price fluctuations (e.g., corn and soybeans), input cost inflation driven by energy prices or fertilizers, government policy shifts especially trade tariffs affecting export demand [S22,S23].

Loan underwriting emphasizes disciplined standards; however adverse weather events or prolonged downturns may impair borrower repayment ability leading to higher credit loss provisions [S6,S22]. Management actively monitors allowances for credit losses but acknowledges potential material upward revisions if conditions deteriorate.

Macroeconomic & Interest Rate Environment

Persistent inflation through late-2025 elevated operating costs particularly wage pressures amid competition for skilled personnel [S1]. The Federal Reserve's pause in rate cuts after aggressive hikes leaves short-term borrowing expensive while competitive forces drive deposit cost increases compressing net interest margins [S9,S28]. Elevated rates risk dampening loan growth demand as well as increasing default likelihood among leveraged borrowers.

Trade policy uncertainty stemming from tariff dynamics between U.S. and major trading partners adds another layer of unpredictability affecting corporate client confidence and investment decisions within Iowa’s export-dependent industries [S13].

Regulatory & Operational Constraints

As a bank holding company dependent on dividends from its subsidiaries for operating cash flows and capital return ability to shareholders is limited by federal restrictions on bank dividend payments that safeguard regulatory capital buffers [S8,S20,S27]. This framework tempers flexibility in dividend hikes or share repurchases.

Further operational risks include the threat of cybersecurity breaches despite comprehensive safeguards employing industry-aligned security frameworks such as those recommended by FFIEC and NIST [S29]. Third-party vendor oversight remains critical given outsourcing dependencies.

Competitive Landscape & Technology Adaptation

The regional focus restricts scalability but enables intimate customer relationships serving as differentiation against national players with broader product sets [N/A – analysis]. Competitive pressure intensifies from fintech entrants innovating in payments or lending platforms pushing Ames National toward measured investments in digital channels while maintaining cost discipline.

Strategic Growth Prospects

Growth hinges on leveraging local market expertise combined with moderate loan portfolio expansion balanced against maintaining credit quality under evolving economic regimes. Opportunities exist where regional agricultural recovery or commercial real estate demand rebounds.

However geographic concentration limits diversification benefits which could cap long-term growth potential absent expansion into adjacent markets or segments.

Investment in technology infrastructure aimed at improving customer convenience (e.g., mobile banking enhancements) represents a strategic priority to counterbalance nascent fintech competition.

Capital Allocation

Return on equity approximated at around 9.2% for FY2025 indicates reasonable profitability though not indicative of outsized returns typical in more diversified banks [F1]. Free cash flow generation remains robust supporting ongoing dividends albeit at subdued levels compared to earlier periods. Resumption of modest share repurchases signals measured confidence but prudence given market uncertainties.

Capital levels remain adequate with regulatory compliance paramount given supervisory scrutiny over banking institutions' resilience post-pandemic.

What To Watch

- Trends in commercial real estate valuations within Iowa’s key counties affecting loan loss provisioning.

- Developments related to agricultural market prices and tariff-related impacts influencing borrower health.

- Changes in Federal Reserve policies around interest rates impacting net interest margins.

- Regulatory announcements regarding bank dividend limitations or capital requirements.

- Investments or partnerships enhancing digital banking capabilities versus fintech competitors.

- Potential mergers or acquisitions that could diversify geographic footprint or product offerings (no recent activity reported).

Conclusion

Ames National Corporation presents a focused community bank model deeply embedded in Iowa’s economic fabric with strengths rooted in relationship banking and local underwriting discipline mitigating some risks associated with concentrated sectors like agriculture and commercial real estate. While recent financials demonstrate a clear rebound backed by solid cash flows and controlled costs,[F1] persistent geopolitical tensions around trade policies coupled with domestic high inflation/interest rate environment create ongoing headwinds.

The company's cautious capital allocation strategy underscores an awareness of economic uncertainties; careful monitoring of evolving credit conditions alongside proactive technology adoption will be essential for sustaining competitiveness going forward.

This analysis synthesizes publicly available data up through early 2026 filings without offering investment recommendations or forecasts beyond reported facts and company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments