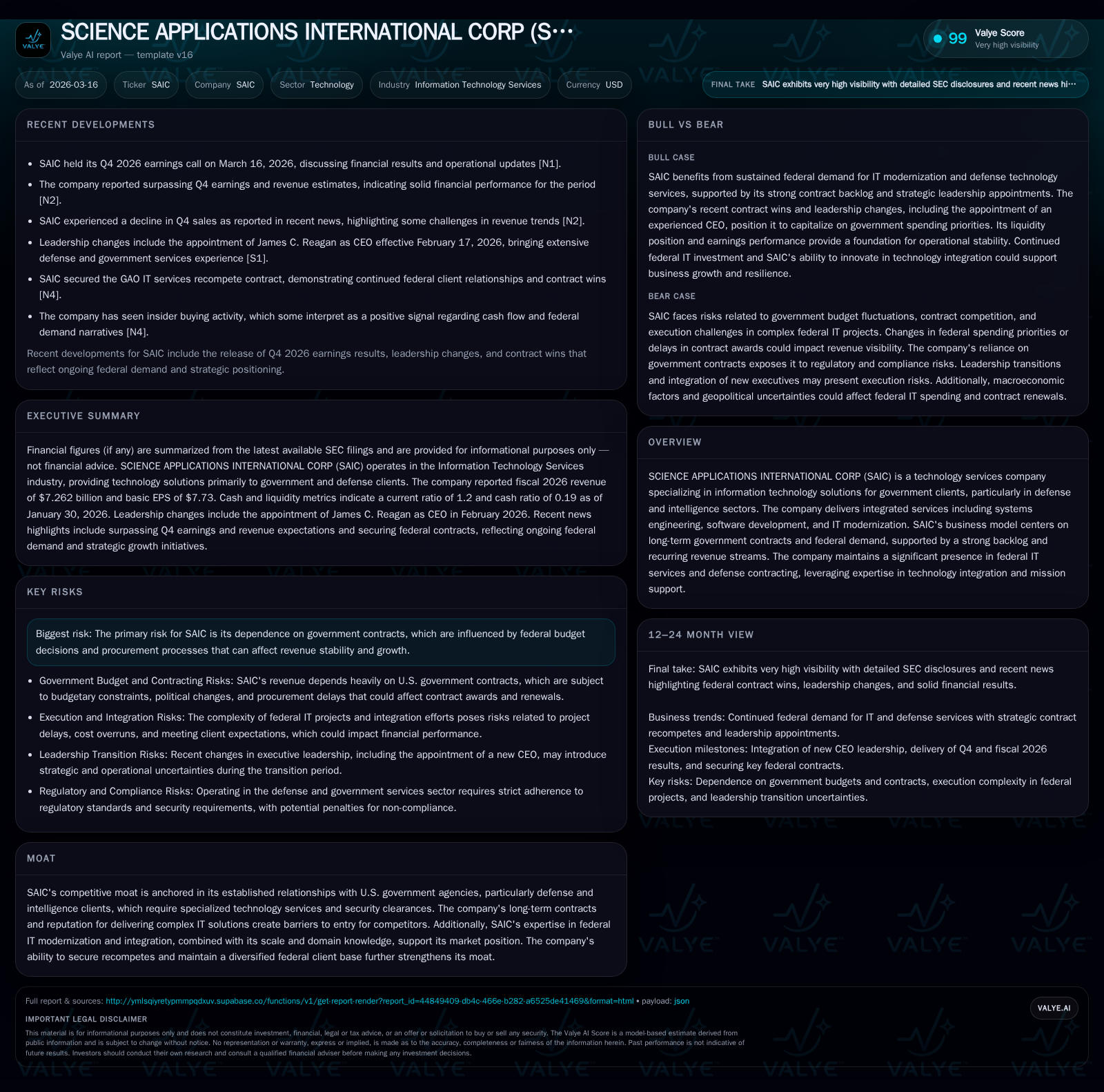

Science Applications International’s Earnings Pressure and Capital Deployment in Spotlight

SAIC faces revenue and net income declines offset by cash flow growth and deliberate capital return strategies amid government contracting headwinds.

Science Applications International Corporation (SAIC) reported a 2.9% revenue decline in fiscal 2026 alongside a sharper 24.1% drop in net income compared to the prior year, reflecting contract repricing and federal spending uncertainties. Despite pressures on the top and bottom lines, operating cash flow rose 23.3%, driven by working capital management and disciplined capex reductions. SAIC continues to sustain shareholder returns through significant share buybacks and dividends, bolstered by a strong return on equity of approximately 24.1%. Future growth hinges on federal budget dynamics and success in contract recompetes, with near-term guidance remained cautious.

Evolution of SAIC’s Growth: Tracking Fiscal Year Trends

SAIC's fiscal year 2026 results illustrate a mild contraction in revenue alongside compressions across operating income and net income margins, set against stronger operational cash flows [F1]. Revenue declined by 2.9% from $7.48 billion in FY2025 to $7.26 billion in FY2026, reflecting the challenges inherent in government IT services contracting cycles where IDIQ (indefinite delivery/indefinite quantity) contracts dominate [F1]. Operating income dropped 7.5% year-over-year to $521 million, with net income down sharply by 24.1% from $477 million to $362 million [F1]. This suggests rising cost pressure or mix shifts adversely impacting profitability beyond top-line softness.

Despite this profit squeeze, operating cash flow achieved notable growth of +23.3% to $609 million driven by efficient working capital management and a modest decrease in capital expenditures (down 11.1% YoY to $32 million) [F1]. Share repurchases increased compared to earlier years ($445 million vs $382 million in FY2024), exemplifying continued disciplined capital returns [F1]. The table below summarizes key annual performance metrics.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2026 | 7.3 | 609 | 521 | -2.9% | ||

| 2025 | 7.5 | 362 | 494 | 563 | -24.1% | |

| 2024 | 477 | 396 | 741 | +59.0% | ||

| 2023 | 300 | 532 | 501 | +8.3% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 445 | 577 | |

| 2025 | 558 | 458 | 23.0 |

| 2024 | 382 | 369 | 26.7 |

| 2023 | 267 | 507 | 17.7 |

Source: SEC companyfacts cache [F1].

Understanding Drivers Behind Declining Revenue and Profitability

SAIC’s decline in sales relates closely to external factors typical for government contractors: contract repricing pressure stemming from macroeconomic inflation impacts on labor costs; ebbing demand due to federal budget realignments; and stiffening competition for recompetes highlighted during the latest earnings call [N1][N7][S1][S4]. The company operates largely under IDIQ contracts requiring qualified security clearances—a complex barrier that nonetheless limits market entrants but also lengthens recompete cycles potentially reducing near-term revenue replenishment.

Additionally, shifts towards newer IT modernization solutions have introduced pricing pressure as federal customers increasingly seek cost optimization amid tighter appropriations [N7][S4]. Profitability suffered more pronounced contraction than revenue due to these mix effects alongside increased overhead investment supporting compliance with stringent customer requirements [S4].

Government Contract Dynamics Reshaping Future Growth Potential

The company’s growth outlook is tightly intertwined with federal budget cycles influencing contract pipelines [N9][S6][S1]. As discussed during recent analyst upgrades [N9], SAIC expects modest recovery beginning FY2027 contingent on securing recompetes within its existing defense-intelligence client base.

Procurement uncertainty remains elevated given multi-year funding delays common in defense appropriations processes and the absence of disclosed material backlog expansion or significant new contract awards emerged from filings or public statements [S1][N9]. Thus, the company’s durable but cyclical government revenue model drives a cautiously optimistic stance pending clearer visibility into award timing.

Operational Cash Flow Expansion Amid Revenue Pressure

A key positive highlight is the robust expansion (+23.3%) in operating cash flow despite revenue softness [F1][S8]. This suggests effective working capital management including collections acceleration and inventory control commonly critical for defense contractors juggling complex billing schedules tied to milestone achievements.

Capex discipline complements this dynamic: FY2026 spending retrenched slightly (-11%) reducing cash outflow burden while maintaining essential technology investments aligned with modernization priorities [F1][S8]. Free cash flow generation remains strong at an estimated $577 million (operating cash flow less capex), sustaining flexibility for capital returns or strategic initiatives [F1].

Capital Allocation Strategy: Balancing Dividends and Buybacks

SAIC’s board has demonstrated consistent shareholder return commitment via ongoing dividend payments ($0.37 per share declared payable April 2026) alongside sizable stock repurchases totaling $445 million for FY2026 – though below the previous year's elevated figure [F1][S7][S9]. This balanced approach reflects recognition of current earnings pressures while preserving capital discipline vital for navigating fluctuating government contract environments.

An approximate return on equity near 24.1% underscores attractive efficiency levels underlying this distribution strategy despite net income decline [F1]. Buybacks also serve as signal mitigating dilution risks linked to employee compensation plans prevalent in cybersecurity-intensive defense IT sectors where talent retention is paramount [S7][S9].

Financial Health Snapshot: Liquidity, Leverage, and ROE Analysis

Liquidity positions remain sound; SAIC reported current assets at approximately $1.18 billion against current liabilities near $982 million yielding a comfortable current ratio around 1.2 as of fiscal year end January 30, 2026 [F1][S18]. This adequacy supports near-term obligations including contract performance-related expenditures.

Equity totaled about $1.5 billion reflecting moderate declines from prior years yet supporting reported ROE metrics via efficient asset utilization despite profitability headwinds [F1]. Debt levels disclosed remain manageable within sector norms thus preserving credit rating stability crucial for working capital financing tailored around multi-phase federal contracts requiring nuanced cash flow forecasting [S18].

Risks Rooted in Federal Procurement and Budget Volatility

Principal risks center on governmental budget fluctuations that may induce abrupt procurement slowdowns or contract scope adjustments—referred colloquially as “procurement cliffs” within defense circles—and impact revenue visibility fundamentally [S4][S5][S10]. Regulatory compliance demands elevate operational complexity especially when dealing with classified projects necessitating recurring security clearances which increase personnel turnover costs.

Legal proceedings noted represent potential contingent liabilities possibly affecting future results though specific case outcomes remain uncertain per SEC risk disclosures [S4][S5][S10]. Additionally, federal shutdown scenarios could disrupt contracting timelines creating quarterly financial variability inherent to the sector’s cyclicality.

What to Watch Next: Indicators for Earnings Rebound or Continued Lag

Upcoming milestones include SAIC’s FY2027 first quarter guidance release anticipated during next earnings cycle—market focus will lie heavily on announced contract wins/recompetes indicating backlog trajectory shifts as well as operating margin inflections validating cost control effectiveness amidst competitive pressures [N1][N9].

Further indicators involve monitoring evolving federal IT modernization spending that could accelerate demand for integrated solutions aligned with SAIC’s core competencies in systems engineering and mission support domains typically leveraged post-contract award stages within the industry context.

Disclaimer: This analysis relies strictly on information available from cited regulatory filings, official news transcripts, and documented data points without offering investment recommendations or speculative forecasts beyond clearly labeled forward-looking discussion based on disclosed guidance or observable trends.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments