Better Home & Finance's Growth Spurs Revenue Gains Despite Persistent Losses and Liquidity Challenges

BETR leverages its AI-driven Tinman platform to expand mortgage originations, while navigating financial losses and capital constraints.

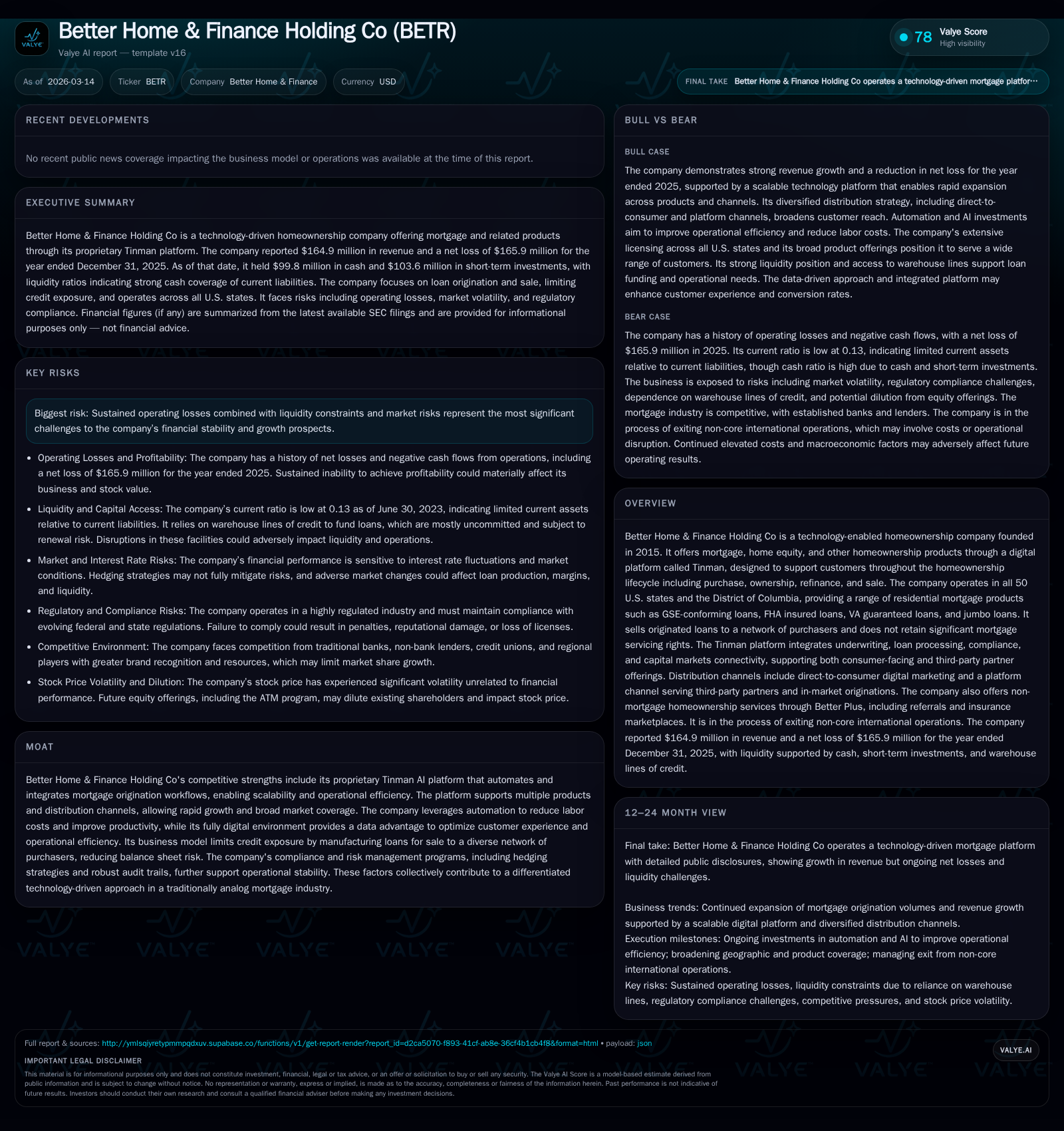

Better Home & Finance Holding Co (BETR) has achieved robust revenue growth driven by increased funded loan volume and a scalable digital platform, Tinman. However, the company continues to face significant net losses and negative operating cash flows, straining liquidity and raising concerns about its financial stability. BETR’s business model mitigates credit risk via rapid loan sales but is vulnerable to interest rate volatility and regulatory complexities. Future growth depends on broadening geographic coverage, enhancing technology automation, and expanding partner channels.

Company Overview

Better Home & Finance Holding Co (BETR), founded in 2015, operates as a technology-enabled homeownership company with a mission to transform the traditionally analog mortgage sector into a streamlined digital experience. Central to this effort is its proprietary AI-driven Tinman platform that automates underwriting, loan processing, compliance, capital markets connectivity, and overall workflow orchestration supporting mortgage origination across various product categories. BETR offers residential first-lien mortgage loans—spanning government-sponsored entity (GSE) conforming loans, FHA insured loans, VA guaranteed loans—and jumbo loans nationwide across all U.S. states plus DC [S1][S10][S18].

Historical Performance

BETR has demonstrated accelerating top-line growth over recent years amid volatile industry conditions characterized by elevated interest rates. Annual revenue expanded from $76.8 million in FY2023 to $108.5 million in FY2024 (+41%) reaching $164.9 million in FY2025 (+52%) [F1]. This progression was supported by funded loan volume growth of approximately 32% in 2025 relative to the prior year [S1]. Despite scaling revenue, BETR continues to post substantial net losses attributable largely to elevated operating expenses associated with continued investment into its platform development, marketing spend for customer acquisition, and workforce restructuring [F1][S1]. Net loss narrowed from $206.3 million in FY2024 to $165.9 million in FY2025 (-20%) though remains pronounced [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 165 | -166 | -167 | +52.0% | +19.6% | |

| 2024 | 108 | -206 | -380 | +41.2% | +61.5% | |

| 2023 | 77 | -536 | -160 | -291 | -6240.7% | |

| 2022 | 9 | -1 | -9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -168 | -446.1 |

| 2024 | -383 | 354.6 |

| 2023 | -160 | -437.5 |

| 2022 | 42.5 |

Source: SEC companyfacts cache [F1].

Note: Operating Cash Flow = CFO; Capex = Capital Expenditures; Equity = Total Stockholders' Equity [F1]

Operating cash flow remains deeply negative ($-166.6 million in FY2025), reflecting ongoing investments coupled with working capital requirements typical of mortgage originators reliant on short-term warehouse financing [F1][S12]. Capital expenditures have normalized (~$1 million), indicating modest investment relative to operational scale.

Business Model and Competitive Strengths

BETR operates primarily as a loan manufacturer selling nearly all originated loans into a diverse secondary market rather than retaining servicing rights [S10][S16]. This approach controls credit risk exposure but amplifies sensitivity to interest rate volatility affecting gain-on-sale margins and loan demand cycles [S1]. The Tinman platform drives scalability by integrating underwriting automation with compliance checks tailored for multi-jurisdictional licenses [S10][S16]. By supporting both direct-to-consumer engagement through performance marketing and a platform channel that partners with third parties who integrate Tinman technology or source loans via BETR’s Home Finance products, the company diversifies customer access points [S13].

Tinman’s AI-driven engine collects extensive data points across each loan file ensuring robust audit trails vital for regulatory compliance which complements their internal compliance team's monitoring efforts [S11][S16]. The company also offers "Better Plus," ancillary homeownership services like referrals for real estate agents and insurance policies via partnerships acting as an agent or referral source generating fee income [S4].

Market Position & Geographic Exposure

As of early 2026, BETR is licensed across all U.S states plus DC with some geographic concentration: approximately one-third of funded loans came from California (17%), Texas (9%), and Florida (7%) during FY2025 [S14][S21]. This geography concentration exposes BETR to regional economic shifts and housing market dynamics which could disproportionately affect origination volumes if adverse.

Competition spans traditional banks, non-bank lenders, credit unions and emerging fintech platforms leveraging similar or adjacent digital origination workflows [S16]. BETR differentiates through continuous investment in end-to-end process automation aiming to lower manufacturing costs below legacy lenders.

Risks & Challenges

BETR’s business is highly sensitive to interest rates—elevated or volatile rates suppress purchase/refinance volumes directly compressing revenue streams given the model’s reliance on gain-on-sale margins rather than MSRs retention [S1][S16]. Though hedging strategies mitigate some exposure between rate lock commitments and investor deliveries, rapid interest rate swings can materially disrupt profitability.

Employee attrition especially among senior management has depleted institutional knowledge impacting key functions such as legal/compliance/accounting/IT [S1]. Recruiting qualified personnel remains challenging amid competitive labor markets for AI-engineers and mortgage underwriters compounded by negative media attention related to workforce reductions since late 2021.

Legal risks include ongoing labor dispute lawsuits claiming unpaid overtime under Fair Labor Standards Act impacting potential liability up to several million dollars plus related litigation involving the CEO posing reputational hazards [S7][S19][S29]. Regulatory burdens are broad encompassing federal/state consumer finance laws alongside emerging AI/data privacy rules adding complexity and cost pressures [S7][S8][S15].

Warehouse funding dependency represents a critical liquidity risk—BETR utilizes three primary warehouse lines totaling $575 million available credit but mostly uncommitted subject to termination or margin calls based on collateral values potentially triggering sudden funding squeezes impeding loan production liquidity if not renewed or replaced on favorable terms [S9][S12][S17].

Future Growth Prospects & Initiatives

BETR foresees growing addressable market share through enhanced customer experiences enabled by further automating manual processes across origination workflows reducing cycle times while lifting conversion rates from application through closing stages leveraging AI advancements within Tinman [S10][S16].

Expanding products into underserved states/product types including government-insured segments remains a focus coupled with broadening geographic coverage as licensing/enforcement capacities scale [S11][S13][S21]. The company plans amplified digital marketing efforts driving organic traffic complemented by deeper penetration via strategic partners integrating Tinman capabilities presenting embedded origination pipelines feeding BETR’s home finance products [S16][S10].

Investment continues toward embedding voice-based AI assistant "Betsy" fostering streamlined data collection during applications enhancing user interaction efficiency without relinquishing necessary human oversight where warranted [S18].

However, no explicit public guidance or specific milestones were disclosed beyond these strategic directional comments as of the filing date; consequently monitoring key metrics like funded loan volume trajectory, gain-on-sale margins amidst macroeconomic shifts; warehouse line renewals; employee retention rates; compliance outcomes; legal-litigation resolutions; alongside execution progress on tech enhancements will be pivotal for assessing forward momentum.

Returns & Capital Allocation

BETR has not generated positive returns historically; approximate return on equity stood at an estimated -446% based on FY2025 net loss against year-end equity of $37 million reflecting deep negative profitability pressures sustained over multiple years since inception as it invests heavily in growth initiatives [F1].

Operating free cash flow after subtracting capex remained negative approximately $-167 million highlighting continuing cash burn patterns contributed by working capital needs aligned with the company's model of short-term financing of loans before sale proceeds repay borrowings [F1]. The firm does not currently pay dividends or conduct share buybacks emphasizing prioritization of reinvestment into platform enhancements and debt servicing amid constrained liquidity [F1].

Summary Analysis

Better Home & Finance occupies an intriguing niche combining sophisticated AI-driven automation within an entrenched yet inefficient U.S housing finance ecosystem dominated by legacy players slow to digitize fully. Its rapidly growing funded loan volumes underpin impressive top-line expansion evidencing demand traction for digitally native lender models that provide enhanced customer experiences.

Nonetheless recurrent operating losses coupled with weak operating cash flow strained liquidity pose significant hurdles needing resolution through sustained margin improvement leveraging scale effects from automation gains alongside control of operating expenses particularly marketing spend and wage costs amid recruitment challenges.

Market risks anchored chiefly around interest rate fluctuations continue imposing volatility on origination activity while dependence on uncommitted warehouse lines adds financial fragility requiring proactive capital management strategies including potential raising of committed facilities or equity capital should conditions deteriorate further.

Regulatory complexity magnifies operational burdens particularly as privacy/data laws evolve alongside scrutiny linked to labor disputes and CEO litigation influence public perception impacting partner relationships potentially threatening distribution channels critical for growth.

Longer-term value accrual likely hinges on successful scaling product reach geographically across U.S., deepening strategic partnerships integrated onto Tinman platform enabling more efficient origination cost structures combined with systematic risk management adapting dynamically to macroeconomic oscillations prevalent in residential mortgage markets.

This analysis is based solely on publicly available information from filings as of March 14, 2026 ([F1],[S#]) without solicitation or recommendation regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments