A.K.A. Brands Faces Profitability Headwinds Despite Revenue Growth and Operational Expansion

Q1 2026 results reveal rising revenue but sustained net losses amid increased cybersecurity investments and debt refinancing.

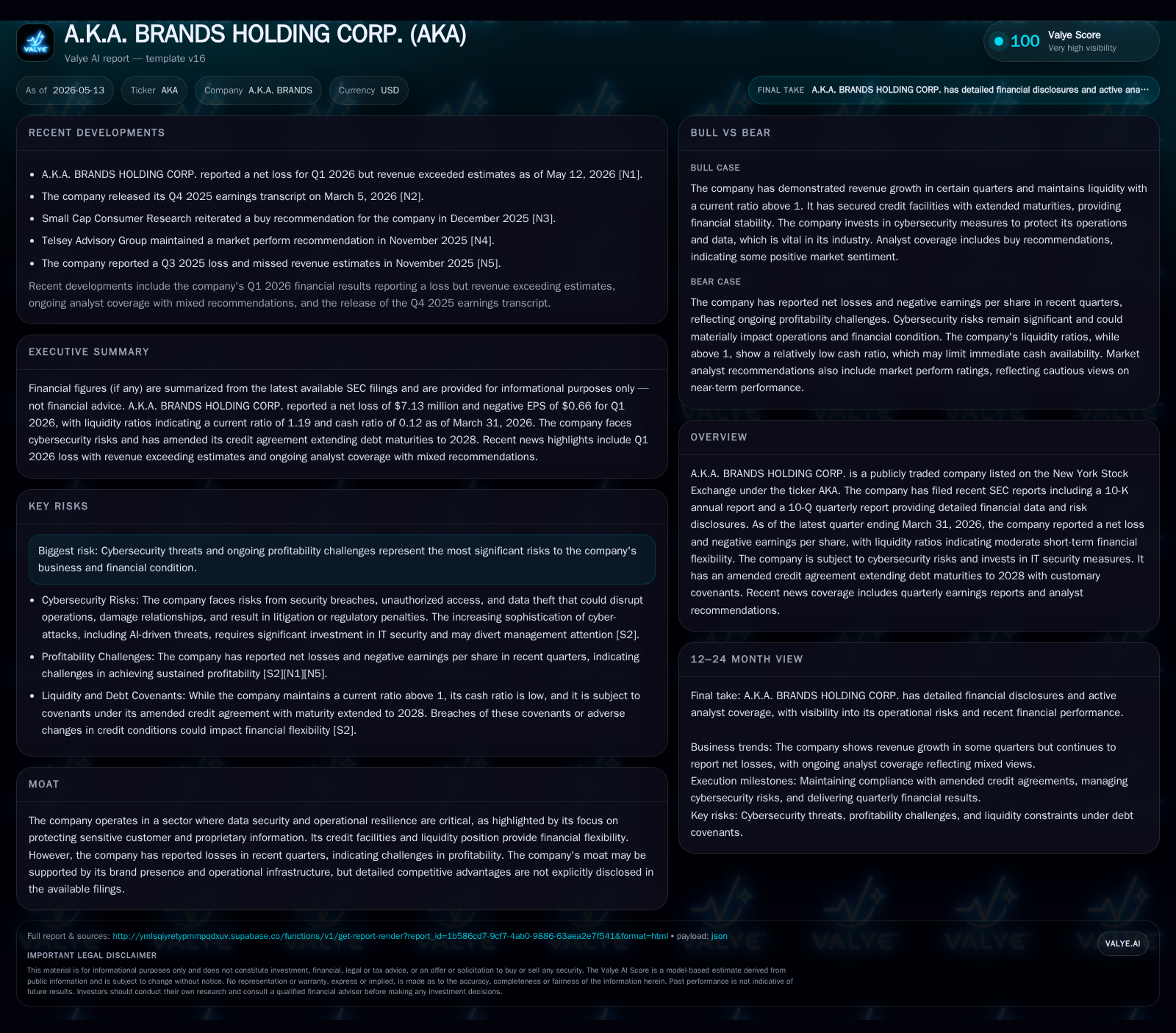

A.K.A. Brands Holding Corp., a portfolio operator of global fashion brands targeting next-gen consumers, reported a first quarter 2026 revenue beat with continued top-line growth driven by strong U.S. sales and active customer base expansion. However, the company remains unprofitable, recording ongoing net losses as it invests heavily in cybersecurity to offset escalating AI-driven threats. The recent refinancing extends credit facilities to 2028, providing financial flexibility to support store openings and wholesale expansion of trend-focused labels such as Princess Polly and Culture Kings. While its data-driven merchandising model fuels frequent product refreshes, risks persist from competitive pressures, consumer preference shifts, and operating cost volatility.

Recent Operating Update: Q1 2026 Performance

A.K.A. Brands Holding Corp.'s latest quarterly filing dated May 12, 2026 [S2] reveals that while the company delivered revenues surpassing analyst expectations for the first quarter ending March 31, 2026, net income remained negative continuing a multi-quarter pattern of losses [N1]. This topline strength was largely driven by growth in U.S. sales and an expanding active customer base across its portfolio.

However, profitability pressure persists due to elevated costs including significant investments in cybersecurity defenses, prompted by an industry-wide escalation in sophisticated data security threats leveraging artificial intelligence methods [S2][S20][S21]. The company emphasized that protecting personal and proprietary information remains critical due to potential reputational damage or regulatory risks from breaches.

Financial flexibility is bolstered by the October 2025 amendment and restatement of its syndicated credit facility extending revolving credit and term loans through October 14, 2028 [S14][S15]. Mandatory amortization payments commence December 31, 2025 but allow capital deployment for growth initiatives such as retail expansion.

Business Model

Operating a portfolio of four lifestyle and streetwear-focused fashion brands — Princess Polly, Petal & Pup, Culture Kings and mnml — A.K.A. Brands targets young consumers (primarily females between ages 15-30) across the United States and Australia [S1]. Revenue derives predominantly from direct-to-consumer e-commerce sales supplemented by brick-and-mortar stores opened strategically since late 2023 and wholesale channel partnerships with major retailers (e.g., Nordstrom, Amazon).

The company employs a distinctive 'test, repeat & clear' merchandising framework leveraging agile data analytics to rapidly introduce new exclusive collections on a weekly cadence. This approach aims to maintain trend relevance and drive frequent consumer repurchases while managing inventory through data-driven clearance strategies.

Crucially, the business model integrates omnichannel retailing combining online experiences with physical stores to build brand engagement — notably Princess Polly's carefully paced store rollout expanding from Los Angeles to multiple U.S. locations since September 2023 [S1].

Margins reflect mix dynamics influenced by sales channels and product assortments, with gross margin improvement modest but positive over recent years based on annual filings [S1]. Nonetheless, operating income remains negative due partly to elevated marketing spend focused on social media influencer collaborations and brand awareness campaigns targeting digitally native customers.

Industry Structure and Competitive Position

A.K.A. operates within the highly fragmented global apparel market valued at approximately $1.84 trillion in 2025 with expected growth driven by e-commerce penetration among millennials and Generation Z shoppers [S1]. The company competes against both legacy fashion conglomerates adapting to digital trends and nimble direct-to-consumer startups.

Its competitive moats include agile brand management expertise enabling rapid response to fast-changing consumer preferences and social media-driven demand volatility. Reliance on China-based suppliers exposes some geopolitical risks but also cost advantages amidst globally complex supply chains.

Cybersecurity emerges as a critical operational pillar differentiating companies able to safeguard customer trust amidst escalating cyber-risk environments characterized by AI-powered hacking attempts [S20][S21]. A.K.A.'s substantial IT security investments underscore this vulnerability.

Growth Drivers

Key growth drivers pivot on multiple axes:

- Geographic Expansion: Aggressive U.S. store openings complement existing Australian presence combined with wholesale distribution scaling broaden market reach.

- Brand Acquisitions: Integration of high-growth labels like Petal & Pup (acquired in 2019) expands market share among young female consumers.

- Digital Engagement: Leveraging platforms like TikTok and Instagram enhances brand relevance among target demographics driving online sales spikes.

- Merchandising Agility: Weekly refreshes enable rapid capitalization on viral trends minimizing markdown risk.

- Omnichannel Synergies: Combining online convenience with experiential retail drives deeper customer engagement boosting lifetime value.

Growth metrics cited include a year-over-year increase in orders (6%) and active customers (3%) through fiscal year-end December 2025 supporting volume expansion [S1].

Risks and Watchpoints

The company acknowledges several material risk factors:

- Profitability Challenges: Despite revenue growth, recurring net losses necessitate focus on operating leverage improvement.

- Cybersecurity Threats: Increasingly sophisticated AI-enabled cyber-attacks require sustained IT investment; failure poses reputational/legal consequences [S20][S21].

- Supply Chain Dependencies: Heavy reliance on Chinese manufacturing subjects operations to geopolitical uncertainties or trade disruptions.

- Consumer Discretionary Spending Volatility: Macroeconomic headwinds like inflation or employment shifts can curtail apparel purchases affecting revenue stability.

- Legal Exposure: Past settlements (e.g., $16.5 million copyright matter) highlight potential contingent liabilities impacting financial health [S1].

- Debt Service Requirements: Amended credit agreement mandates amortizations beginning late 2025; liquidity management will be critical given net debt near $91.7 million per year-end [F1].

What to Watch Next

Upcoming indicators critical to monitoring A.K.A.’s trajectory include:

- Quarterly updates on profitability trends particularly improvements in operating income amid controlled expenses.

- Reports detailing cybersecurity incident occurrence or mitigation success influencing risk profile.

- Customer retention rates and average order values signaling brand loyalty strength in volatile fashion markets.

- Inventory turnover ratios indicating effectiveness of 'test & clear' approach amid rapidly changing fashion cycles.

- Progress against store opening targets validating omnichannel strategy execution.

- Any adjustments or waivers related to debt covenants under amended credit facility impacting financial flexibility.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $20mm | |

| 2025-12-31 | ||

| Total debt | $112mm | |

| 2025-12-31 | ||

| Net debt | $92mm | |

| 2025-12-31 | ||

| Current assets | $129mm | |

| 2025-12-31 | ||

| Current liabilities | $105mm | |

| 2025-12-31 | ||

| Current ratio | 1.23x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

As of December 31, 2025 per latest annual filing [F1]:

While liquidity appears adequate with a current ratio above one, net losses depress equity metrics with operating margins still negative reflecting ongoing investment cycles amid competitive pressures.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available SEC filings and related disclosures as of May 13, 2026. It does not constitute investment advice or recommendations regarding the securities of A.K.A. Brands Holding Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments