Amkor Technology Bolsters Advanced Semiconductor Packaging with Expanding Global Footprint

Amkor's Q1 2026 results reveal steady revenue growth and capacity expansion amid dynamic semiconductor demand.

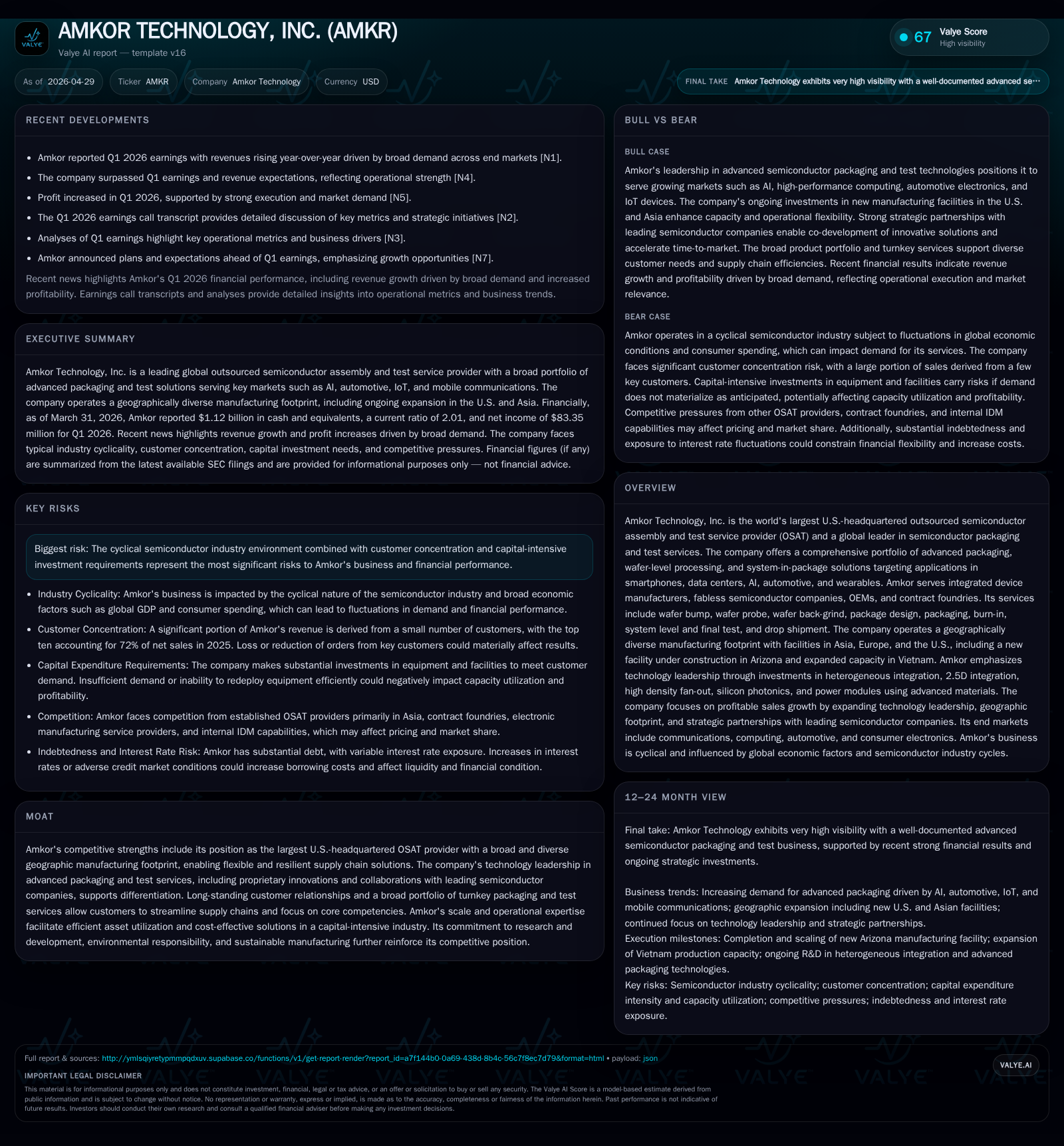

Amkor Technology posted solid Q1 2026 quarterly results underscoring broad-based end-market demand and ongoing capacity investments, including scaling operations in Vietnam and constructing a new plant in Arizona. As the largest U.S.-headquartered OSAT, Amkor leverages an integrated business model offering turnkey packaging and test services critical for advanced semiconductor applications in smartphones, AI, automotive, and data centers. Its differentiated technology portfolio and geographic footprint underpin competitive resilience despite typical semiconductor industry cyclicality and customer concentration risks. Near-term growth will hinge on successful facility qualifications and ramping heterogeneous integration products in emerging high-value sectors.

Q1 2026 Operating Update: Navigating Demand and Capacity Gains

Amkor’s latest quarterly filing dated April 28, 2026 (Form 10-Q) reveals a positive operating trajectory underpinning its market leadership in outsourced semiconductor assembly and test (OSAT) services [S2]. The company reported broadly diversified demand across strategic end markets including smartphones, data centers, automotive systems, and consumer electronics channels—contributing to measured revenue increases in the quarter per recent earnings commentary [N1]. These gains reflect consistent customer procurement patterns despite cyclical uncertainties endemic to semiconductors.

Operationally, Amkor advanced the expansion of its Vietnam manufacturing facility—a key part of its Asia-Pacific footprint enhancement—progressing towards higher utilization rates. Concurrently, construction continues on a state-of-the-art Arizona plant aimed at servicing U.S.-based customers with lower logistics complexity and compliance advantages amid growing regionalization trends [S3]. These capacity augmentation efforts align with sustained R&D investments fueling advanced packaging innovations that support heterogeneous integration demands from high-growth sectors such as AI accelerators and automotive electrification.

The quarter also demonstrated maintained gross margin stability despite input cost pressures characteristic of semiconductor supply chains. This highlights Amkor’s ability to optimize production scale while managing fixed cost leverage during fluctuating order volumes—a critical attribute for profitability in capital-intensive OSAT operations.

Amkor’s Integrated Business Model: Offering End-to-End Packaging and Test Solutions

Amkor’s business model hinges on providing comprehensive semiconductor packaging and test services that span wafer bumping, wafer probe, wafer back-grind, full package design, burn-in testing, system-level final test, and drop shipment logistics [S1]. Customers — including IDMs (Integrated Device Manufacturers), fabless designers, OEMs, and contract foundries — rely on Amkor to transform silicon wafers into ready-to-integrate packaged semiconductors. This turnkey service bundling creates substantial switching costs due to the technical complexity involved as well as qualifying processes unique to each manufacturing site.

Technologically, Amkor commands a leadership position through its focus on advanced packaging formats such as system-in-package (SiP), fan-out wafer level packaging (FOWLP), copper hybrid bonding for dense 3D chip stacking, and co-packaged optics enabling high bandwidth for data centers—a critical differentiator in a crowded OSAT market segment [S18]. Its research hubs primarily based in Korea facilitate continuous innovation tailored towards reducing package footprints while improving electrical performance and thermal management.

By managing the entire value chain internally—from wafer processing steps through final testing—Amkor offers customers improved yield control, reduced cycle times, lower total cost of ownership, and supply chain simplification. This integrated approach is especially appealing to fabless companies concentrating capex on front-end wafer fabrication rather than back-end assembly.

Industry Context: Competitive Dynamics in OSAT and Semiconductor Services

The global outsourced semiconductor assembly and test industry operates under oligopolistic dynamics dominated by large players like ASE Technology Holdings (Taiwan), JCET Group (China), Powertech Technology Inc., alongside Amkor as the leading U.S.-headquartered provider [S1]. Geographic footprint diversity is a critical advantage given ongoing U.S.-China trade tensions incentivizing regionalization of semiconductor supply chains.

Amkor benefits from manufacturing sites across Asia (Vietnam, Philippines, Korea), Europe (Portugal), and North America (Arizona). This multi-regional presence enables it to flexibly allocate production flows based on customer needs and regulatory constraints—dampening risks related to tariffs or export controls notably impacting Chinese competitors less embedded globally [S6].

Nevertheless, pricing pressure persists as foundry consolidation accelerates vertical integration trends among IDMs seeking internal packaging capabilities or strategic partnerships with contract foundries offering bundled front- to back-end services. Facility qualification timelines present high barriers as new plants must meet rigorous customer standards before volume orders commence; this favors incumbents with proven execution track records like Amkor.

Growth Catalysts: Geographic Expansion, Advanced Packaging, and End Market Trends

Key growth drivers identified include:

Geographic Expansion: The scaling of Vietnam's manufacturing capacity complements the timely completion of the Arizona facility. These expansions directly serve increasing U.S. semiconductor end-market demand driven by reshoring policies and supply chain diversification imperatives [S2], [S3].

Advanced Packaging Innovations: Demand for heterogeneous integration solutions such as multi-die modules with ultra-fine interconnects addresses performance limitations posed by Moore's Law scaling. Applications in AI accelerators require co-packaged optics technologies uniquely supported by Amkor’s R&D platform enabling interface bandwidth enhancements—critical for data center operators chasing power efficiency gains [S1], [S18].

End Market Evolution: Strong secular trends from automotive electrification embracing SiC power devices require specialized high-power modules developed by Amkor’s packaging team. Additionally, continued proliferation of smart mobile devices sustains smartphone-related packaging needs alongside emerging AR/VR wearables driving compact system-in-package adoption rates upward.

These factors are expected to ratchet up volume demand as newly built capacities clear customer qualification hurdles with potential near-term milestone updates indicated during recent investor communications [N2].

Risks and Constraints: Cyclicality, Customer Concentration, and Capital Intensity

Amkor explicitly acknowledges vulnerabilities common to OSAT providers:

Semiconductor Cyclicality: Semiconductor pricing volatility coupled with short order backlogs limits revenue visibility requiring disciplined capacity planning to prevent gross margin dilution during downturns where fixed costs remain elevated proportionally higher at low utilization rates [S23].

Customer Concentration: Approximately 72% of net sales derive from the top ten customers with Apple (

30%) and Qualcomm (11%) leading—a concentration that exacerbates sales volatility if any large account alters sourcing strategies or faces its own market headwinds [S6].Capital Expenditure Intensity: Building or upgrading assembly/test plants carries significant capital outlay risk especially around timing uncertainties associated with customer qualification delays which can defer payback periods on these investments [S24].

Geopolitical Trade Barriers: Increasing regulatory constraints impose risks related to export controls potentially affecting cross-border shipments or component sourcing especially for facilities within China or involving Chinese customers foundational to some production flows [S7].

Intellectual Property Legal Risks: Ongoing exposure to patent litigation or claims over proprietary technology may require costly licenses or legal settlements impacting operating results unexpectedly [S26].

Key Developments on the Horizon: Facility Qualifications, Customer Wins, and Market Signals

The company’s near-term operational outlook hinges on several critical execution inflection points:

Arizona Facility Qualification: Successful finishing phases for this new U.S.-based plant will enable servicing critical domestic markets benefiting from localized supply chains amid geopolitical push-pull dynamics. Achieving customer approval remains paramount before commercial volume ramps can commence fully [S3].

Vietnam Throughput Improvements: Improved operational efficiency combined with ramped production volumes as expanded machinery installations reach steady state offer scope for meaningful incremental revenue contribution this year alone [N2].

Adoption in Growth Segments: Further traction securing design wins around heterogeneous integration packages—especially serving data center AI accelerators—and advanced automotive modules will increase content per device metrics thereby driving ASP improvements while reinforcing technological differentiation [N2].

Monitoring these milestones will provide valuable signals into utilization rate trends affecting profitability trajectory.

Financial Profile Snapshot: Liquidity and Capital Structure in Focus

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1121mm | |

| 2026-03-31 | ||

| Current assets | $3.8bn | |

| 2026-03-31 | ||

| Current liabilities | $1867mm | |

| 2026-03-31 | ||

| Current ratio | 2.01x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Amkor maintains a robust liquidity position supportive of ongoing capital-intensive projects required by evolving technology demands. As of March 31, 2026:

This strong current ratio above 2x reflects ample short-term asset coverage over liabilities affording operational agility especially amid elevated CapEx cycles tied to facility expansions and R&D investments focused on emerging packaging technologies [F1], [S2]. While total indebtedness remains substantial historically hovering above $1 billion range—with manageable net leverage after accounting for cash balances—the company must balance debt servicing costs against fluid capital allocation choices in a volatile broader economic context [S13].

This analysis is grounded exclusively on disclosed SEC filings up to April 28th, 2026 ([S1], [S2], [S3]) complemented by contemporaneous news reports ([N1], [N2]). It aims solely to elucidate operating context without offering investment advice or price commentary.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments