MGP Ingredients Confronts Profit Deficit Despite Strong Liquidity in Q1 2026

First quarter results reveal substantial net loss amid robust liquidity, raising questions on growth and operational resilience.

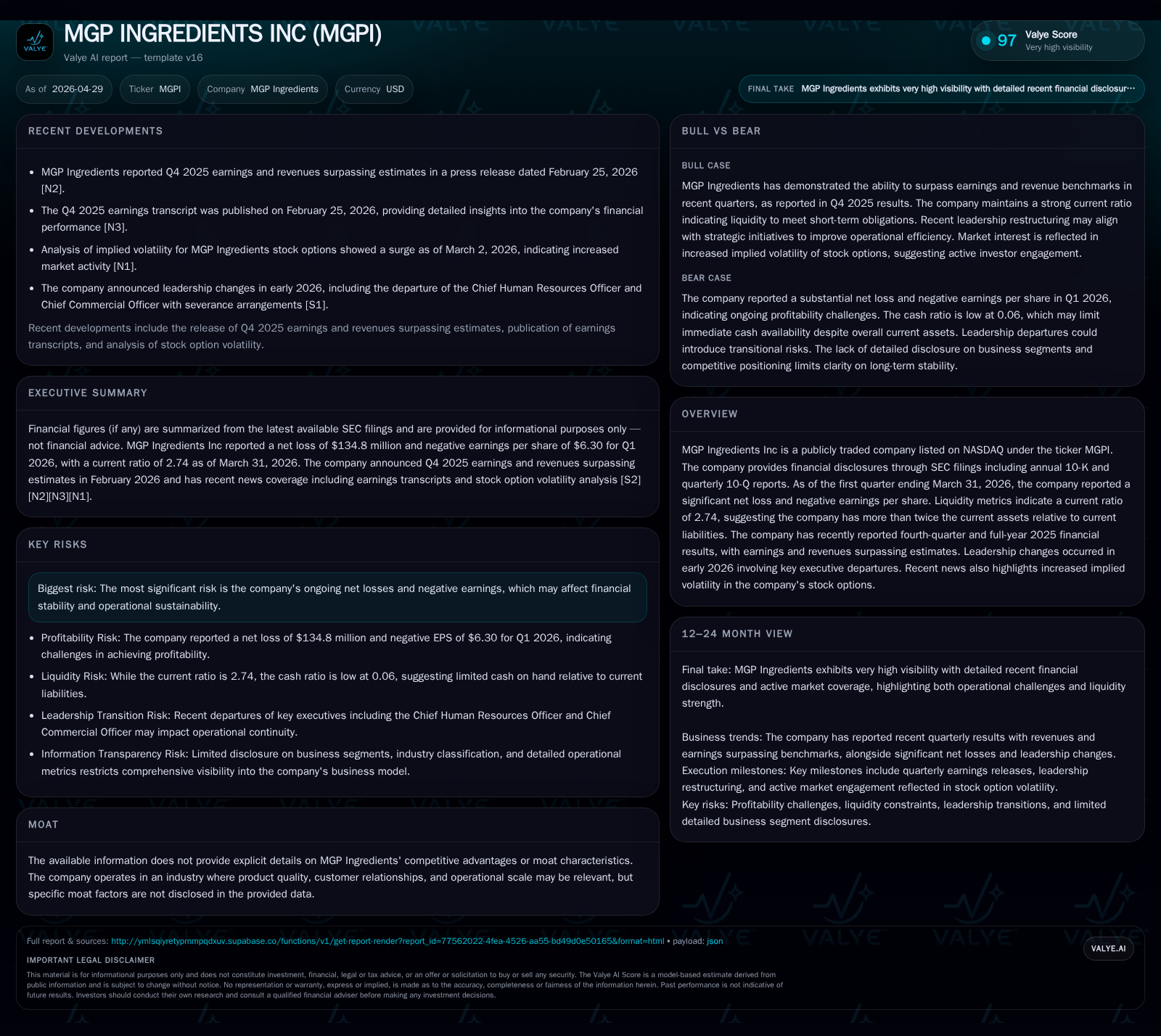

MGP Ingredients reported a significant net loss and negative earnings per share in the first quarter of 2026, marking ongoing profitability challenges. This financial strain contrasts with a strong liquidity position, underscored by a current ratio of 2.74 and substantial current assets exceeding current liabilities. Recent leadership changes add complexity to the company's strategic outlook as it navigates margin pressures and operational realignments. The company’s core business remains centered on grain-based ingredient production, facing industry headwinds including cost dynamics and capacity considerations.

Q1 2026 Results Highlight Significant Net Loss Despite Solid Current Ratio

MGP Ingredients’ latest quarterly filing dated April 29, 2026, lays bare continuing profitability challenges with a pronounced net loss reported for the first quarter ending March 31, 2026 [S2]. While exact Q1 revenue figures are not freshly disclosed, the operating environment is marked by negative earnings per share signaling deteriorating near-term earnings power. Contrasting this bleak income statement is a notably strong liquidity profile: the company reported current assets at approximately $506 million against current liabilities near $185 million, yielding a healthy current ratio of 2.74 as of quarter-end [F1]. This surplus of short-term assets over liabilities indicates significant operational capital cushioning despite operational losses.

Recent event filings also indicate notable shifts in executive leadership with departures of key roles such as Chief Human Resources Officer and Chief Commercial Officer earlier in the year impacting organizational stability [S23]. These developments compound the profit deficit narrative but highlight an active management response to evolving internal challenges.

MGP Ingredients’ Business Model: Core Products and Customer Segments

MGP Ingredients derives its revenues primarily through the production and sale of distilled spirits and specialty food ingredients based on fermented grains—a business rooted deeply in agricultural processing [S1]. The company's product portfolio includes spirits used in consumer beverages and ingredients like wheat proteins used in food manufacturing. Revenue streams stem from sales contracts with beverage producers and food manufacturers reliant on consistent supply quality.

The company leverages scale production capabilities at multiple distillery sites to improve unit economics; however, these scale benefits are subject to raw material input costs that can exert margin pressure if not effectively managed. Customer relationships appear typically long-term but sensitive to product quality consistency and service reliability given the competitive commodity nature of many ingredient segments.

Competitive Dynamics and Industry Positioning in Ingredient Supply

Operating within specialized fermenting ingredient markets places MGP Ingredients among a tightly regulated sector where both commodity pricing dynamics and specialized formulation requirements converge [S1]. Industry competition features several mid-sized ingredient suppliers competing on price, volume flexibility, product purity, and logistical execution.

Capacity utilization plays a critical role here: facilities underutilization can dilute fixed cost absorption while supply chain disruptions—such as raw grain availability or transportation bottlenecks—influence both costs and delivery timelines. Regulatory oversight related to food safety standards adds compliance cost layers that can further pressure margins. Notably, product differentiation remains limited beyond quality certifications or niche specialty offerings; thus pricing power is largely contingent on operational efficiency and maintaining customer trust.

Key Growth Drivers and Expansion Opportunities

Despite recent setbacks revealed in Q1 results, MGP retains levers for growth including optimizing distilling operations—though two Kentucky distilleries were temporarily idled earlier in April 2026 to recalibrate capacity utilization, reflecting an active approach to matching production with demand [S15]. Enhanced sales efforts could target expanding their specialty ingredient footprint or premium distilled products with higher margin profiles.

Organic growth might arise from improved mix favoring value-added products versus commoditized ingredients, along with penetrating emerging food trends emphasizing protein enhancements or artisanal spirits. Capital investments aimed at cost reduction or process automation could also incrementally improve margins. However, these initiatives are tempered by the need to resolve underlying structural issues following reported losses.

Risks and Constraints Impacting Performance Trajectory

The dominant risk theme revolves around ongoing net losses translating into continued cash burn that could test financial resilience absent meaningful operating improvements [S5][S20]. Management turnover presents execution risk due to potential disruptions in strategic continuity and customer account management [S23]. Supply chain fragilities—volatile grain prices or shipment delays—pose additional operational headwinds that can exacerbate margin compression.

Regulatory changes affecting labeling or production methodologies carry inherent uncertainties impacting compliance timelines or cost structures. The cyclical nature of beverage end markets also exposes MGP to demand fluctuations tied to consumer discretionary spending trends.

Upcoming Milestones and What to Watch in 2026

Close monitoring should be placed on upcoming quarterly disclosures for evidence of margin stabilization or return to profitability benchmarks as operations post-distillery idling normalize [S2][S3][S10]. Leadership appointments or announcements clarifying strategic priorities will be potent indicators of organizational direction post-early-year executive departures.

Other focal points include contract renewals with major beverage customers serving as barometers of demand momentum. Tracking capital expenditure patterns or shifts in product mix toward more differentiated offerings would illuminate growth trajectory shifts.

Latest Financial Snapshot: Liquidity, Debt, and Profitability Metrics

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $10mm | |

| 2026-03-31 | ||

| Total debt | $252mm | |

| 2026-03-31 | ||

| Net debt | $242mm | |

| 2026-03-31 | ||

| Current assets | $506mm | |

| 2026-03-31 | ||

| Current liabilities | $185mm | |

| 2026-03-31 | ||

| Current ratio | 2.74x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period Ending |

|---|---|---|

| Cash & Equivalents | 10,357,000 | |

| 2026-03-31 | ||

| Total Debt | 252,450,000 | |

| 2026-03-31 | ||

| Net Debt (Approx.) | 242,093,000 | |

| 2026-03-31 | ||

| Current Assets | 506,049,000 | |

| 2026-03-31 | ||

| Current Liabilities | 184,991,000 | |

| 2026-03-31 | ||

| Current Ratio | 2.74 | |

| 2026-03-31 |

This snapshot underscores how MGP maintains solid liquidity buffers as reflected in a current ratio of 2.74 as of March 31, 2026, despite carrying substantial debt loads characteristic of capital-intensive processing operations.

This analysis is based solely on publicly filed SEC documents as of April 29, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments