Meihua International Medical Technologies: Adapting to Market Headwinds and Regulatory Challenges

Meihua International Medical Technologies confronts Nasdaq delisting and revenue declines while pursuing diversification through SaaS and industrial park ventures.

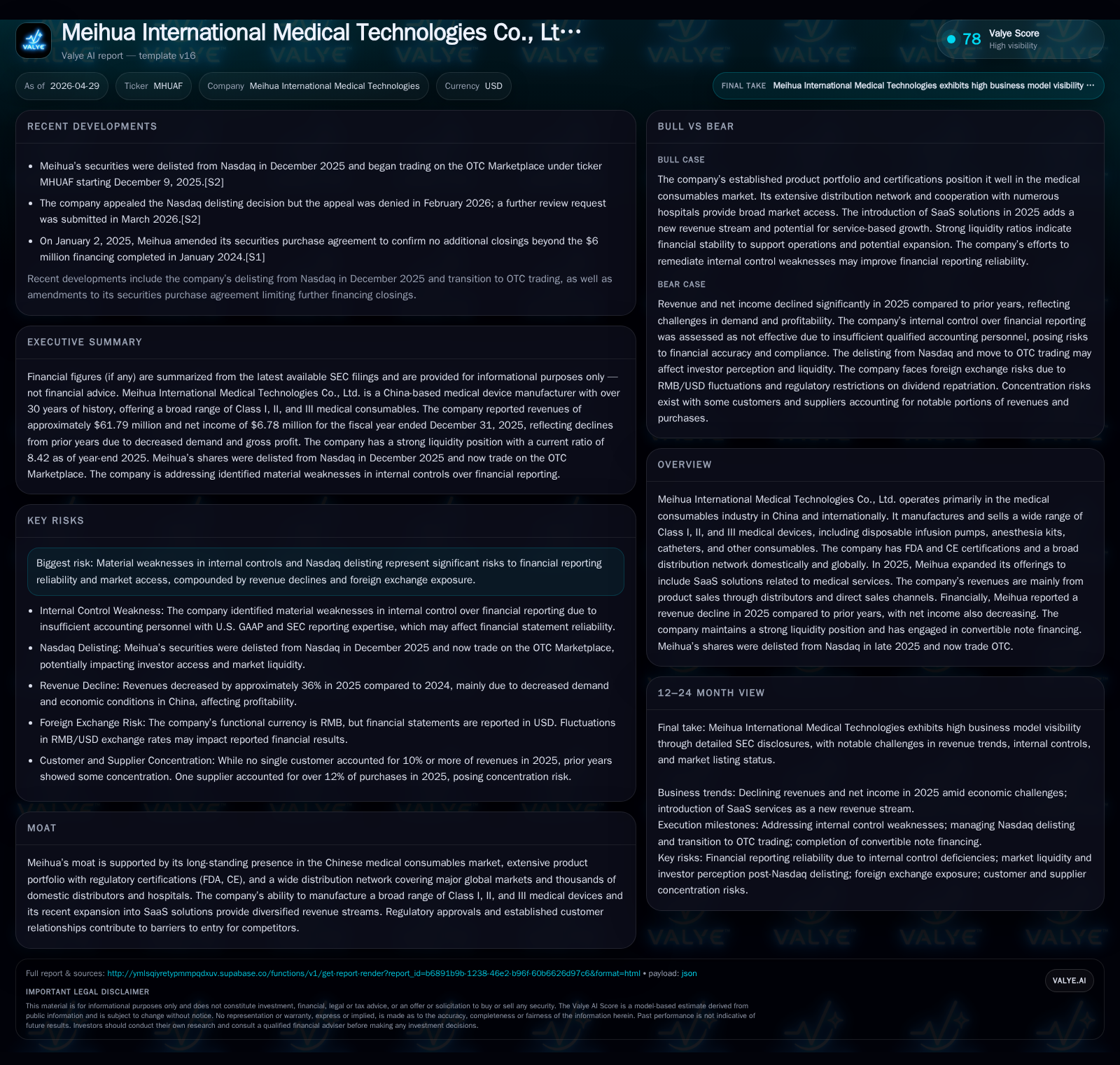

In early 2026, Meihua International Medical Technologies (MHUAF) faced a critical setback as Nasdaq denied its appeal to reinstate listing, transitioning its shares to OTC trading. This regulatory event compounds revenue pressures from a significant decline in 2025, driven by softer demand amid China's economic stagnation. The company leverages its expansive portfolio of FDA- and CE-certified medical consumables and a broad distributor network, while strategizing growth through new SaaS offerings and an industrial park development slated to generate revenue in mid-2026. Risks include ongoing reporting concerns tied to internal controls, currency exposure, and dependence on successful execution of emerging initiatives.

Nasdaq Delisting and Recent Operating Update

On February 24, 2026, Meihua International Medical Technologies received definitive notice from Nasdaq that its appeal to regain listing status was denied following suspension and delisting effective December 2025. Consequently, the company’s Class A ordinary shares transitioned to trading on the OTC Marketplace under ticker "MHUAF" starting December 9, 2025 [S2]. This marked regulatory development profoundly impacts Meihua’s market liquidity and investor access, constraining visibility and potentially deterring institutional participation accustomed to major exchange listings.

The delisting arose under Nasdaq Listing Rule 5815(c), though specific underlying deficiencies were not detailed in the public filing. The company responded swiftly by requesting a further review by the Nasdaq Listing and Hearing Review Council as of March 2, 2026 [S2]. Meanwhile, management continues regular disclosures via SEC filings but acknowledges these events underscore heightened compliance and operational scrutiny.

This regulatory setback coincides with pronounced revenue pressures experienced in fiscal year 2025. Total revenues contracted approximately $35 million year-over-year (36%) to $61.79 million from $96.91 million in 2024 [S1], symptomatic of weakening customer demand amid a stalling macroeconomic backdrop in China impacting healthcare procurement cycles. Net income similarly declined by 37% to $6.78 million largely driven by compressed gross margins reflecting pricing pressure or cost inflation [S1]. This combination of operational headwinds framed within the latest quarterly filing articulates why strategic pivoting is imperative.

Business Model Nuances and Product Quality Overview

Meihua operates primarily as a manufacturer and distributor of a broad assortment of Class I-III medical consumables with more than three decades of experience and regulatory credentials securing FDA registration alongside European Union CE certification — crucial endorsements that enable global market access across stringent regulatory jurisdictions [S1]. The product suite encompasses disposable infusion pumps, anesthesia puncture kits, electronic pumps, urethral catheterization kits, gynecological examination kits, endotracheal intubation devices, dressing supplies, and various tubing products totaling over 800 domestic SKUs complemented by more than 400 export SKUs internationally [S1].

Revenue generation centers on sales to distributors—approximately 4,409 domestically covering major Chinese medical institutions and pharmacies—and direct sales channels servicing over 573 hospitals nationwide [S1]. International distribution leverages a network of roughly 403 exporting distributors reaching markets across Europe, North America, Asia, South America, Africa, and Oceania. This wide yet specialized distribution footprint deepens switching costs for clients due to integrated supply relationships combined with product quality assurances stemming from comprehensive certifications.

In addition to physical product sales, Meihua has begun offering Software as a Service (SaaS) solutions targeting healthcare infrastructure digitization including cloud-based platforms coupled with implementation services plus ongoing technical support designed to optimize hospital and clinic workflows. Although this SaaS segment remains at an emergent stage relative to the core consumables business volume-wise, it represents strategic product diversification aligned with evolving industry trends favoring integrated digital solutions [S1].

Competitive Positioning and Industry Dynamics

Operating within China’s competitive medical consumables sector—the largest globally—Meihua benefits from entrenched brand recognition sustained by regulatory clearances that form high barriers for new entrants needing time-consuming approvals for Class II/III devices especially under FDA/CE regimes [S1]. However, the industry exhibits demand cyclicality linked closely to public health spending patterns; recent softness reflects macroeconomic stimuli lagging recovery post-COVID disruptions affecting elective procedures and capital procurements.

Pricing power is modest given commoditized nature of many disposable items but partially cushioned by differentiated premium lines such as advanced infusion pumps where technology sophistication justifies fewer direct substitutes. The vast distributor network (over 4,800 total globally) serves as both moat and operational complexity driver: scale enables broad market coverage but mandates sophisticated logistics plus credit risk management under volatile end-market conditions.

Regulatory oversight continues intensifying not only from authorities but also marketplace expectations for hygienic standards post-pandemic elevating entry barriers further yet pressuring manufacturers towards continual R&D investments for compliance adherence without assured proportional revenue uplift [S1].

Growth Drivers: Diversification and Industrial Park Development

Amid slowing core device sales growth contributing to recent top-line decline, Meihua pursues emerging growth avenues anchored on two principal initiatives as outlined in its latest annual filing:

Medical Industrial Park in Hainan Free Trade Port: Construction commenced on a specialized facility aimed at fostering manufacturing innovation while leasing space to related medical device tenants. Phase I interior fit-out is expected for completion with tenant lease commencement projected around July 2026 pending successful tenant demand traction [S1]. This long-cycle asset development aims at generating stable rental income diversifying away from product sales volatility though subject to construction delays or government policy shifts typical for infrastructure projects.

Healthcare SaaS Platforms: Offering cloud-hosted software products supporting online health consultations among other services marks Meihua's entry into the digital health segment broader than simple device manufacturing. While currently nascent without material revenue contribution noted yet evolving strategy includes incremental ramp supported by technical service teams delivering implementation and system optimizations essential for client retention [S1].

The company also discloses exploratory efforts designing an AI-assisted robotic surgery (RAS) system—a clearly experimental long-horizon project signaling intent to participate beyond consumables into higher-tech medtech fields but presently without commercialization progress or tangible financial input [S1].

Key Risks and Operational Watchpoints

Significant risks stem from material weaknesses historically identified in internal controls that undermine reliability perceptions of financial reporting compounded directly by the adverse effect of Nasdaq delisting restricting capital markets access and investor confidence levels [S1,S2]. Such reputational capital impairments could hamper future financing endeavors or strategic partnerships critical for growth funding.

Financial results remain exposed to foreign exchange volatility due to RMB functional currency operations translating into U.S. dollar reporting metrics with RMB exhibiting appreciation/depreciation swings (~4.2% appreciation in 2025) adding layers of earnings unpredictability unrelated directly to operating performance [S1]. The absence of formal hedging policies leaves net income susceptible amid increasingly complex geopolitical currency relations.

Cybersecurity poses operational continuity risk given increasing institutional reliance on interconnected information systems; Meihua maintains an extensive Cybersecurity Incident Management System overseen directly by senior leadership including board representation underscoring governance awareness but the landscape remains fraught with broad-spectrum threats requiring ongoing vigilance investments [S1].

Lastly, the company’s balance sheet shows a strong liquidity position with a current ratio of 8.42 as of December 31, 2025, supported by current assets of approximately $154 million against current liabilities of $18 million [F1]. This indicates manageable short-term liabilities and preserved liquidity buffers despite external market stressors. Monitoring capital raising activities remains important given ongoing strategic initiatives and market conditions.

Forward-Looking Milestones and Execution Metrics

Investors should track several catalyst points including:

- Outcomes from the Nasdaq Listing Review Council appeal process following the February delisting denial which could theoretically alter secondary market visibility though prospects appear limited based on prior rulings [S2];

- Progress updates regarding tenant acquisition velocity in Hainan industrial park ahead of anticipated July 2026 leasing start date; initial tenant leases secured indicate some momentum but sustained occupancy crucial for steady-state profitability realization [S1];

- Adoption rates and subscription growth metrics for SaaS healthcare platforms once publicly reported will illuminate market receptivity versus existing entrenched competitors across software-enabled health services;

- Quarterly order flow trends tied closely to China’s macro recovery signals impacting medical consumable restocking cycles giving leading directional indications on when bottoming/bounce-back may be expected post-weakness documented in FY25 revenues [S1,S2];

- Pipeline developments relating to AI surgical robotics remain speculative but any alpha-stage breakthroughs or partnership announcements could materially alter longer-term innovation narratives.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $154mm | |

| 2025-12-31 | ||

| Current liabilities | $18mm | |

| 2025-12-31 | ||

| Current ratio | 8.42x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

(Measured at fiscal year-end December 31, 2025 except for current ratio based on year-end current assets/liabilities) shows a marked contraction in top-line compared with prior years alongside solid operating profitability margin maintenance albeit at reduced absolute earnings levels consistent with headwinds discussed above [F1]. Meihua International Medical Technologies balances entrenched product strengths against significant regulatory-driven challenges as it seeks new growth vectors amidst macroeconomic uncertainty.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments