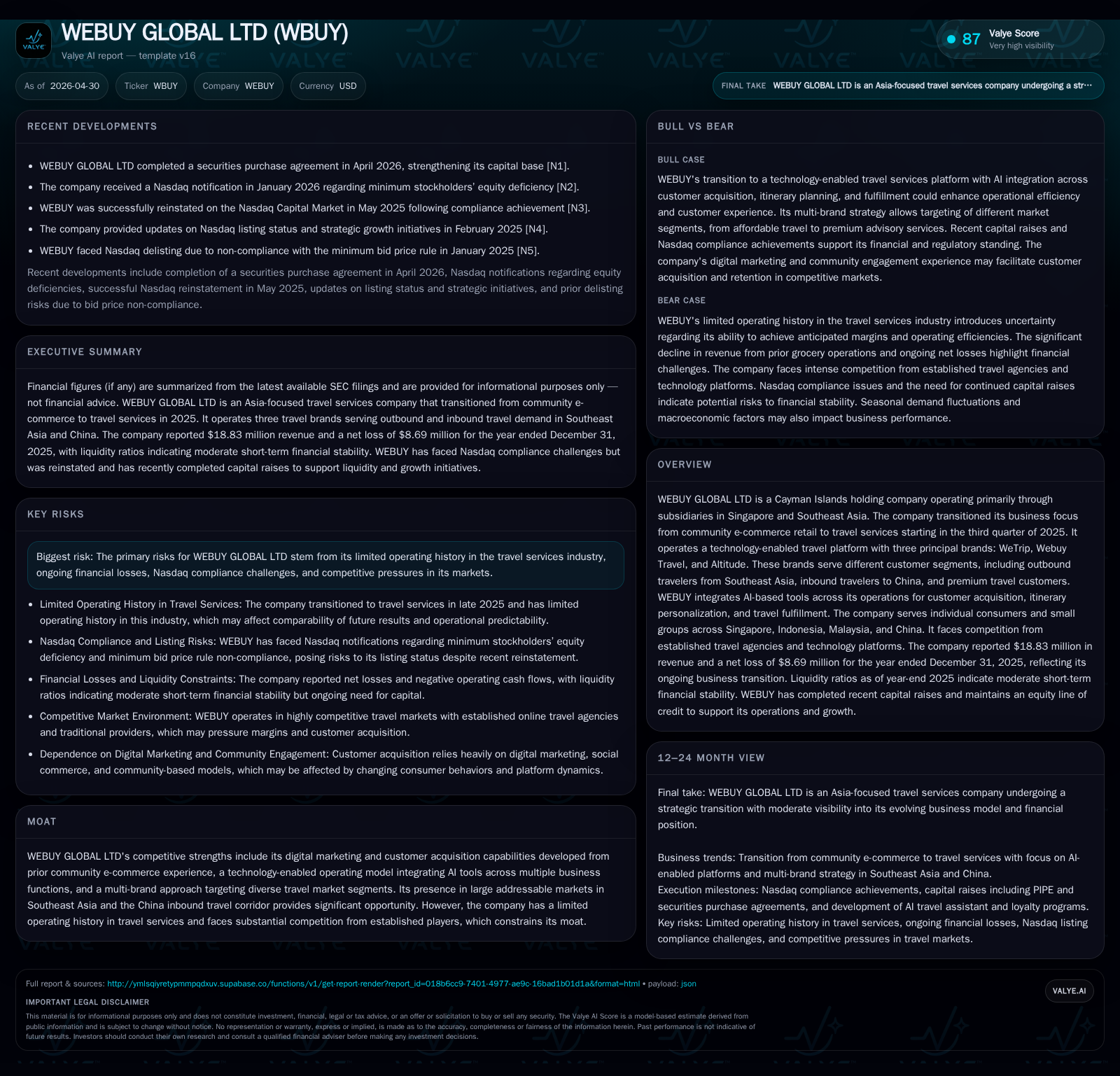

WEBUY GLOBAL LTD’s Strategic Pivot to Travel Services Challenges Profitability Amid Market Competition

Recent share issuances and operational shifts mark WEBUY GLOBAL’s transition from e-commerce to a technology-driven travel platform, spotlighting growth opportunities and mounting financial pressures.

WEBUY GLOBAL LTD executed significant equity transactions in early 2026, reinforcing liquidity as it continues its strategic shift from Southeast Asian grocery e-commerce to a travel services business. The company’s AI-augmented multi-brand platform targets diverse regional travel segments but faces competitive pressure and limited industry tenure. While packaged tours revenue grew by 24% in 2025, total revenue declined sharply due to winding down of grocery operations. Operational losses persist amid ramped marketing and credit provisions, underscoring the challenge of scaling sustainably in a fragmented, competitive travel market.

Recent Operating Update: Equity Raises Support Strategic Shift

In April 2026, WEBUY GLOBAL LTD completed several significant shareholder transactions that materially affect its near-term liquidity and capital structure. The company issued 300,000 Class A ordinary shares worth approximately $351,000 as part of supplemental compensation for CEO Bin Xue [S2]. Separately, Mr. Xue purchased 100,000 Class B ordinary shares at market price totaling $117,000; these Class B shares convey enhanced voting rights but no dividends [S2].

Earlier in March 2026, WEBUY closed a private investment in public equity (PIPE) financing raising $1 million with issuance of approximately 1.14 million Class A shares at an effective price of $0.88 per share [S3]. This PIPE tranche represents close to 23% ownership dilution of Class A common stock outstanding at the time [S3].

Business Model: Technology-Enabled Travel Services Platform

WEBUY operates as a Cayman Islands holding company with key subsidiaries in Singapore serving Southeast Asia markets [S1], transitioning since Q3 2025 from grocery retail—with discontinued operations now segmented—to a technology-enabled travel platform business [S1]. It focuses on three distinct brands:

- WeTrip: Targets international travelers from Western countries like the US, UK, Australia visiting China and Asia.

- Webuy Travel: Serves local Southeast Asian outbound travelers primarily in Singapore and Indonesia offering affordable global travel experiences.

- Altitude: Caters to premium clients seeking curated luxury travel with AI-assisted itinerary personalization.

The core value proposition hinges on integrating advanced AI-based tools across customer acquisition channels—including digital marketing—and throughout itinerary curation and fulfillment processes [S1]. This digital foundation facilitates scalable customer engagement through personalized experiences that differentiate from conventional travel agents.

Revenue derives mainly from packaged tour sales where clients pay upfront or via advance deposits (reflected partially as deferred revenue), supplemented by service fees embedded within offerings. Margins depend on supplier cost management, pricing discipline facilitated by proprietary tech insights, and operational efficiencies.

However, WEBUY’s operational tenure in travel services remains limited since its pivot post-Q3 2025; prior experience was rooted in social commerce-driven grocery distribution [S1]. This transition reflects a deliberate strategic reorientation targeting higher-margin categories after assessing long-term viability constraints of the grocery segment.

Industry Structure and Competitive Position

The regional travel services industry is highly fragmented with numerous legacy agencies entrenched alongside emerging online platforms employing sophisticated technology stacks. WEBUY confronts strong incumbent competition across both inbound Chinese tourism corridors and outbound Southeast Asian segments [S1]. This marketplace also includes dominant players leveraging larger scale marketing budgets and established supplier networks.

Despite these challenges, WEBUY leverages two competitive advantages:

- Deep digital marketing expertise inherited from community e-commerce enables efficient customer acquisition via social media channels and referral networks.

- AI integration offers differentiated itinerary personalization tools enhancing customer satisfaction relative to more traditional agents.

Nevertheless, given the nascent stage of its travel business operations, its overall moat remains constrained by limited brand recognition among premium travelers and modest scale compared to incumbents.

Growth Drivers

Expansion of Packaged Tour Revenues

In fiscal 2025, WEBUY grew packaged tour services revenue by approximately 24.4% to $18.39 million even as total continuing operations revenue declined due to cessation of grocery activities [S13]. This reflects increasing customer adoption driven by:

- Geographic expansion within Singapore and Indonesia targeting growing middle-class outbound travelers.

- Enhanced digital marketing campaigns improving lead generation quality.

- Diversification into premium segments via the Altitude brand tapping wealthier clientele seeking tailored experiences.

Increasing Customer Prepayments & Deferred Revenue

The rise in deferred revenue by around $2.39 million indicates stronger advance bookings supporting near-term cash flow improvements [S7]. This signals improved operational momentum as trust builds around WEBUY’s service reliability.

Technology Platform Maturation & AI Enhancements

Ongoing investment in AI-assisted itinerary design aims to continuously refine personalization algorithms enhancing customer retention rates. Moreover, this improves cross-selling potential across the multi-brand ecosystem [S1].

Equity Financing & Capital Availability

Successful private placements and access to a $20 million equity line-of-credit (ELOC) provide optionality for capex or marketing investments needed for scaling operations under favorable terms [S4].

Risks / Watchpoints / Growth Constraints

Limited Operating History & Transition Risk

Having ceased grocery operations fully only recently leaves limited financial comparability historically [S1]; management faces execution risk scaling a relatively new business model amid volatile international tourism environments influenced by geopolitical or health factors.

Ongoing Financial Losses & Cash Burn

Operating losses widened to $6.62 million for FY 2025 with net loss exceeding $8.5 million reflecting elevated selling expenses ($1.47 million) including aggressive marketing spend plus notable expected credit loss provisions ($2.47 million) on aging receivables [F1][S23]. Although cash outflow improved YOY due to receivable collections pushdown net operating cash used remained negative [$2.93 million] [S7].

Nasdaq Listing Compliance Concern

The company received Nasdaq deficiency notices related to minimum stockholders’ equity requirements below mandated $2.5 million levels as of June 30, 2025 but has submitted compliance plans backed by capital raises [S14][S16]. Failure here could adversely impact investor confidence and trading liquidity.

Stiff Competition & Customer Retention Challenges

Digital marketing advantages may be eroded as competitors increase spend or improve tech capabilities; client acquisition costs may rise disproportionately disrupting growth economics.

What to Watch Next

- Execution on converting PIPE investment proceeds into tangible market share gains sustained beyond initial acquisitions.

- Utilization and drawdown progress under the existing ELOC facility providing financial runway for growth investments [S4].

- KPIs around deferred revenue growth indicating advance bookings' acceleration or stagnation reflecting consumer confidence.

- Management's ability to control credit risks evidenced by reduction in expected credit loss provisions over subsequent quarters.

- Product innovation milestones integrating AI enhancements further personalizing itineraries that can foster higher margins or upsell opportunities.

- Regulatory developments impacting inbound China tourism flows or outbound Southeast Asia leisure tendencies post-pandemic normalization.

- Monitor management team stability given recent leadership transitions affecting execution capability [S18][S19].

Financial Profile Summary (Latest Available Annual Data)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $13.68mm | |

| 2025-12-31 | ||

| Current liabilities | $11.90mm | |

| 2025-12-31 | ||

| Current ratio | 1.15x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Revenue | $18.83M | |

| 2025-12-31 | ||

| Operating Income | -$6.62M | |

| 2025-12-31 | ||

| Net Income | -$8.53M | |

| 2025-12-31 | ||

| Cash & Equivalents | $4.15M | |

| 2024-12-31 | ||

| Total Debt | $0.17M | |

| 2024-12-31 | ||

| Current Assets | $13.68M | |

| 2025-12-31 | ||

| Current Liabilities | $11.90M | |

| 2025-12-31 | ||

| Current Ratio | ~1.15x | |

| 2025-12-31 |

Liquidity remains tight but manageable with positive working capital supported largely by advances collected from customers rather than profitable operations at present [F1][S7]. Operating cash flow improved significantly YOY yet stays negative consistent with ongoing expansion investment stage.

This analysis is for informational purposes only based on publicly available SEC filings and does not constitute investment advice or recommendations regarding WEBUY GLOBAL LTD’s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments