General Dynamics Strengthens Quarterly Performance on Steady Defense Demand

Q1 2026 results underscore General Dynamics' robust contract portfolio and liquidity amidst stable defense spending.

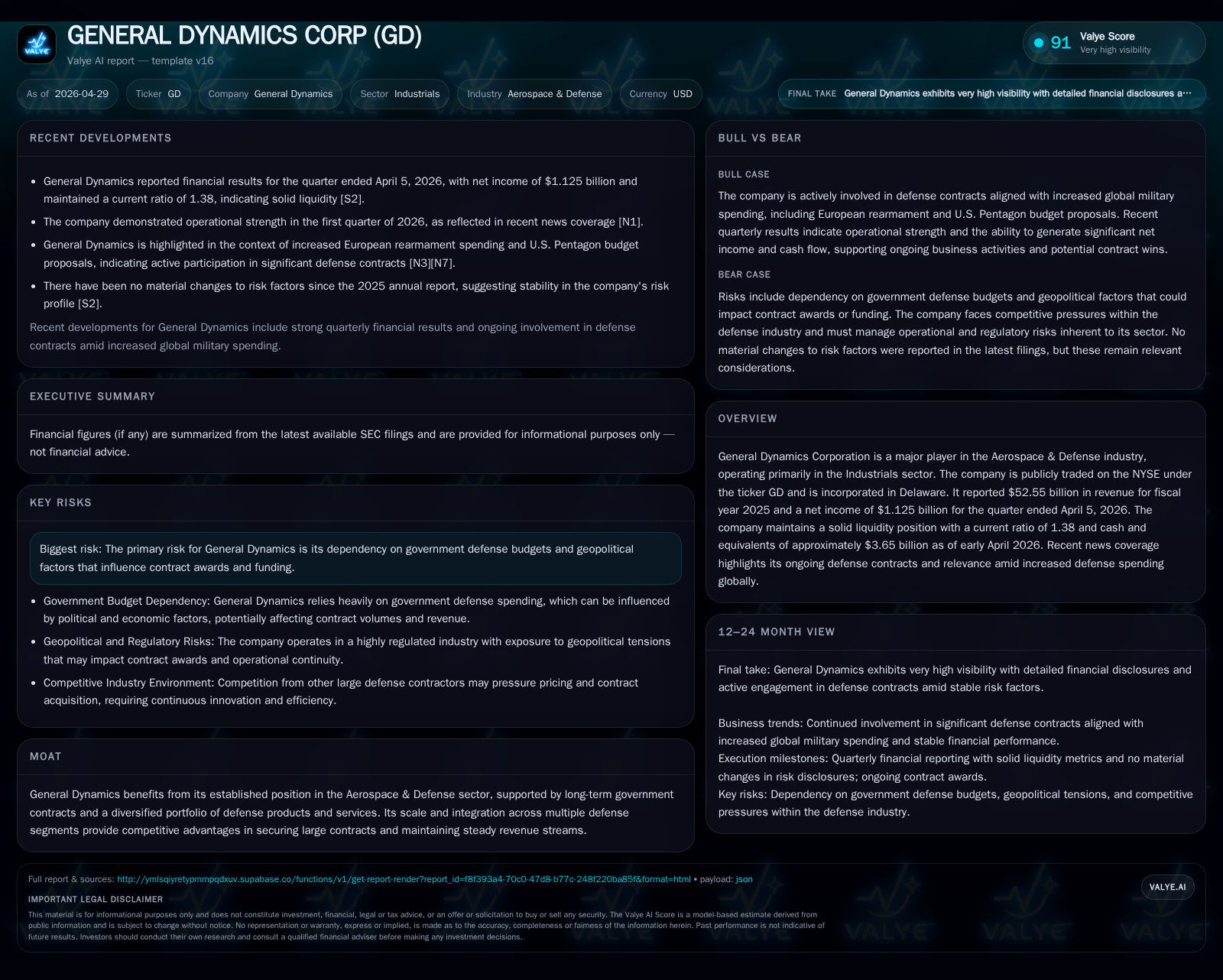

In Q1 2026, General Dynamics posted solid financial results highlighted by a net income of $1.125 billion and demonstrated a strong liquidity position with a current ratio of 1.38 supported by $3.65 billion in cash. The company’s diversified aerospace and defense business model, anchored in long-term government contracts across land, marine, and aerospace systems, continues to underpin steady revenue streams and margin stability. Growth prospects are bolstered by rising government budgets, innovation in next-gen defense technologies, and expanding international engagements, while risks remain related to geopolitical uncertainties and federal budget variability.

Quarterly Operating Update Highlights: Solid Earnings and Contract Wins

General Dynamics Corporation (GD) reported strong first-quarter results for the period ended April 5, 2026, per its April 29, 2026 Form 10-Q filing [S2] and supporting Form 8-K announcement [S3]. The company recorded net income of $1.125 billion for the quarter—a notable figure that confirms operational strength amid ongoing demand for defense products [F1]. This performance aligns with an annual revenue base of $52.55 billion reported for fiscal year 2025 [F1]. Liquidity remains robust as evidenced by a current ratio of 1.38 and cash & equivalents approximating $3.65 billion at quarter-end [F1], providing ample flexibility for funding working capital requirements or strategic investments.

While no material changes were noted in risk disclosures compared to the prior annual report [S2], the company reaffirmed its steady contract position including sizable backlogs that underpin near-term revenue visibility [S3]. This operational update highlights GD’s ability to sustain earnings quality even as the broader geopolitical environment evolves.

Business Model Overview: Diversification Across Aerospace & Defense Segments

General Dynamics operates a diversified business model segmented primarily into Land Systems, Aerospace Platforms, Marine Systems, and Technologies & Training divisions according to its latest annual report [S1]. Its revenue streams derive chiefly from long-term procurement contracts with multiple U.S. government agencies including the Department of Defense, enhanced by select international customer engagements.

The Land Systems segment provides armored vehicles critical to modern military operations; Aerospace Platforms focuses on business jets alongside military aviation components; Marine Systems builds nuclear-powered submarines and surface ships vital for naval supremacy; Technologies & Training offers command and control systems alongside simulation solutions for military readiness.

This multi-segment diversification not only spreads risk across different defense domains but also creates embedded switching costs through complex integration requirements inherent in prime contractor roles. Moreover, many contracts span multiple years with recurring maintenance or upgrade components that bolster margin sustainability and cash flow predictability over extended cycles.

Competitive Positioning Within Aerospace & Defense Sector

Operating within a consolidated industry dominated by formidable peers such as Lockheed Martin or Northrop Grumman [S1], General Dynamics benefits from significant scale advantages allowing it to participate competitively in large multi-year deal procurements both domestically and abroad. Its entrenched government relationships facilitate superior access to contract pipelines, particularly against newer entrants lacking these established credentials.

The company's technology investments support differentiation—especially in emerging fields like advanced cybersecurity solutions and hypersonic weaponry—that enable defense customers to upgrade capabilities amid shifting threat environments. Stable government budgets generally underpin steady pricing power; however, contracting cycles tend to be elongated due to regulatory complexities and capital intensity associated with large platform deliveries.

Market consolidation further narrows competitive pressure but also raises barriers to entry given stringent compliance standards and sophisticated technological requirements faced by suppliers.

Key Growth Catalysts: Government Budgets, Product Innovation & International Expansion

Growth momentum for General Dynamics is largely tethered to structural drivers rather than cyclical fluctuations. Central among these is sustained incremental increases in U.S. defense spending highlighted in recent policy proposals targeting enhanced readiness amid geopolitical tensions [N11][N12]. Moreover, European rearmament efforts open new demand corridors internationally supporting export-oriented sales growth [N9].

Innovation remains crucial; GD is channeling R&D resources into next-generation systems such as hypersonics, cyber-defense capabilities, networked command & control platforms as well as autonomous systems outlined in its filings [S1]. These emergent product lines respond directly to evolving warfare paradigms emphasizing speed, precision, and digitalization.

Complementing organic growth is strategic penetration into allied foreign militaries where modernization programs require advanced integrated platforms—this geographical diversification lessens dependency on any single government budget cycle while extending contract tenure profiles.

Risks and Constraints: Budget Volatility and Geopolitical Headwinds

Despite operational strengths, General Dynamics faces notable risks chiefly related to governmental budget processes which remain inherently uncertain especially under changing political administrations or shifting congressional priorities as documented in its latest risk disclosures [S1][S9]. A significant portion of revenue depends on federal contracts susceptible to appropriation delays or reallocations.

Geopolitical dynamics also impose risks for international contract awards with export controls, regulatory scrutiny, or diplomatic shifts potentially delaying deals or modifying terms. Supply chain complexity inherent in aerospace & defense manufacturing—including vulnerabilities exposed during recent global disruptions—adds execution risk layers impacting delivery schedules or input costs.

Competitive prize bidding can intensify given overlapping capabilities offered by other prime contractors aiming at similar program wins impacting pricing flexibility.

Future Watchpoints: Guidances, Next Contract Awards, and Margin Trajectory

Stakeholders should watch forthcoming quarterly disclosures for management commentary on margin progression reflecting operational efficiencies versus inflationary cost pressures which may temper profitability trends [S3]. Monitoring backlog composition updates provides insights into anticipated revenue trajectories especially as new contracts are secured or existing programs enter different phases.

Upcoming milestone events such as major platform rollouts or service expansions could function as tangible growth indicators validating strategic execution plans discussed in earnings calls referenced by analysts [N6][N8]. Given the cyclical yet sticky nature of defense contracting pipelines, signs of accelerating order intake will be crucial signals.

Additionally, any changes in the U.S. or allied governments’ procurement strategies influenced by global security developments will materially impact GD’s medium-to-long term outlook.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3.7bn | |

| 2026-04-05 | ||

| Current assets | $26.1bn | |

| 2026-04-05 | ||

| Current liabilities | $18.8bn | |

| 2026-04-05 | ||

| Current ratio | 1.38x | |

| 2026-04-05 |

Source: SEC companyfacts cache [F1].

| Metric | Value |

|---|---|

| Revenue (FY25) | $52.55B |

| Net Income (Q1) | $1.125B |

| Cash & Equivalents | $3.65B |

| Current Ratio | 1.38 |

This snapshot reflects a healthy financial foundation with substantial liquidity facilitating capital allocation optionality—including potential acquisitions—and buffer capacity against funding volatility typical within government contracting sectors [F1]. Net debt levels are manageable considering cash holdings supporting strategic agility.

Disclaimer: This analysis is prepared solely for informational purposes based on publicly available filings and news sources. It is not intended as investment advice or a recommendation regarding any securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments