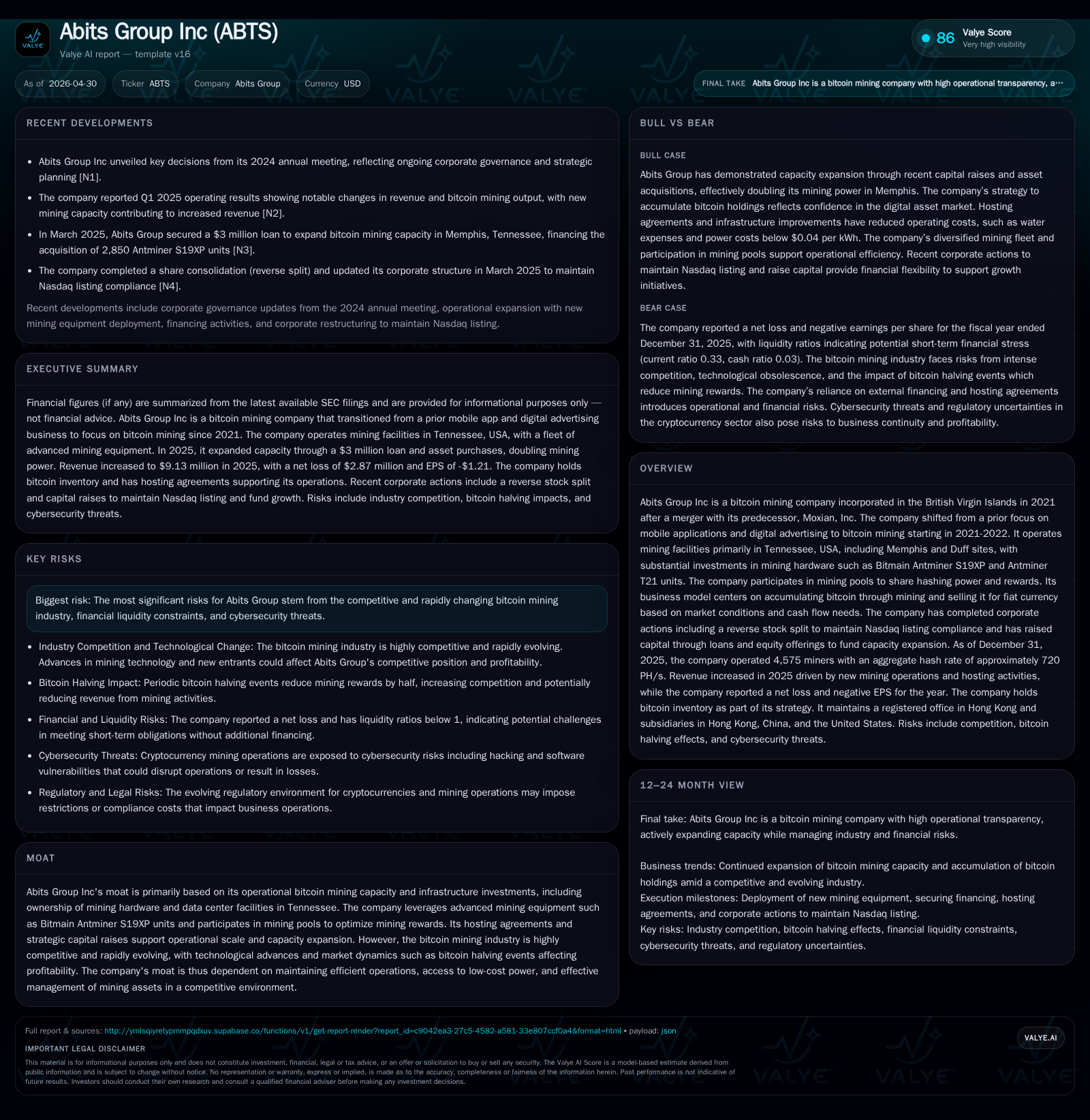

Abits Group Accelerates Bitcoin Mining Capacity Expansion with Advanced Hardware Deployment

Abits Group Inc doubled its US bitcoin mining capacity in 2025 through new Antminer installations and strategic hosting agreements.

In its latest quarterly filing, Abits Group Inc reported significant progress in scaling its bitcoin mining operations by doubling power capacity from 10MW to 22MW via deployment of 2,850 Antminer S19XP units in Memphis, Tennessee. The company's shift from a failing mobile app business to focused bitcoin mining underpins its current model: owning proprietary mining hardware and facilities while balancing bitcoin accumulation with periodic sales. Despite industry challenges such as bitcoin halving events reducing rewards, Abits benefits from low electricity costs, hosting partnerships, and recent capital raises to sustain growth. Risks include sector competition, technology obsolescence, and financial leverage, while upcoming metrics to monitor include hashing power growth, bitcoin holdings, and cost efficiencies.

Recent Operating Update

Abits Group Inc’s latest quarterly filing dated April 29, 2026 ([S2]) reveals the company’s audited financial results for the fiscal year ended December 31, 2025. The primary near-term development is the successful expansion of its bitcoin mining capacity in the U.S., particularly in Tennessee. During early 2025, Abits secured a $3 million loan specifically earmarked for purchasing roughly 2,850 units of Bitmain Antminer S19XP miners. These machines were fully deployed by late March 2025 at its Memphis facility ([S1],[S14]). This move effectively doubled the company’s mining operational power from an initial 10MW to approximately 22MW.

By year-end 2025, the company operated a combined fleet of about 4,575 miners across Tennessee locations (Memphis and Duff), translating into an aggregate hash rate of approximately 720 petahashes per second (PH/s). The mix comprises primarily Antminer S19XP air-cooled (2,991 units) and hydro-cooled (1,299 units) models alongside a smaller number of Antminer T21s (285 units) ([S1]). Notably, the upgraded hydro-cooling initiatives have contributed to operational efficiency by lowering cooling costs through increased use of hydro-power at off-peak times.

The company reported revenue growth from $6.71 million in 2024 to $9.13 million in 2025 (+37%), driven principally by income generated from newly commissioned Memphis miners which started contributing in late Q1. Additionally, Abits began generating auxiliary hosting revenues totaling over $300K through contractual arrangements with the local utility board where it hosts equipment under a joint venture structure ([S1],[S10]).

Cost of revenue totaled approximately $5.45 million with electricity consumed primarily at the Duff site ($2.76 million) and hosting fees at Memphis ($1.92 million) constituting major components ([S1]). Despite rising scale and debt interest cost related to the expansion loan (12% simple interest), operating profit before depreciation and amortization improved slightly to $3.68 million (versus $3.38 million prior year). However, depreciation expense swelled by around $0.9 million owing to additional hardware capitalization ([S1],[S14]).

Mining output was somewhat subdued relative to prior years due mainly to the April 2024 Bitcoin network halving event which reduced block rewards by half, resulting in mined bitcoins totaling approximately 89 compared to historical levels above 100 BTC annually ([S1],[S28]). Management signaled a strategic shift towards holding mined bitcoin reserves on balance sheet — increasing total BTC holdings more than sixfold during the year from approximately 2.58 coins to nearly 16 coins — reflecting long-term confidence amid market volatility.

Business Model

Abits’ business model centers on acquiring and operating dedicated bitcoin mining hardware located primarily within North American sites, notably Tennessee-based facilities in Memphis and Duff ([S1],[S11]). The company procures cutting-edge ASIC mining machines such as Bitmain’s Antminer S19XP series — both air- and hydro-cooled variants — plus newer T21 units that offer hash rates up to around 64 terahashes per second (TH/s) per unit ([S11],[S17]). Revenue is generated mainly through two channels: direct income from mined bitcoins credited on successful block discoveries—enhanced via participation in mining pools that allocate rewards based on contributed hash rates—and fees earned by hosting third-party equipment utilizing excess electrical capacity.

Mining involves substantial capital expenditures on high-performance equipment and the requisite infrastructure (power delivery systems, cooling technologies). The company leverages contract-based hosting arrangements with utility providers allowing for scale flexibility while optimizing energy cost efficiencies that are crucial given electricity represents one of the largest variable expenses ([S10],[S14]). Off-peak operation scheduling combined with hydroelectric cooling has demonstrably curtailed water usage costs by nearly half during FY25 ([S1]), directly benefiting margins.

Crucially, Abits’ approach includes selective bitcoin accumulation rather than immediate sale optimizing for market conditions or corporate liquidity needs ([S11]). This balance between holding digital assets and monetization serves as a tactical hedge against bitcoin price fluctuations inherent in the volatile crypto ecosystem.

Industry Structure and Competitive Position

The bitcoin mining industry is highly competitive with participants ranging from individual hobbyists to globally scaled enterprises operating multi-site data centers []. Companies compete on hash rate capacity, energy cost advantages, geographic diversification, and technology edge.

Abits operates mainly within the U.S., where access to low-cost power sources including hydropower offers a strategic advantage versus regions with higher energy prices []. Hosting agreements with local utilities enhance reliability of electricity supply critical for continuous mining operations.[S10] However, technological innovation cycles demand ongoing reinvestment as newer ASIC models emerge rapidly which may render older fleets uneconomical if not phased out prudently ([S11],[S28]).

Its participation in mining pools helps stabilize reward volatility but introduces fee structures around ~2% which must be balanced against solo operational benefits ([S29]).

Relative to larger public miners or vertically integrated crypto firms possessing massive scale or proprietary software capabilities,[] Abits remains mid-sized but has pursued aggressive capacity build-out since shifting wholly into this sector post-2021 merger with predecessor Moxian.[]

Growth Drivers

- Capacity Expansion: Continued procurement/deployment of advanced ASIC miners supporting hash rate growth enhances potential mining rewards assuming constant difficulty levels.[S17]

- Operational Efficiency: Cost control through use of hydroelectric cooling solutions while managing water resources reduces recurring expenses — critical given thin margins linked to energy consumption.[S1]

- Hosting Revenue Stream: Monetizing unused electricity supply via hosting third-party equipment diversifies income sources beyond direct bitcoin mining yields.[S10]

- Capital Raising Flexibility: Recent registered direct offering raising ~$2.1 million facilitates working capital; prior $3M loan secured asset-backed financing for expansion without diluting equity significantly.[S3,S22]

- Bitcoin Holdings Strategy: Building cryptocurrency reserves aligns revenue recognition strategy with bullish longer-term market outlook potentially amplifying returns if prices appreciate.[S1]

- Technology Adoption: Timely upgrading hardware fleet with efficient rigs like Antminer T21 enhances competitiveness amid rising network difficulty.[S21]

Risks / Watchpoints / Growth Constraints

- Bitcoin Halving Events: Scheduled supply halving reduces block rewards every ~four years imposing structural pressure on profitability unless offset by lower cost inputs or rising bitcoin prices.[S28]

- Market Volatility: Cryptocurrency price swings can affect realized margins materially; inventory held is subject to market risk.

- Energy Price Exposure: Although currently benefiting from low-cost power (<$0.04/kWh), fluctuating electricity markets or policy regulations could increase operating costs unexpectedly.

- Technological Obsolescence: Rapid innovation requires consistent capital reinvestment; failure or delay risks falling behind competitors with superior hash efficiency.

- Financial Leverage: Increased debt service costs post $3 million loan repayment obligation at high interest rate (12%) impact net earnings sensitivity.[F1,S14]

- Cybersecurity: Exposure to hacking or adverse software events threatens digital asset security underpinning business value.[S16]

- Liquidity Constraints: Current balance sheet liquidity is tight (cash & equivalents $83K vs current liabilities $2.76 million yielding current ratio around.33) highlighting reliance on refinancing or capital raises [F1].

What To Watch Next

Stakeholders should monitor:

- Hash rate trajectory post recent additions of new Antminer T21 units deployed fully at Duff site as per April 2026 update [S17].

- Changes in overall bitcoin production volumes relative to evolving blockchain network difficulty metrics.

- Quarterly financial performance focusing on operating margin resilience amid energy cost trends.

- Updates on hosting arrangement contracts extension or expansion that influence ancillary revenues.

- Management commentary regarding BTC holding strategy adjustments balancing market conditions vs cash requirements.

- Capital structure initiatives including any new equity issuance or debt refinancing events impacting liquidity profile.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $83837 | |

| 2025-12-31 | ||

| Total debt | $375000 | |

| 2025-12-31 | ||

| Net debt | $291163 | |

| 2025-12-31 | ||

| Current assets | $900684 | |

| 2025-12-31 | ||

| Current liabilities | $3mm | |

| 2025-12-31 | ||

| Current ratio | 0.33x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period End |

|---|---|---|

| Revenue | $9.13 M | |

| FY Dec '25 | ||

| Operating Income | $3.68 M | |

| FY Dec '25 | ||

| Net Income | -$2.87 M | |

| FY Dec '25 | ||

| Cash & Equivalents | $83.8 K | Dec '25 |

| Total Debt | $375 K | Dec '25 |

| Current Ratio | 0.33 | Dec '25 |

Abits’ most recent year-end financials reflect moderate revenue growth fueled largely by new capacity deployments but show a net loss position influenced by elevated depreciation charges and financing costs associated with its loan-financed expansion effort ([F1],[S14]). The company maintains modest liquidity positions relative to liabilities underscoring importance of continued capital access for ongoing operations ([F1]).

This analysis is based solely on publicly available regulatory filings without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments