TEVA Pharmaceutical Advances Neuroscience Pipeline and Navigates Market Challenges in Q1 2026

Teva leverages its acquisition of Emalex Biosciences to bolster its neuroscience pipeline while managing generics market pressures and sustainability-linked debt risks in Q1.

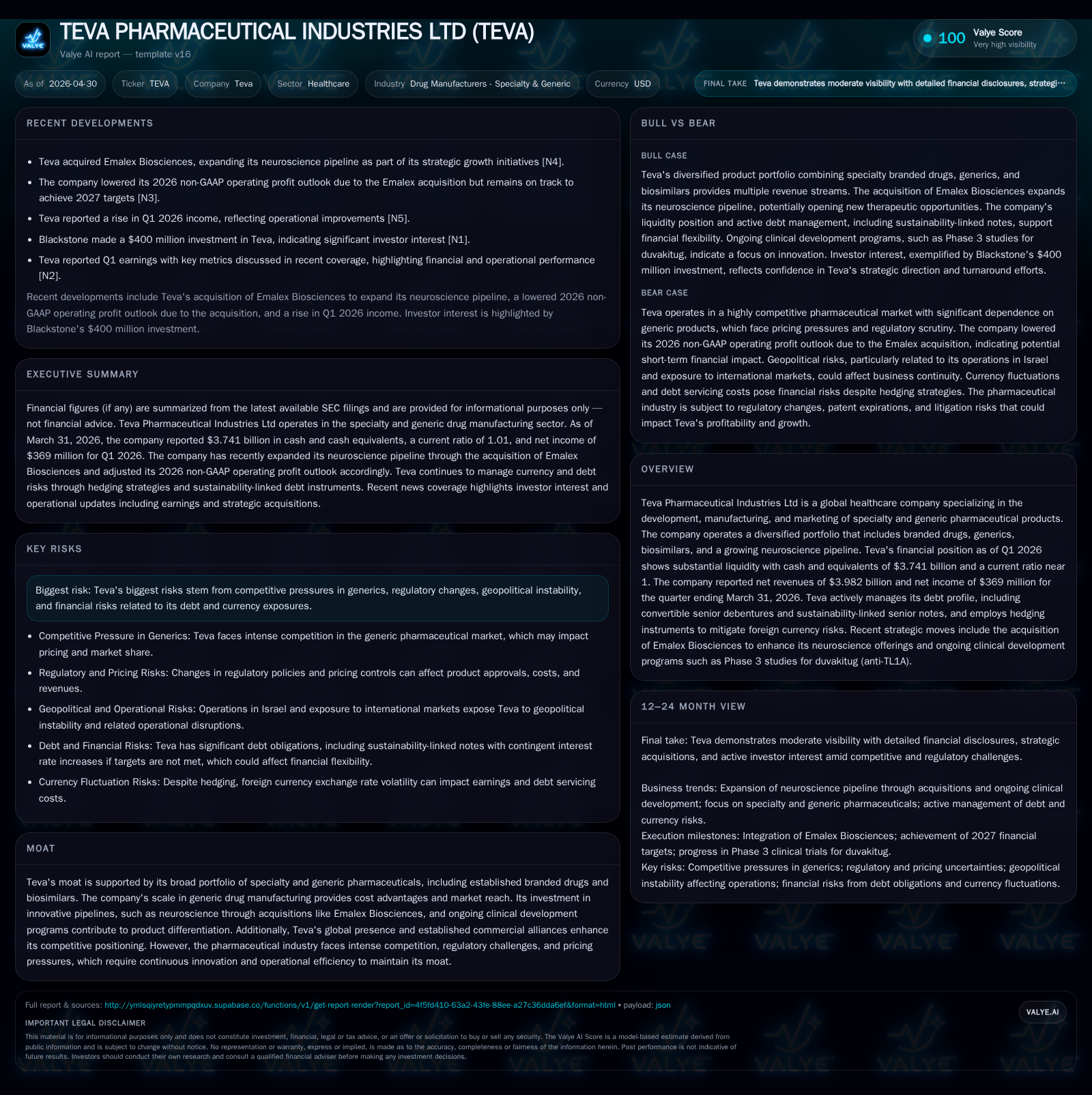

In Q1 2026, Teva Pharmaceutical Industries Ltd demonstrated proactive strategic refinement by integrating Emalex Biosciences to expand its pipeline into neuroscience therapeutics, notably advancing Phase 3 trials of duvakitug. Despite generics market headwinds marked by pricing pressure and regulatory delays, Teva secured operational resilience through disciplined debt repayment and liquidity preservation. The company’s sustainability-linked senior notes introduce variable interest costs contingent on performance targets post-May 2026, underscoring a nuanced financial risk profile. Teva’s robust cash position and global commercial alliances support its diversified pharmaceutical footprint and growth ambitions.

Q1 2026 Operating Update: Strategic Moves and Market Realities

Teva Pharmaceutical Industries Ltd reported net revenues of $3.982 billion with a net income of $369 million for the quarter ended March 31, 2026 [S2][S3][F1]. A crucial financial development was the February repayment of $23 million on its 0.25% convertible senior debentures at maturity. These debentures carry embedded clauses linking interest rates and potential premium payments to sustainability performance targets effective May 9, 2026 [S2]. Failure to meet these benchmarks can trigger a step-up in interest expenses between 0.125%–0.375% per annum, adding a nuanced layer of financial risk for Teva.

The quarter also highlighted operational challenges common in the generic pharmaceuticals sector: delayed launches of new generic products driven primarily by intensified competition and evolving regulatory policies [S2]. Teva's dependence on generics exposes it to both pricing pressure from competitors and shifts in reimbursement dynamics due to healthcare reforms like the U.S. One Big Beautiful Bill Act (OBBBA), which may reduce Medicaid insured populations and alter utilization patterns among payors [S22]. Such factors create headwinds for top-line momentum despite underlying demand.

Simultaneously, Teva is actively investing in specialty innovation through the acquisition of Emalex Biosciences, announced during Q1 2026, designed to deepen its neuroscience pipeline [N6]. This strategic repositioning reflects an effort to capture longer-term value through differentiated products beyond the commoditized generics market.

TEVA’s Business Model and Product Portfolio Quality

Teva operates a diversified pharmaceutical business model generating revenues from branded specialty drugs, high-volume generics, biosimilars, licensing arrangements, and milestone payments arising from developmental collaborations [S1]. Generics historically have represented a significant portion of revenue due to Teva's scale in manufacturing efficiency and broad geographic reach [S1], but these products face durable structural pressures including narrower price bands set by payors.

The company's licensing income notably includes milestone receipts linked to its innovative therapies pipeline. For example, development milestone payments tied to duvakitug’s Phase 3 study initiation contributed substantially to recent revenue recognition [S1]. The Emalex Biosciences acquisition is a deliberate step toward bolstering this specialty pipeline targeting the central nervous system (CNS), reinforcing a portfolio mix shift that could improve overall product differentiation over time.

Teva's expansive manufacturing scale delivers cost advantages important in generics production but also necessitates continual investment in quality control amidst rigorous regulatory oversight [S2]. Its commercial operations include key alliances with wholesalers, hospitals, pharmacies, and buying groups concentrated across major regions — relationships that underpin distribution but also concentrate negotiation leverage among customers.

Positioning Within the Specialty and Generic Pharmaceutical Industry

The pharmaceutical industry within which Teva competes features intense rivalry especially among generic manufacturers where price competition drives margins thin [S2]. Regulatory frameworks have tightened globally with heightened requirements for product approvals, inspections, and pharmacovigilance contributing to delayed launches or occasional recalls that disrupt growth cadence [S22].

Teva benefits from a moat supported by its breadth across branded drugs, biosimilars, established generics markets, plus an expanding neuroscience R&D effort post-Emalex [F1]. Nonetheless, incumbents face persistent risks from consolidation among distributors and payer entities which intensify pricing pressures.

Innovation-driven specialty pharmaceuticals offer higher barriers to entry relative to commoditized generics; thus Teva's Pivot to Growth strategy focuses on expanding this roster alongside sustaining core generic franchises efficiently [S2]. Regulatory uncertainty remains a critical competitive challenge — for example U.S. Executive Orders targeting prescription drug prices have implications for revenue trajectories that require strategic adaptation.

Growth Drivers: Neuroscience Expansion and Portfolio Diversification

The centerpiece of Teva’s near-term growth agenda is accelerated development within neuroscience therapeutics brought forward through Emalex acquisition [N6], complemented by clinical trial progress on duvakitug (anti-TL1A), now entering Phase 3 studies—a critical commercial inflection point that drives milestone payments and long-term product launch potential [S1][N12].

Simultaneously, biosimilars sales are rising as a partial hedge against generics cyclicality given their growing adoption due to patent expirations on biological drugs. Operational improvements targeting supply chain efficiencies aid margin enhancement amidst pricing challenges in core generics markets [S2].

Licensing deals producing upfronts and milestones provide non-linear revenue spikes supporting R&D funding flexibility [S1]. Collectively these elements define measurable KPIs including trial enrollments, regulatory submissions timelines, biosimilar market penetration rates, new product launch dates, and achieved cost savings — all determinative for trajectory assessment.

Risks and Constraints: Competitive Pressures, Regulatory Environment, and Debt Considerations

Competitive intensity remains highest within generics where price erosion is perennial while customer concentration among wholesalers amplifies bargaining power against manufacturers like Teva [S2]. Regulatory risks include potential delays or denials impacting launch windows primarily due to complex compliance demands or quality deviations resulting in recalls or facility suspensions [S22].

Legal proceedings associated with opioid litigation impose reputational risk alongside possible financial contingencies that remain unresolved [S22]. Additionally, the firm’s sustainability-linked senior notes carry conditional interest rate step-ups if environmental or social performance goals are not met starting May 2026, which could increase debt servicing costs [S2].

Geopolitical uncertainties extend across global operations introducing supply chain disruptions or market access challenges especially in volatile regions impacting international revenue streams [S2]. These multifaceted constraints require continued operational discipline with strategic innovation focus essential for sustained moat defense.

Upcoming Catalysts and Indicators to Monitor

Key upcoming milestones include announcements regarding progress or completion of duvakitug Phase 3 clinical trials expected within the next 12-18 months driving potential licensing income bumps [N12]. Monitoring regulatory approvals especially in neurosciences will indicate commercialization readiness enabling shift away from purely generic reliance.

The achievement or shortfall against sustainability targets scheduled for assessment around May-September 2026 should be closely watched given implication for interest rate resets on linked senior notes influencing financial expense line items [S2].

Additional indicators are timely resolution of generic product launch delays alongside updates on reform-induced impacts such as Medicaid insured population shifts under OBBBA policy framework affecting sales volumes.

Quarterly earnings cadence will continue serving as a barometer for execution effectiveness within both legacy generic platforms and innovation pipeline commercialization phases through concrete revenue/margin movements.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3.7bn | |

| 2026-03-31 | ||

| Current assets | $13.7bn | |

| 2026-03-31 | ||

| Current liabilities | $13.5bn | |

| 2026-03-31 | ||

| Current ratio | 1.01x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value |

|---|---|

| Cash & Equivalents | $3.741 billion |

| Net Revenues (Q1) | $3.982 billion |

| Net Income (Q1) | $369 million |

| Current Ratio | 1.01 |

Teva closed Q1 with strong liquidity positioning ($3.741 billion cash) nearly matching current liabilities reflected in a current ratio slightly above one — signifying credible near-term solvency despite operating complexities [F1][S2]. Net income improved relative to prior periods underscoring operational adjustments balancing out cost inflationary pressures. The company repaid $23 million of convertible senior debentures at maturity in February 2026 and continues to monitor sustainability-linked financing instruments that may affect future interest costs depending on performance outcomes [S2].

This analysis incorporates the latest public filings from Teva Pharmaceutical Industries Ltd up through April 29, 2026 (10-Q) alongside relevant SEC event reporting (8-K), corroborated by contemporaneous third-party news evaluations. It is intended solely as an informational review without constituting investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments