Nano-X Imaging’s Strategic Push and Pay-Per-Scan Innovation in Medical Imaging

Nano-X reported operational progress in Q1 2026 emphasizing commercialization and regulatory advances, underpinning its pay-per-scan model and global expansion in the digital tomosynthesis space.

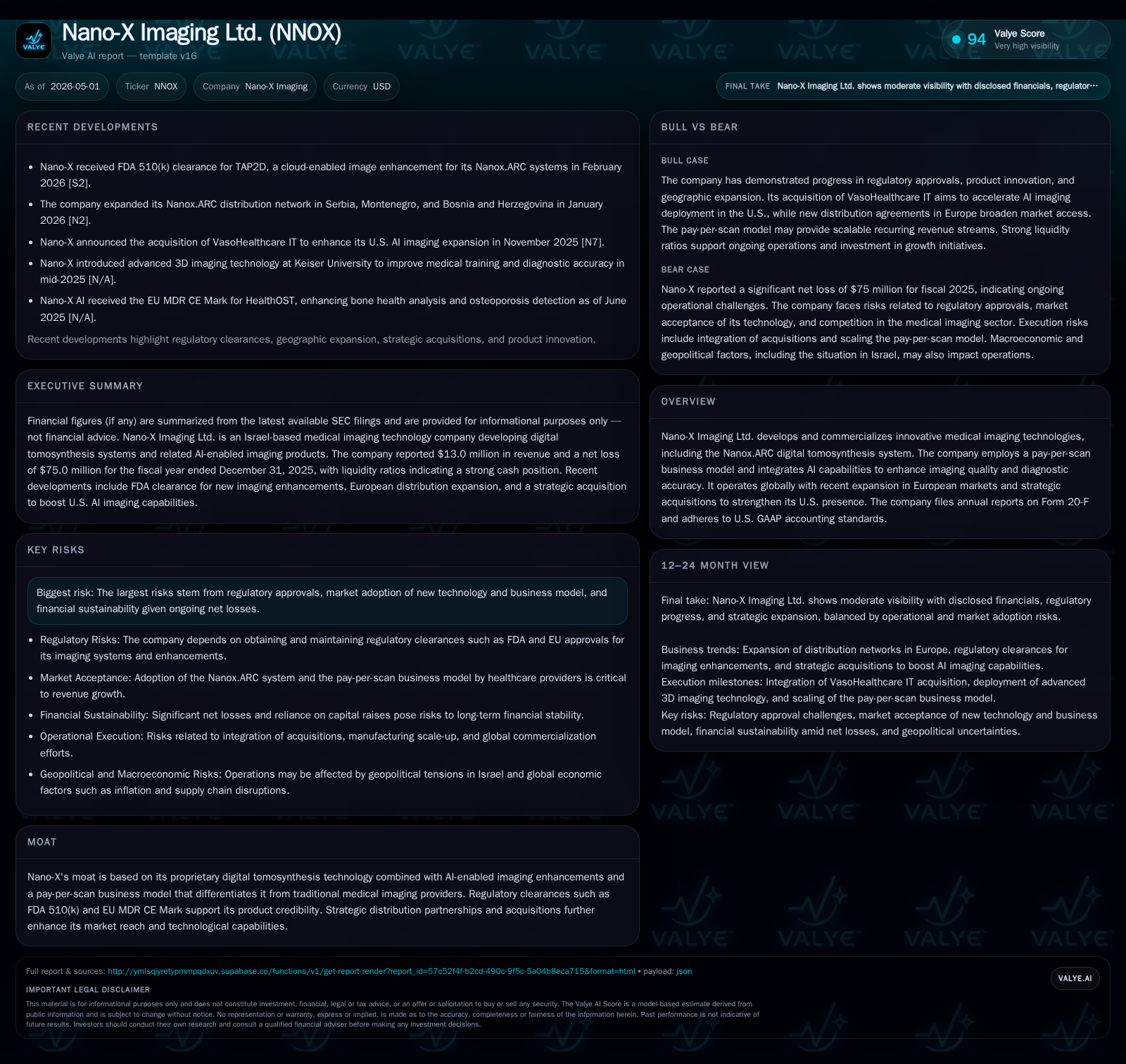

In its latest quarterly update, Nano-X Imaging disclosed continued momentum behind the commercialization of its Nanox.ARC digital tomosynthesis system supported by regulatory clearances and manufacturing partnerships. The company’s business model leverages a differentiated pay-per-scan revenue approach combined with AI-enhanced imaging to disrupt traditional medical imaging economics. Strategic acquisitions have broadened its technology capabilities and U.S. market access while geographic expansion into Europe complements growth prospects. However, regulatory hurdles, adoption of new technology and business model, and sustained net losses remain key risks to execution. Financially, Nano-X maintains a solid liquidity position ahead of scaling operations.

April 2026 Quarterly Update: Operational Highlights and Market Implications

Nano-X Imaging’s most recent quarterly disclosure filed on April 20, 2026 ([S2]) centers on continued operational developments pivotal to advancing commercial scale adoption of its Nanox.ARC system. While not divulging granular scan volumes or exact revenue updates beyond annual figures, the filing includes an attached press release reflecting current corporate narratives focused on commercialization progress within existing geographies. The document reiterates adherence to U.S. GAAP reporting standards while also providing certain non-GAAP metrics excluding specific expenses to frame performance in investor communications.

This update confirms the company's ongoing commitment to scale production via supply chain partnerships and enhance its offering through AI-enabled features cleared by regulators earlier this year. These near-term operating touches anchor Nano-X’s path toward broadening its user base in competitive medical imaging markets.

Innovating Medical Imaging: Nano-X’s Technology and Monetization Model

At the core of Nano-X’s strategy is the Nanox.ARC digital tomosynthesis system, which uniquely merges semiconductor-based X-ray source technology with advanced AI-powered imaging diagnostics ([S1]). This patented technology differentiates from conventional computed tomography by offering a cost-effective alternative designed to increase accessibility of medical imaging globally.

Nano-X employs a pay-per-scan revenue model whereby healthcare providers pay based on actual scan usage instead of large upfront equipment costs typical across the industry. This aligns revenue growth strongly with scan volume expansion rather than device shipments alone, creating recurring revenue streams linked directly to healthcare workflow utilization.

AI integration elevates image quality through proprietary enhancements like TAP2D, which received FDA 510(k) clearance in early 2026 ([S9]), enabling cloud-enabled augmentation that improves diagnostic confidence. Regulatory support extends internationally with CE marking under EU MDR standards, facilitating entry into key European markets where Nano-X has recently expanded operations ([S1]). This combination of technology innovation plus flexible monetization positions Nano-X distinctly amid legacy medical imaging vendors.

Competitive Position: Industry Structure, Regulatory Clearances, and Distribution Strategy

The medical imaging landscape remains highly competitive yet fragmented by entrenched analog technologies such as full-scale CT scanners costing significantly more than Nanox’s compact digital tomosynthesis units. Regulatory clearances like FDA 510(k) for new software components affirm product safety/effectiveness benchmarks crucial for hospital procurement decisions ([S1], [S9]).

Strategic manufacturing agreements with SKAN-X Radiology Devices (CEI), which produces X-ray tubes using Company-supplied semiconductor chips since late 2024 ([S1]), secure critical supply chain control over components essential for device performance consistency and cost efficiencies. Additionally, Fabrinet's contract manufacturing services commenced in mid-2025 include assembly, testing, shipping logistics, and consigned inventory management under a volume supply agreement ([S1]). These partnerships reduce traditional barriers tied to scaling production capacity without extensive capital expenditure.

Acquisitions such as USARAD have deepened Nano-X’s service value chain by incorporating radiology service segments into their platform allowing bundled offerings combining imaging hardware/software with interpretation services - enhancing stickiness with healthcare customers in the U.S. market ([S1]). Similarly, Nanox AI acquisition adds intellectual property assets focused on software-driven clinical decision support tools.

These moves collectively strengthen distribution reach across multiple regions while reinforcing differentiation via integrated solutions rather than standalone hardware sales.

Manifesting Growth: Geographic Expansion, Strategic Acquisitions, and AI Enhancements

Nano-X signals growth driven by expanding into European territories leveraging CE mark registrations coupled with targeted sales efforts focusing on hospitals seeking cost-efficient alternatives to legacy modalities (, [S1]). The ability to facilitate increased scan volume under the pay-per-use framework allows scaling revenues as installed base penetration rises without direct proportional increases in fixed manufacturing costs.

Recent acquisitions contribute strategic muscle by supplementing core imaging products with complementary service lines; USARAD expands radiology coverage while Nanox AI accelerates software roadmap including data analytics and automated reporting capabilities that could unlock incremental pricing or expandable use cases beyond traditional imaging workflows.

AI enhancements like TAP2D provide competitive differentiation that can extend product lifecycle value through continuous feature upgrades delivered via cloud platforms—a rising trend among medical device innovators aiming for subscription-like revenue extensions.

Operational KPIs implied from filings emphasize monitoring installed systems count alongside scans performed as key demand markers controlling top-line momentum as commercialization scales regionally.

Risks and Constraints: Regulatory, Market Adoption, and Financial Sustainability Challenges

Despite technological promise, Nano-X faces notable hurdles detailed primarily in its annual filing ([S1]) including uncertainties around timing Windows for securing comprehensive regulatory approvals across diverse jurisdictions potentially delaying market penetration pace. Regulatory scrutiny may intensify given the novel nature of some components (e.g., AI-powered enhancements), necessitating robust validation data supporting clinical efficacy claims.

Furthermore, customer adoption risk looms given disruption inherent in shifting from outright capital equipment purchase towards a usage-based pay-per-scan model – buyers may exhibit cautious procurement behavior pending firsthand evidence of ROI or sufficient reimbursement frameworks aligning incentives.

Ongoing losses (operating income -$78M; net income -$75M for 2025 [F1]) underscore financial sustainability challenges requiring prudent cash management despite ample liquidity buffers presently available.

Goodwill associated with acquisitions requires periodic impairment assessments sensitive to forecast revisions or discount rate changes reflecting business uncertainty ([S1]). Competitive risk remains acute as entrenched industry incumbents develop or acquire emerging tech capabilities potentially eroding Nano-X's early-mover advantage.

In sum, these risks form critical watch points balancing optimism over innovation-led disruption against execution complexities inherent within regulated healthcare markets.

Forward Look: Milestones, Execution Markers, and Demand Signals in 2026

Moving forward through 2026, key milestones include ongoing regulatory submissions supporting incremental product launches or geographic authorizations especially within Europe where further clarity on reimbursement policies will influence uptake ([S2], [S3]). Enhancement of manufacturing throughput through Fabrinet’s facilities is another pivotal operational execution point necessary to meet anticipated demand growth sans bottlenecks.

Successful integration outcomes from USARAD & Nanox AI acquisitions offer relevant checkpoints measuring synergy realization mostly around combined go-to-market effectiveness plus cross-selling opportunities.

Management commentary across recent SEC filings emphasizes tracking quarterly increases in scans processed as leading indicators foreshadowing revenue acceleration aligned to their pay-per-scan model expansion ([S2]). Pricing evolution trends also warrant scrutiny as increasing sophistication around AI features might enable pricing premium capture perpendicular to volume gains.

Monitoring these unfolding developments will illuminate whether Nano-X can solidify competitive footholds amidst intensifying industry dynamics while progressing toward scaled profitability horizons.

Financial Snapshot: Liquidity, Capital Structure, and Profitability Considerations

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $49mm | |

| 2025-12-31 | ||

| Current assets | $67mm | |

| 2025-12-31 | ||

| Current liabilities | $17mm | |

| 2025-12-31 | ||

| Current ratio | 3.96x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

As of December 31, 2025 per latest audited data ([F1]), Nano-X holds $49.15 million in cash & equivalents against modest total debt near $3.8 million (albeit dated September 2021), yielding a healthy current ratio close to 3.96 reflective of short-term liquidity robustness relative to liabilities totaling roughly $16.9 million at year-end.

On profitability metrics defined by full-year 2025 results: revenues totaled approximately $13 million whereas operating losses approached $78 million culminating in net loss close to $75 million illustrating significant operational investment phases amid early commercialization cycles.

Negative net debt position (~$45 million excess cash over debt) according to available balance sheet data supports a reasonable runway though sustained losses highlight elevated funding needs requiring either external capital raises or material operating improvements to sustain tech development alongside marketing expansion initiatives.

| Metric | Value (USD) | Date |

|---|---|---|

| Cash & Equivalents | 49,151,000 | |

| 2025-12-31 | ||

| Total Debt | 3,800,000 | |

| 2021-09-30 | ||

| Current Ratio | 3.96 | |

| 2025-12-31 | ||

| Net Income | -75,018,000 | |

| 2025-12-31 |

This financial position contextualizes Nano-X’s need to balance growth investments with prudent cash consumption strategies amid longer-term vision for scalable profitable operations.

This analysis is based solely on publicly available SEC filings and Companyfacts data [F1] as of April–May 2026 without providing any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments