Grown Rogue International's Vertical Integration Reinforces Market Position as New Jersey Unit Marks Milestone

The company highlights its New Jersey affiliate's first-year sales, underscoring vertical integration benefits and strategic consolidation in evolving cannabis markets.

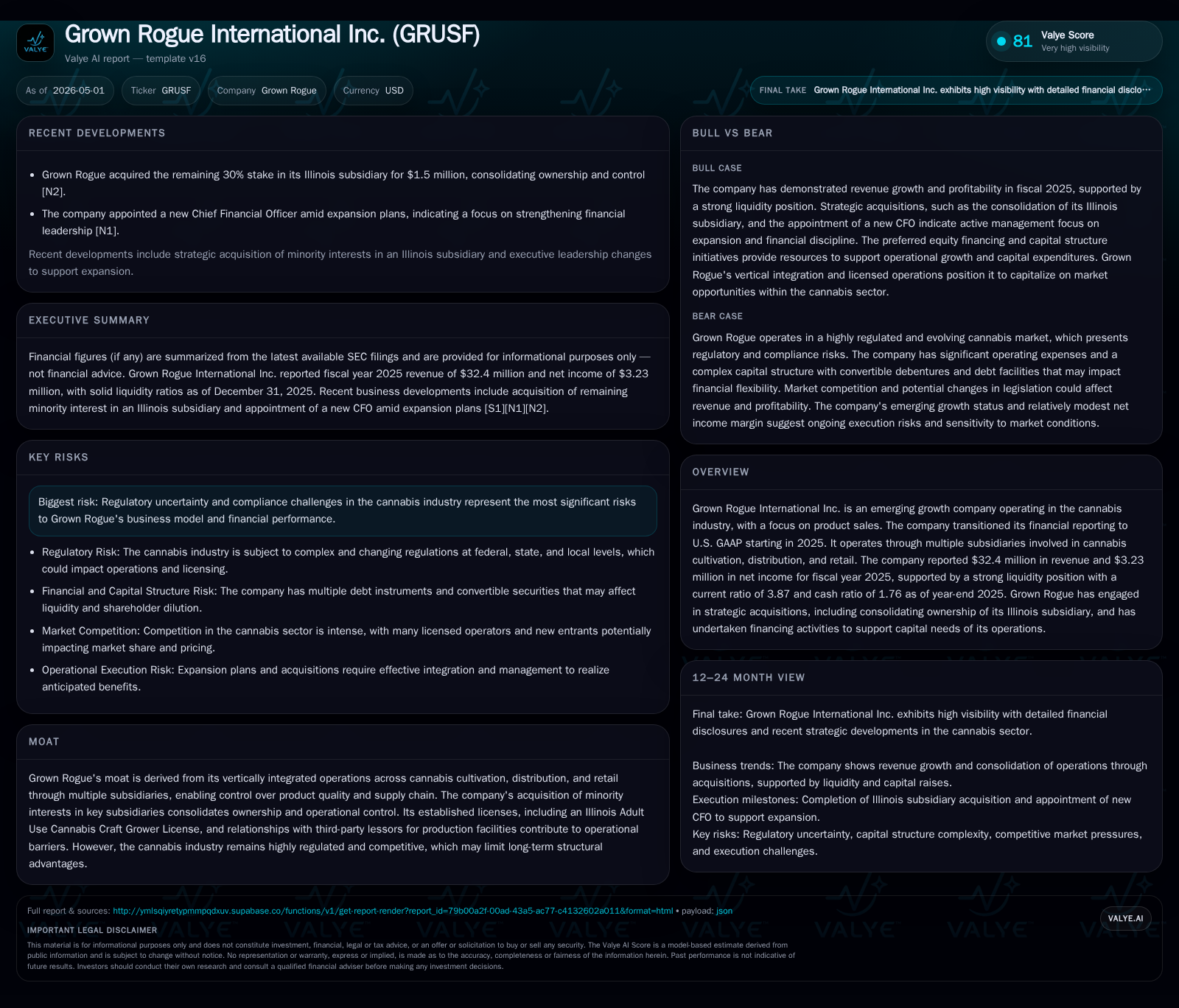

Grown Rogue International recently celebrated the one-year sales anniversary of its New Jersey affiliate, a tangible marker of progress within its vertically integrated cannabis operations. The latest quarterly update reveals ongoing strategic consolidation, particularly in Illinois through acquisition of minority interests, while reinforcing liquidity strength supportive of growth. Positioned within a highly regulated and fragmented industry, the company leverages its control across cultivation, distribution, and retail to maintain supply reliability and product quality amid competitive pressures.

Recent Operating Developments and Their Significance

Grown Rogue International Inc.'s December 15, 2025 Form 6-K marked a notable milestone: its New Jersey affiliate celebrating one full year of active sales operations [S2]. This achievement signals tangible operational progress within a strategically important state where legal cannabis markets are still evolving. Such milestones provide critical validation of customer adoption and supply chain stabilization in newly penetrated regions.

Following this, on April 27, 2026, Grown Rogue announced it will release financial results for Q1 2026 on May 12 along with an earnings webcast [S3]. Situated soon after the holiday quarter close, this update is expected to reveal early impacts from recent acquisitions and capital deployments supporting expansion initiatives. These near-term events collectively illustrate incremental traction across regional operations within the company’s vertically integrated model.

Business Model: Vertical Integration Across Cultivation, Distribution, and Retail

Grown Rogue’s business model is anchored in controlling the value chain across cannabis cultivation, distribution logistics, and retail sales through a network of subsidiaries operating under distinct licenses [S1]. The vertical integration not only enables consistent product quality oversight but also limits dependency on third-party growers or distributors—a competitive advantage given regulatory constraints on supply chains.

A pivotal asset in this model is Sea Craft LLC, an Illinois-based craft grower holding an Adult Use Cannabis Craft Grower License. In March 2026, Grown Rogue's majority-owned subsidiary GRMA moved to acquire the remaining 49% minority stake from other members pending regulatory approval [S17]. This consolidation enhances operational control over cultivation capacity licensing benefits under Illinois law — particularly important given tight state-imposed production caps.

Controlling cultivation assets supports reliable wholesale supply to Grown Rogue’s retail networks spread across multiple states including New Jersey and Oregon. Additionally, leasing arrangements with third-party landlords for facility production provide flexibility for scaling up without full capital burdens of property ownership [S1].

Competitive Positioning in a Regulated, Fragmented Cannabis Market

Within the highly regulated U.S. cannabis industry landscape, Grown Rogue competes among numerous regional operators balancing state-level rules and market fragmentation. The regulatory environment creates entry barriers shaped by limited state licenses, compliance requirements, and restrictions on retail storefront density.

Particularly relevant is the company's foothold via licenses such as the Illinois Adult Use Craft Grower permit—an officially capped license type restricting total output but offering premium product positioning due to craft categorization. Leveraging relationships with lessors for production sites grants some operational leverage versus owning costly real estate outright.

However, persistent regulatory uncertainty remains both a moat and risk: while it limits new entrants and consolidates existing players’ positions, it also means long-term structural advantages are fluid subject to government policy changes or shifting compliance costs [S1]. Price competition persists especially at retail level given oversupply risks in mature markets.

Growth Catalysts: Expansion of Regional Operations and Strategic Acquisitions

Key growth drivers include geographic expansion efforts evidenced by New Jersey’s affiliate one-year mark—indicating sustained local market establishment—and recent minority interest buyout for full ownership of Sea Craft within Illinois [S2][S17]. Such moves increase not only scale but simplify governance structures historically encumbered by joint ventures or minority partnerships.

In March 2026, Grown Rogue secured $3 million in preferred equity financing through issuing preferred units convertible into common stock or subordinate voting shares over a three-year horizon—highlighting active capital raising aimed at funding capital expenditures tied to production capacity expansions [S7]. This monetary inflow complements existing cash holdings (~$10 million) underpinning near-term capex plans.

The appointment of a new CFO announced in April underscores an organizational push toward disciplined financial strategy as management navigates both organic growth opportunities and potential bolt-on acquisitions noted in corporate updates [N1]. These steps align with scaling ambitions requiring careful liquidity management amid sector volatility.

Risks and Constraints: Regulatory Challenges and Industry Competition

Despite operational achievements, regulatory risk forms the preeminent constraint impacting Grown Rogue’s trajectory. The cannabis space continues grappling with policy shifts including possible license revocations or alterations in taxation frameworks that carry immediate cost implications. Compliance overheads arising from multi-state operations also add complexity regularly affecting margins.

Competition remains intense at both wholesale and retail levels due to abundant supply options in certain states coupled with pricing pressures eroding upward margin potential. License quantity limitations provide some barrier but are balanced by rising illegal market activity in some jurisdictions challenging legal players’ volumes.

Consequently, monitoring political environments that influence cannabis legalization trends is crucial since legislative reversals or delays could quickly impact asset utilization or planned investments [S1].

Key Near-Term Milestones and Investor Watchpoints

Investors should track Grown Rogue's Q1 2026 earnings release scheduled for May 12 alongside earnings call participation—a timely snapshot reflecting immediate outcomes from recent acquisitions such as Illinois minority interest consolidation as well as capital deployment effects from preferred equity financing [S3][S6].

Additional focus points include any announcements relating to licensing advancements or new state market entries which remain pivotal for expanding revenue base. Furthermore, refinancing developments or additional investment activities communicated by management offer insights about strategic priorities addressing competitive dynamics and ensuring growth capital availability.

Latest Financial Snapshot Supporting Growth Ambitions

As of December 31, 2025 ([F1]), Grown Rogue reported revenues exceeding $32 million supported by net income above $3.2 million despite operating losses driven by reinvestment phases. Cash reserves surpassing $10 million underpin flexible funding options while total debt near $12.6 million results in modest net debt (~$2.5 million), reflecting manageable leverage conditions useful for securing additional capital or absorbing unforeseen expenses without deleterious strain on fiscal stability.

Such financial positioning provides a foundation for measured risk-taking consistent with vertical integration strategies requiring upfront investments in cultivation infrastructure and facility lease commitments.

This analysis focuses on operational dynamics grounded strictly in recent SEC filings combined with company disclosures through early calendar year 2026 events. It refrains from projecting future performance outside stated guidance or non-public information. Readers should consider ongoing regulatory developments when evaluating industry prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments