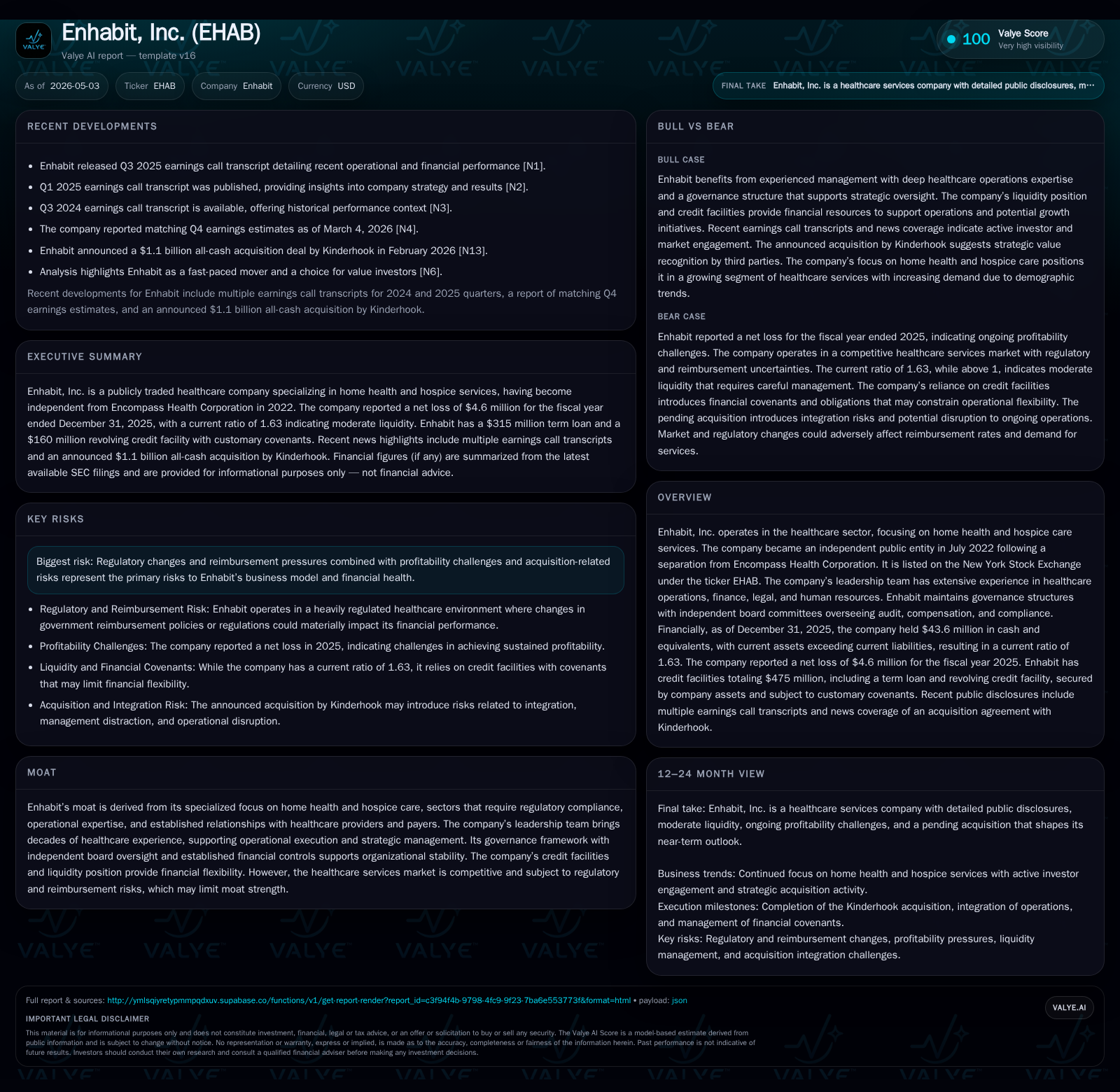

Enhabit’s Merger Moves and Home Healthcare Growth Trajectory

Enhabit advances a pending merger amidst steady home health service demand and complex reimbursement dynamics.

Enhabit, Inc. reported stable operating conditions in its latest quarterly filing ahead of a merger slated to close in mid-2026. The company specializes in home health and hospice care, generating revenue primarily through Medicare and other insurance reimbursements, which impose regulatory complexity and pricing pressure. Its competitive position benefits from specialized capabilities and deep regulatory compliance experience but faces ongoing risks related to reimbursement changes and leveraged capital structure. Key near-term catalysts include shareholder approval of the $688 million acquisition by Kinderhook-backed Anchor Parent, with operational integration and financial performance in focus thereafter.

Latest Operating Update: Quarterly Performance and Acquisition Progress

Enhabit’s latest quarterly disclosure on November 5, 2025 ([S2]) reports no material changes to risk factors since FY 2024 but underscores ongoing operational stability ahead of a transformative corporate event. The company maintains a cash balance of $43.6 million and current assets totaling $205.6 million against current liabilities of $126.3 million, yielding a current ratio of 1.63—reflecting sound short-term liquidity [F1].

On February 22, 2026, Enhabit entered into a definitive merger agreement to be acquired by Anchor Parent, LLC (an affiliate of Kinderhook Industries) via Anchor Merger Sub Inc., with a transaction equity value supported by $688 million in equity commitments plus debt financing ([S3],[S7],[S8]). The Federal Trade Commission granted early termination of the Hart-Scott-Rodino waiting period by mid-April 2026 ([S8]), paving the way for a special stockholder meeting scheduled May 12, 2026 to approve the merger. Subject to customary closing conditions—including stockholder approval—the transaction is anticipated to close in Q2 2026.

This pending acquisition marks a pivotal strategic milestone for Enhabit amid a healthcare services industry increasingly focused on scale to counter regulatory pressures and enhance operational efficiency.

Business Model Breakdown: Home Health and Hospice Service Offerings

Enhabit operates exclusively within the home health and hospice segments of healthcare, having been spun out independently from Encompass Health Corporation in mid-2022 ([S1]). The company delivers skilled nursing care, therapy services (such as physical and occupational therapy), social support, and palliative care directly to patients’ homes or residential facilities.

Revenue generation predominantly derives from third-party payers: Medicare remains the largest single source due to the population aged over 65 requiring home-based care options; Medicaid and commercial insurance contribute additional streams ([S1]). These Medicare reimbursements are governed by complex regulations—including service eligibility criteria and payment rate schedules—which impose both operational burdens and limits on price setting.

The need for specialized clinical staff capable of meeting stringent certification requirements combined with compliance to federal reporting elevates switching costs for customers entrusting sensitive post-acute care needs ([S1]). Moreover, Enhabit’s executive leadership team includes veterans with substantial healthcare operations expertise who drive quality initiatives to maintain compliance while aiming for cost efficiency.

Competitive Positioning within Healthcare Services Sector

Within the fragmented landscape of home health providers—which ranges from national chains to regional players—Enhabit's competitive position centers on its focused scope coupled with governance structures that ensure audit rigor and compliance controls ([S1]). While regulatory oversight curbs pricing power inherently due to fixed reimbursement formulas under Medicare fee schedules or bundled payments frameworks, Enhabit leverages its operational excellence as a differentiation factor.

The company faces competition not only from large diversified healthcare services firms but also evolving entrants targeting telehealth-enabled or technology-driven post-acute care solutions. Despite competitive pressures, Enhabit's moat includes its specialized provider network relationships and payer contracts reinforced by careful management of regulatory risk ([S1],[F1]). However, the sizable debt load reflecting leveraged capital raise strategies constrains both investment capacity and margin resilience upon reimbursement volatility ([F1],[S4]).

Drivers of Growth: Market Demand, Regulatory Tailwinds, and Operational Leverage

Demand-side growth is structurally supported by demographic tailwinds: the aging U.S. population drives an expanding pool of patients medically appropriate for home health or hospice services ([S1]). The broader healthcare trend toward de-institutionalization favors cost-effective outpatient alternatives where Enhabit is well positioned.

Regulatory cues potentially augment growth via incentives encouraging home-based palliative care or reductions in skilled nursing facility utilization rates—areas where policy aims intersect with patient preference shifts. Mergers like the one pending at Enhabit often enable scale economies in back-office operations and improved purchasing power for clinical supplies or IT systems facilitating quality improvements while containing administrative overhead ([S1]).

Operational leverage gains may also emerge if post-merger integration successfully consolidates overlapping service footprints or streamlines patient referral networks between hospice and home health arms enhancing revenue per patient served.

Risk Factors and Potential Constraints on Expansion

Despite growth opportunities, major risks persist centered on external reimbursement environments prone to policy revision including CMS payment cuts or restructuring that could materially compress margins given Medicare’s dominance ([S2],[F1]). Regulatory complexities impose continuing compliance costs which if breached may lead to recoupment actions or penalties impacting financial outcomes.

Merger-related risks include uncertainty over final approvals notwithstanding FTC clearance—shareholder dissent or unforeseen conditions could delay closure. Post-merger integration poses execution challenges such as retention of clinical talent, culture alignment among combined entities, system harmonization costs—all affecting near-term performance benchmarks ([S7],[S8]).

Key Catalysts to Monitor: Milestones Around Merger Completion and Financial Targets

Critical upcoming milestones include the May 12th special stockholder meeting on merger approval ([S7],[S8]), after which closing is anticipated later in Q2 2026 if all conditions are met. Monitoring management announcements regarding integration plans or disclosed operating targets post-close will be essential to evaluate realization of synergistic benefits.

Further updates on reimbursement environment shifts by CMS or legislative developments impacting skilled nursing facility alternatives remain important demand markers potentially influencing financial outlooks.

Operational metrics such as patient volume growth rates in home health services or hospice admission trends could serve as early indicators of sustained market share gains post-merger.

Financial Snapshot: Liquidity, Debt Profile, and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $44mm | |

| 2025-12-31 | ||

| Total debt | $426mm | |

| 2025-12-31 | ||

| Net debt | $382mm | |

| 2025-12-31 | ||

| Current assets | $206mm | |

| 2025-12-31 | ||

| Current liabilities | $126mm | |

| 2025-12-31 | ||

| Current ratio | 1.63x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Liquidity at year-end remains adequate for current obligations; however strategic capital deployment will likely prioritize post-merger integration expenditures alongside prudent leverage management given covenant thresholds described in recent credit agreements ([S4],[F1]).

This analysis synthesizes Enhabit’s recent SEC filings through April–November 2025/26 combined with its corporate event trajectory shaping its position within the specialized home health services sector. Investor assessments might focus on execution risks surrounding completion of the Kinderhook-backed acquisition while appraising structural growth drivers linked to aging demographics amid evolving healthcare payment landscapes.

This report is informational only and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments