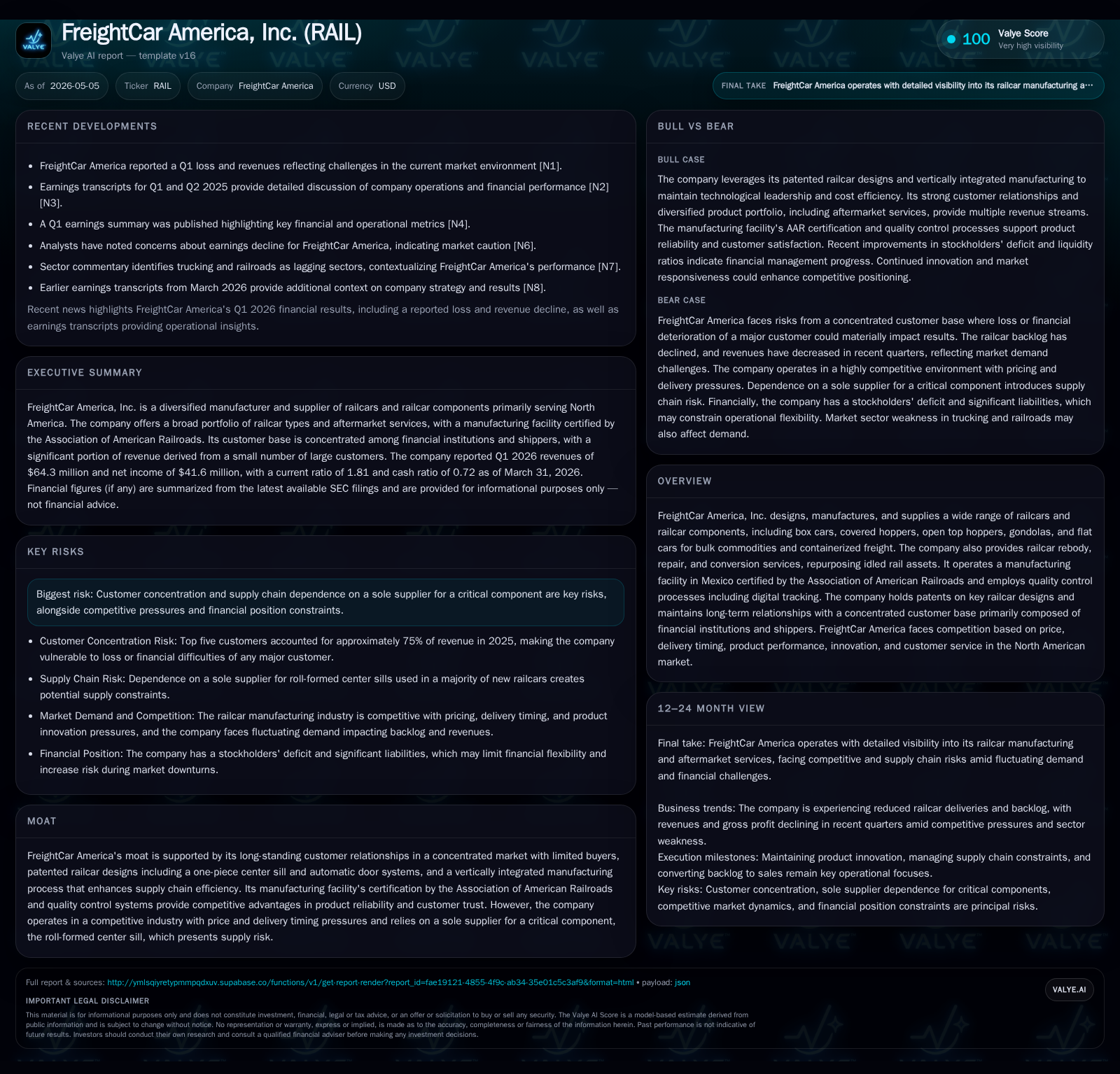

FreightCar America Shifts Focus with Carly Railcar Acquisition and Backlog Decline in Q1 2026

Latest quarterly results highlight backlog contraction amid strategic aftermarket expansion through acquisition.

In the first quarter of 2026, FreightCar America reported a contraction in its railcar backlog alongside a key acquisition aimed at bolstering its aftermarket distribution segment. The company's core business of designing and manufacturing specialized freight railcars remains anchored by patented products and long-standing customer relationships, though it faces cyclical demand patterns and supply chain risks. The newly acquired Carly Railcar Components will expand service offerings and parts supply capabilities, supporting growth beyond new railcar builds. The business operates in a competitive North American industry dominated by price sensitivity and delivery timing pressures, with concentrated buyers largely from financial institutions and shippers.

Recent Operating Update: Q1 2026 Filing Highlights

FreightCar America's most recent quarterly report dated May 4, 2026 [S2] underscores notable shifts in its operational landscape. The company's total railcar backlog contracted significantly from 2,797 units at the end of 2024 to approximately 1,926 units by the end of 2025, with an estimated sales value of $137 million. This reduction reflects typical cyclicality in railcar demand but points to softer near-term manufacturing volume.

Complementing this metric, FreightCar announced completion of the acquisition of Carly Railcar Components ("CRC") on December 19, 2025 [S2]. CRC operates as a wholly owned subsidiary now integrated into FreightCar's aftermarket distribution network. This strategic move aims to broaden FreightCar’s footprint beyond new railcar builds into higher-margin aftermarket replacement parts and services, a segment offering steadier revenue streams amid fluctuating new-build orders.

Additionally, inventory reserves related to excess or slow-moving parts held steady with $866K at March-end compared to $950K at December-end; this stability suggests relatively balanced procurement pacing despite backlog contraction [S2].

These developments signal FreightCar’s intent to partially offset cyclicality in manufacturing through aftermarket growth initiatives while navigating the current market softness.

Business Model: Integrated Railcar Manufacturing and Aftermarket Services

FreightCar America's core business consists of designing, manufacturing, and supplying a diverse mix of freight railcars including box cars, covered hoppers, open-top hoppers, gondolas, flat cars used primarily for bulk commodities transport within North America [S1]. Its product suite benefits from proprietary technology such as patented one-piece center sills and automatic door systems that underpin differentiation and longstanding customer trust.

The company's revenue mechanics are dual-pronged: substantial top-line proceeds derive from manufacturing new railcars sold primarily to financial institutions (78% revenue share in 2025) who finance lease portfolios for shippers; smaller but growing revenue flows stem from the aftermarket segment encompassing parts supply, rebodying, repair services, and safety inspections [S1].

Manufacturing operations occur via an AAR-certified plant in Mexico utilizing digital quality tracking called TruTrack™, which monitors production stages ensuring compliance with stringent standards. This vertical integration improves cost control and reliability—a critical buying factor given industry emphasis on durability and timely delivery [S1].

Pricing is influenced by raw material costs (notably steel and aluminum), contract terms including cancellation clauses with compensation provisions for order disruptions, plus project complexity dictating unit labor content. Contract backlogs function as key pipeline indicators for future revenue recognition.

Overall margins fluctuate with product mix between high-ticket new builds versus aftermarket parts/services. Aftermarket tends to yield better margin stability and cash conversion owing to recurring parts demand among incumbent customers.

Industry Structure and Competitive Position

The North American railcar market is oligopolistic with a handful of players supplying both freight cars and componentry. Buyers span financial investors who own fleets leased to shippers alongside direct purchases by railroads or commodity shippers themselves. Relative scarcity of buyers amplifies customer concentration risk; FreightCar’s top three customers alone contributed over half its revenue in recent years [S27].

Competition is intense on price given large contract sizes and frequent bidding processes but also heavily weighted on delivery timing flexibility since fleet replenishment impacts transport logistics critically. Product innovation involving weight reduction (e.g., aluminum-bodied cars), enhanced door automation systems, increased load capacity, durability improvements through patented technologies foster competitive moats but require ongoing R&D investments [S1].

FreightCar’s ability to maintain patents on critical designs such as the BethGon II coal car enhances defensibility yet reliance on a sole supplier for the roll-formed center sill limits supply chain diversity—posing risk if disruptions occur there.

Moreover, adherence to AAR certifications and robust quality assurance positions FreightCar favorably for securing contracts where reliability is non-negotiable.

Growth Drivers

Backlog Conversion

Backlog levels—currently at about 1,926 units—are pivotal growth markers translating future manufacturing volume when converted into firm deliveries. Contractual safeguards obligate customers to compensate for cancellations mitigating downside but delays in order progression reflect cyclical demand patterns impacted by broader economic conditions affecting commodities shipping volumes.

Aftermarket Expansion Through Acquisition

The CRC acquisition strategically boosts FreightCar’s presence in aftermarket components distribution—an area offering more predictable revenue streams insulated somewhat from capital spending cycles affecting new builds [S2]. Cross-selling opportunities for rebody services combined with parts sales create stickier customer relationships enhancing lifetime value.

Innovation Pipeline

Continued development of lighter-weight aluminum designs (e.g., BethGon II enhancements) improves payload efficiency appealing to cost-conscious shippers focused on operating economics. Emphasis on automatic door systems expands addressable markets especially where cargo security and unloading speed are valued.

Supply Chain Optimization

FreightCar’s vertically integrated manufacturing process supported by digital quality controls reduces delays and defect rates enabling faster customer deliveries—a distinct advantage given industry-wide pressure on lead times.

Risks / Watchpoints / Growth Constraints

- Customer Concentration: With top five customers accounting for roughly three-quarters of sales recently [S27], losing any major contract poses material earnings impact risks.

- Supply Chain Risk: Dependence on a sole supplier for critical roll-formed center sills creates vulnerability; disruptions could delay production significantly.

- Cyclicality: Demand for new freight cars ties closely to commodity transport activity which can fluctuate sharply with economic cycles impacting railroad capex budgets.

- Pricing Pressure: Competitors may erode margins through aggressive bids especially when delivery schedule premiums compress or raw material inputs spike.

- Regulatory Risks: Compliance with evolving safety standards or changes in trade tariffs affecting import/export costs could alter cost structures unexpectedly.

- Financial Covenants: The company holds a $115 million term loan maturing at end-2028 subject to leverage ratio tests beginning March 31, 2025; failure to meet these covenants would restrict operational flexibility [S2].

What to Watch Next

- Backlog Trends: Monitoring changes in firm order volumes will indicate recovery or further softening in demand.

- Aftermarket Revenue Growth: Integration success of Carly Railcar Components should manifest as incremental aftermarket sales gains.

- Raw Material Cost Trajectory: Fluctuations here affect margins directly; mitigation strategies or price pass-through mechanisms will be key execution points.

- Debt Covenant Compliance: Quarterly leverage testing results post-March 2025 period warrant close scrutiny given potential liquidity impacts.

- New Product Launches: Releases or patent extensions enhancing product competitiveness could sustain pricing power.

- Customer Concentration Dynamics: Any shifts in client composition or contract renewals with major customers could materially influence revenue visibility.

Financial Profile (Latest Snapshot)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $112mm | |

| 2025-12-31 | ||

| Net debt | $47mm | |

| 2025-12-31 | ||

| Current assets | $163mm | |

| 2026-03-31 | ||

| Current liabilities | $90mm | |

| 2026-03-31 | ||

| Current ratio | 1.81x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

The balance sheet exhibits moderate leverage with total debt net of deferred financing costs at approximately $101 million as of March 31, 2026 [S4], down marginally year-over-year. The company maintains compliance with covenants tied to its $115 million term loan maturing December 31, 2028 [S2]. Liquidity metrics reveal current assets at around $163 million against current liabilities near $90 million yielding a current ratio close to 1.81—indicating sufficient working capital coverage [F1],[S2].

Recent quarters show operating income fluctuating consistent with production volume swings but adjusted net income benefited from non-cash gains related to changes in warrant liability fair values [S23],[S20]. Cash flow generation faced headwinds due primarily to inventory increases aligned with backlog staging [S23].

This financial position supports ongoing operational initiatives including acquisitions like CRC while requiring vigilant cost management given margin sensitivities inherent in commodity-driven industries.

Disclaimer: This analysis is based solely on publicly available filings as cited without provision of investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments