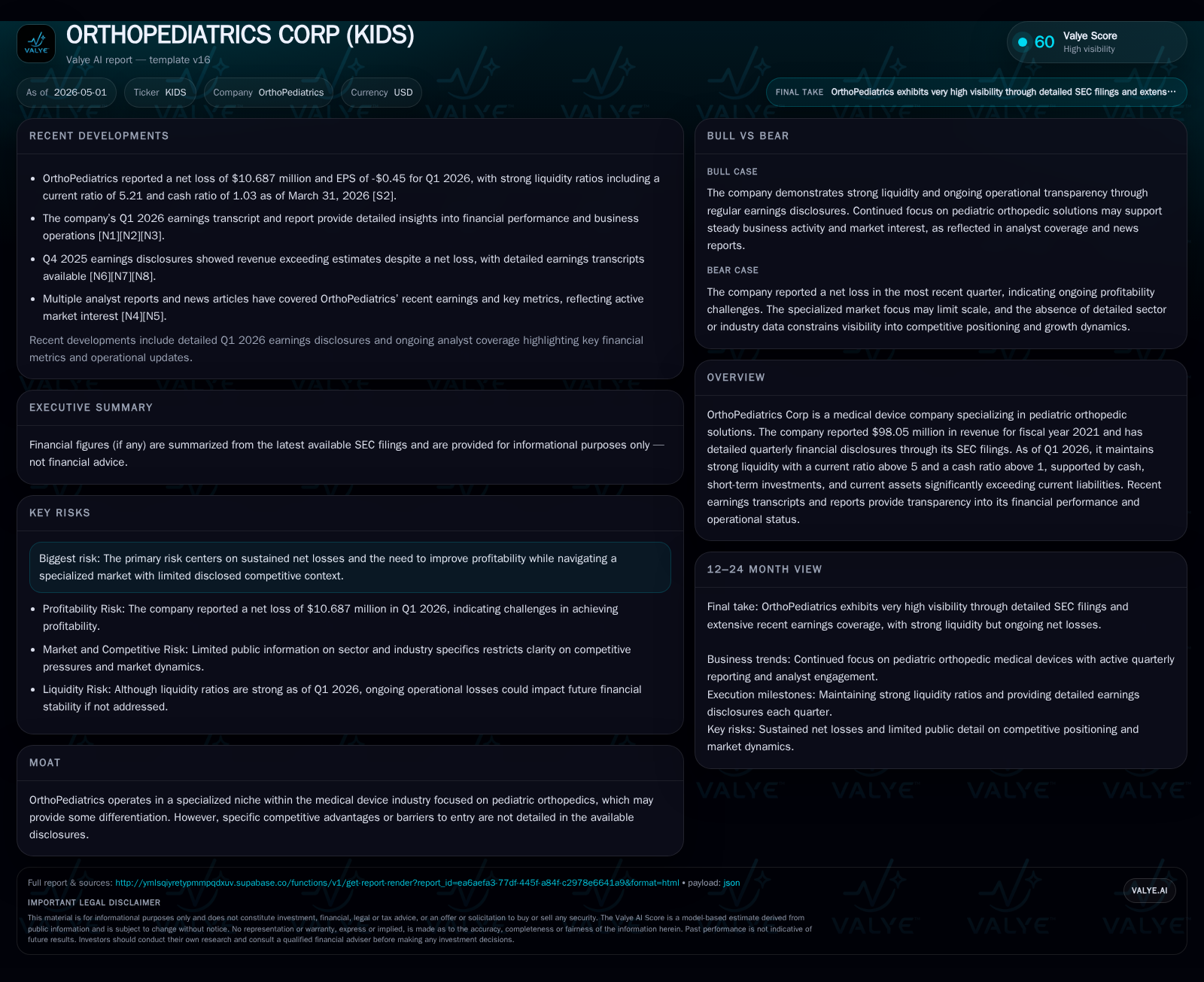

OrthoPediatrics Corp Accelerates Pediatric Orthopedic Market Penetration with Q1 2026 Momentum

OrthoPediatrics reported robust Q1 revenue growth supported by international expansion and product innovation despite ongoing operating losses and leverage challenges.

In its latest quarterly filing, OrthoPediatrics demonstrated notable progress in expanding its pediatric orthopedic market share, driven by new warehousing facilities and sales infrastructure in key international markets. While revenue outpaced estimates, the company continues to face operating losses amid heavy investment in growth initiatives. Its balance sheet shows strong liquidity with a current ratio above 5, though net debt remains significant. The firm’s specialized pediatric implants and bracing portfolio, underpinned by contract manufacturing and in-house production, positions it distinctively in a niche segment with moderate regulatory barriers.

Q1 2026 Operational Update: Revenue Growth and Margin Dynamics

For the quarter ended March 31, 2026, OrthoPediatrics Corp. disclosed continued top-line momentum despite persistent operating losses [S2]. The company reported revenues ahead of street estimates as elective pediatric surgeries showed signs of recovery following disruptions from COVID-19 and RSV episodes over the prior years [N2], [N3]. This uplift was particularly notable given the niche nature of its business where procedure volumes are inherently linked to hospital operational capacity.

However, operating expenses increased reflecting ongoing investments in sales infrastructure, including staffing hires and international logistics capabilities [N1]. The firm’s earnings transcript underscored that while profitability remains elusive this quarter, strong demand fundamentals support a positive outlook for scaling margins over time. Management highlighted that gross margin dynamics remained stable but driving down operating loss requires continued volume scale alongside cost discipline [N1].

Business Model and Product Portfolio: Specialized Pediatric Orthopedics and Innovation

OrthoPediatrics’ business model revolves around designing, producing, and marketing a comprehensive suite of anatomically appropriate orthopedic implants, surgical instruments, and specialized braces for children [S1]. Revenue arises primarily from sales of implants developed under contracts with third-party manufacturers, whereas orthotic bracing products are largely produced internally. This dual approach offers benefits in cost control for braces while leveraging partner expertise for complex implant manufacturing.

Flagship products include PediLoc® plates and screws designed exclusively for pediatric anatomies, ApiFix® minimally invasive scoliosis correction systems acquired in 2020, and specialty bracing such as Boston Brace 3D®. This portfolio addresses multiple pediatric conditions—from trauma to deformity correction—providing surgeons with tailored solutions that differ substantially from adult orthopedic offerings. The product mix thus captures both implantable devices used intraoperatively and external braces geared towards non-surgical management.

Competitive Positioning within the Pediatric Orthopedic Device Industry

Operating within a focused pediatric orthopedic segment distinguishes OrthoPediatrics from broader medical device peers [S1]. This specialization creates some natural barriers—surgeons require devices precisely fitting smaller skeletal structures which adult implants cannot accommodate. Furthermore, regulatory approvals tailored to pediatric populations impose moderate hurdles to entry, contributing to switching costs for hospitals committed to these systems.

The competitive landscape includes limited direct pediatric device providers; however, adjacent adult orthopedic companies occasionally encroach by modifying adult devices off-label for children. OrthoPediatrics counters this through ongoing innovation pipelines and clinical partnerships emphasizing long-term pediatric outcomes. Still, as disclosed risks highlight [S1], reimbursement dynamics and evolving healthcare regulations present constant operational challenges.

Growth Drivers: International Expansion and Adjacent Market Offerings

A key visible driver this quarter is the accelerated international rollout. Legal entities were recently established in Brazil (Nov 2025), complementing already operational subsidiaries in Europe (Netherlands, Germany), Australia, Canada, Belgium, Italy, Switzerland, Austria, UK, New Zealand—all aimed at direct sales rather than agent models [S1]. Warehouses opened in the Netherlands (July 2025) and Australia (February 2024) underpin these efforts by reducing lead times and improving local service.

Additionally, acquisitions such as ApiFix® (2020) and MD Ortho (2022)—the latter providing clubfoot products—broadened OrthoPediatrics’ clinical reach into related pediatric deformity domains. Such strategic expansions help mitigate elective surgery volatility witnessed during health crises by diversifying therapeutic applications across multiple pediatric subspecialties.

Risks and Constraints: Profitability Challenges, Debt Load, and Market Sensitivities

Despite growth progress, profitability remains challenging with operating losses persisting per latest filings [F1]. High fixed costs associated with R&D investments, international infrastructure buildout, marketing efforts focused on surgeon education/expertise development all weigh heavily.

The company carries substantial net debt near $94.46 million against $12.2 million cash reserves as of March 31, 2026 [F1]. OrthoPediatrics demonstrates strong short-term liquidity reflected by a current ratio above five [F1].

Moreover, sensitivity to global health emergencies—including COVID-19 or RSV surges—remains acute. These have historically constrained elective surgeries critical to implant demand volumes [S1], [S2]. Supply chain disruptions due to geopolitical tensions or material shortages could also impair timely product availability.

What To Watch Next: Milestones in Geographic Rollout, Profitability Levers, and Regulatory Landscape

Looking forward, near-term execution hinges on scaling international sales effectiveness following recent warehouse openings and legal entity establishments [N1], [S1]. Monitoring sequential sales improvements from these regions will indicate traction beyond U.S. core markets.

Regulatory filings or clearances on novel products or enhancements will signal pipeline vitality critical to sustaining competitive edge. Likewise, tracking progress on cost containment efforts amidst rising labor and material expenses will illuminate path toward operating leverage.

Lastly, any guidance updates regarding break-even timelines or incremental free-cash-flow visibility emerging from corporate communications should provide meaningful directional clarity.

Financial Snapshot: Balance Sheet Strength Amid Operating Losses

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $12mm | |

| 2026-03-31 | ||

| Total debt | $107mm | |

| 2026-03-31 | ||

| Net debt | $94mm | |

| 2026-03-31 | ||

| Current assets | $246mm | |

| 2026-03-31 | ||

| Current liabilities | $47mm | |

| 2026-03-31 | ||

| Current ratio | 5.21x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Despite nearly $95 million net debt on the balance sheet at quarter end [F1], OrthoPediatrics demonstrates strong short-term liquidity reflected by a current ratio above five [F1]. This stems from high current assets relative to liabilities combined with cash plus short-term investments totaling over $12 million [F1]. Operating losses continue as investments ramp up but robust liquidity cushions mitigate immediate solvency concerns.

This financial posture supports continued capital deployment toward growth initiatives including international expansion warehouses established recently along with hiring of operating personnel across new geographies [S1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments