Seer, Inc. Reframes Proteomics Commercialization With New Acquisition Proposal

Seer’s April 2026 unsolicited acquisition offer intersects with early-stage commercialization dynamics of its Proteograph platform amid competitive biotech pressures.

In late April 2026, Seer, Inc. disclosed receipt of a highly contingent, unsolicited acquisition proposal accompanied by director nominations, signaling potential governance and valuation impacts during a critical early commercial phase. The company’s business model revolves around its integrated Proteograph Product Suite, combining hardware, consumables, proprietary nanoparticles, and software primarily for research institutions—a complex offering with concentrated customer revenue. Operating in a fragmented proteomics landscape with established competitors and evolving regulatory scrutiny over research-use labeling, Seer’s growth hinges on scientific adoption and platform penetration amidst market and execution risks. Upcoming milestones include monitoring sales traction, product development progress, and responses to the acquisition overture. Financially, Seer maintains a robust cash reserve supporting ongoing commercialization losses inherent to its early-stage lifecycle.

Recent Strategic Development: The Acquisition Proposal and Its Implications

On April 27, 2026, Seer filed an 8-K disclosing receipt of a revised unsolicited acquisition proposal dated April 24 from investors Bradley L. Radoff, Michael Torok, and affiliates [S3][S5]. The bid was highly contingent on financing and other conditions that rendered it non-binding. Alongside the offer came nominations for new directors proposed by these investors. Importantly, Seer's Board of Directors unanimously rejected this proposal shortly after [S17].

This unexpected overture arrives at a pivotal juncture as Seer navigates the commercialization of its Proteograph Product Suite amid early-stage execution challenges [S1]. The timing likely reflects perceived valuation disconnects given ongoing operational losses and concentrated customer revenue. While non-binding status tempers immediate strategic shifts, such proposals often prompt management and shareholders to reevaluate governance structures and path-to-value propositions.

From an investor perspective, this event injects uncertainty but also volatility into near-term expectations. It highlights market debates over intrinsic worth juxtaposed against nascent commercial traction and sector dynamics. The company's explicit rejection signals confidence in its current trajectory or desire to avoid disruption during scale-up.

Seer’s Business Model: Integrated Proteograph Suite and Customer Dynamics

Seer's core business revolves around its integrated Proteograph Product Suite — which combines automation instruments, proprietary engineered nanoparticles packaged as consumables, and accompanying software for high-throughput proteome analysis [S1][F1]. Revenue streams are generated from sale of instruments alongside recurring consumable nanoparticle kits essential for each assay run.

Customers predominantly include commercial entities focused on drug discovery, academic research institutions pushing proteomics boundaries, and research organizations analyzing complex biological systems [S1]. This mix entails varying buying cycles but generally favors specialized platforms delivering novel data productivity.

Manufacturing is contracted to Hamilton Company under strict quality control protocols reflecting the complexity of nanoscale components combined with precision instrumentation [S1]. This outsourcing model allows Seer to focus on R&D innovation but introduces dependency risk as scale grows.

Currently revenue is concentrated among relatively few clients due to early-stage market penetration; this customer concentration amplifies earnings volatility but underscores initial adopter reliance typical in proteomics technology launches.

Competitive Context: Industry Structure and Barriers in Proteomics Technology

The proteomics arena blends legacy life sciences giants—offering established mass spectrometry platforms—with emerging niche providers focusing on novel protein capture or detection technologies [S1][S4]. Competitors wield broader product portfolios facilitating bundled sales while potentially leveraging entrenched customer relationships.

Seer's moat centers on combining hardware precision with proprietary nanoparticle chemistries enabling deeper proteomic coverage without sacrificing throughput or reproducibility [S1]. Its software complements this ecosystem providing analytical clarity—a critical factor given complex data outputs.

All products carry Research Use Only (RUO) labeling disclaimers per FDA guidelines; this avoids rigorous clinical diagnostics clearance but invites regulatory scrutiny particularly as customers explore translational applications [S4][S14].

Switching costs arise partly from integration depth between hardware-consumables-software suites forming locked-in user experiences though scientific workflow adoption remains fluid given alternative methods.

Ongoing collaborations with academic labs sustain validation cycles adding scientific credibility — essential in sustaining market acceptance vis-à-vis competitors who may emphasize scale or price advantages.

Growth Catalysts: Adoption Drivers and Market Penetration Opportunities

Seer's growth thesis is anchored in accelerating scientific validation across large-scale studies proving value over legacy methods [S1]. Such evidence supports broader institutional adoption beyond initial footholds.

Sales and marketing ramp-up is underway per public filings indicating increased headcount investments geared toward educating prospects about platform advantages [S2]. This will be critical in shortening sales cycles in typically conservative biotech procurement environments.

Recurring revenue from consumables forms a foundation for cash flow predictability once installed base scales materially; consumption patterns reflect assay frequency aligned with research intensity [F1].

Innovation pipeline extensions within the Proteograph framework — whether enhanced nanoparticles or software algorithm improvements — present opportunities for upselling existing customers or unlocking adjacent market segments if regulatory pathways open for clinical diagnostics.

Despite early progress indicators in select accounts referenced in disclosures [S2], structural challenges tied to concentrated revenue must be mitigated through portfolio expansion or diversification across sectors (pharma vs academic vs CROs).

Navigating Risks: Commercialization Hurdles, Customer Concentration, and Competition

Persistent net losses underscore the typical burn profile for cutting-edge life sciences technologies transitioning from R&D to commercial operations [F1][S2]. Achieving sustainable profitability depends heavily on successful market expansion which remains uncertain.

Manufacturing complexity dependence on third-party suppliers carries risks related to capacity constraints or quality deviations impacting delivery timelines or reliability perceptions [S1].

Customer concentration risk persists as early adopters drive most revenues; failure to broaden customer base swiftly could expose financial volatility especially if any large client reduces orders [S2].

Competition demands continuous technical innovation lest rivals erode share through lower cost bases or complementary capabilities offered by larger ecosystem players [S4].

Regulatory landscapes around RUO categorization retain ambiguity; any shift mandating clinical clearance could raise costs or stall adoption cycles significantly given FDA enforcement precedents reviewed in filings [S4][S14].

Upcoming Milestones: Key Indicators to Monitor for Execution Progress

Investors should track forthcoming quarterly disclosures updating sales performance metrics—especially figures indicating incremental instrument installations or consumable volumes sold reflecting adoption velocity [S2].

Announcements regarding new product features or partnership expansions would signal healthy product pipeline momentum reinforcing competitive differentiation.

Board decisions linked to unsolicited acquisition proposal outcomes represent another tactical focal point—whether further negotiations emerge or proxy contests materialize is relevant for governance stability assessments [S3][S17].

Regulatory developments impacting RUO labeling guidelines or diagnostic-related policies at FDA could materially influence legal compliance frameworks applicable to Seer's offerings [S4][S14]. Staying attuned to such external shifts is imperative.

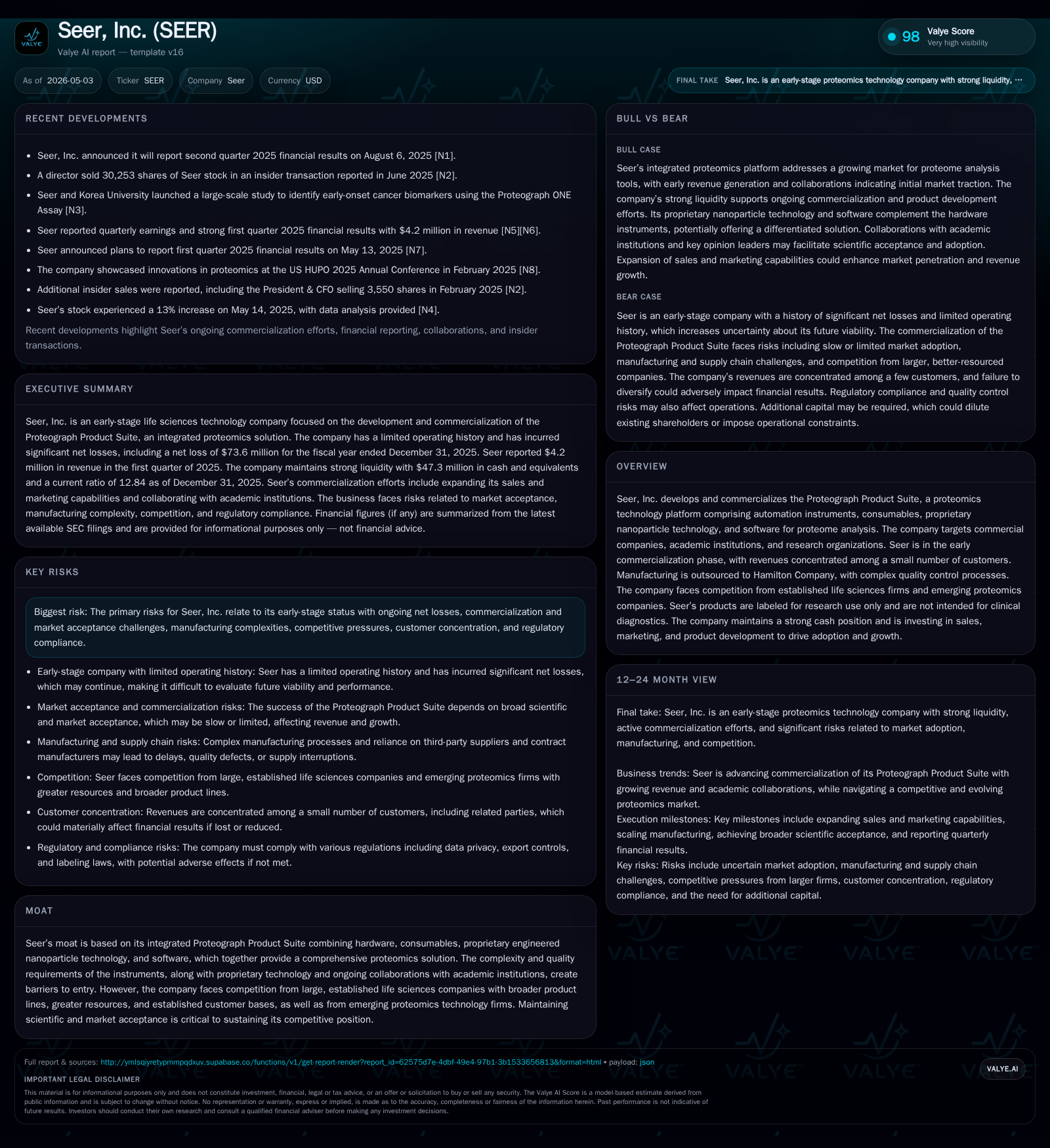

Financial Profile: Current Position and Operational Burn

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $47mm | |

| 2025-12-31 | ||

| Current assets | $202mm | |

| 2025-12-31 | ||

| Current liabilities | $16mm | |

| 2025-12-31 | ||

| Current ratio | 12.84x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

According to the most recent available SEC companyfacts dated December 31, 2025, Seer holds approximately $47.3 million in cash and equivalents against current liabilities of $15.7 million yielding a robust current ratio of ~12.8—indicating solid near-term liquidity [F1].

Conversely operating income registers a substantive loss of $77.9 million reflecting ongoing investments necessary for commercial scale out during this nascent phase [F1]. Such burn rates emphasize the capital-intensive nature typical of innovative life sciences tech firms pre-profitability.

This financial posture underscores reliance on existing cash reserves coupled potentially with public equity offerings or partnerships to fund accelerating commercialization expenses including salesforce buildout and R&D enhancements [S2][S21].

This analysis focuses exclusively on information publicly disclosed as of May 2026 without prognostications regarding future outcomes or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments