Annaly Capital Management’s Q1 2026 Update Highlights Agency MBS Strategy Amid Interest Rate Volatility

Annaly’s latest quarterly report emphasizes its continued focus on Agency mortgage-backed securities and managing risks in a competitive mortgage REIT landscape.

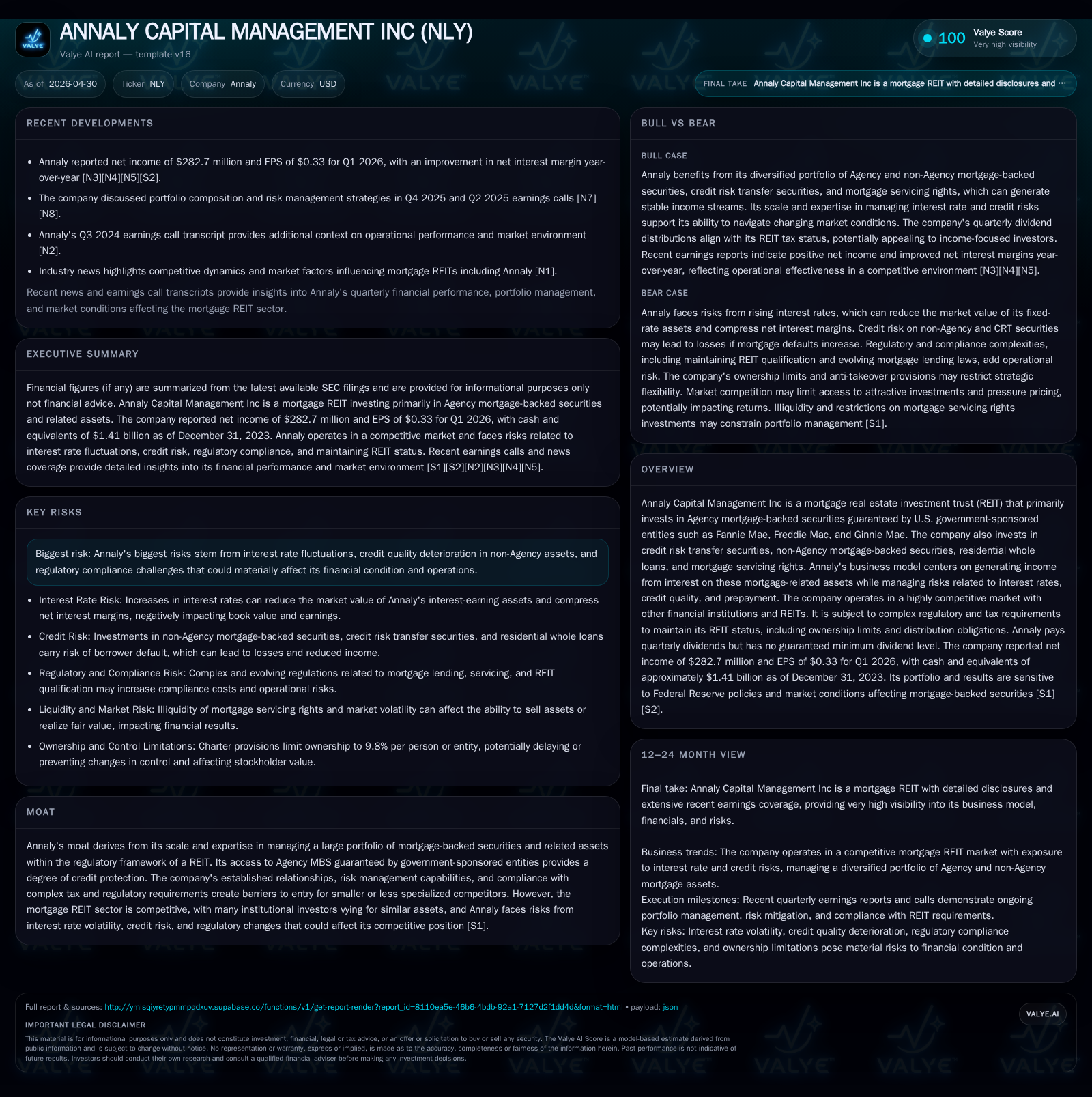

Annaly Capital Management reported first-quarter 2026 results reflecting stable net interest margins and ongoing exposure to Agency mortgage-backed securities (MBS). The company reaffirmed its approach of leveraging government-sponsored entity guarantees to mitigate credit risk while cautiously expanding in non-Agency and credit risk transfer assets. Regulatory compliance and interest rate fluctuations remain critical risks, but Annaly’s scale and expertise position it well within a challenging environment. The path forward depends on navigating cyclical interest rate dynamics and maintaining disciplined asset allocation.

Recent Operating Update and Its Significance

Annaly Capital Management’s first-quarter 2026 Form 10-Q filing (April 29) reiterates stability in its core business despite ongoing macroeconomic headwinds [S2]. The company reported consistent net interest margins supported primarily by its Agency MBS holdings—securities backed implicitly by U.S. government-sponsored entities (GSEs) such as Fannie Mae, Freddie Mac, and Ginnie Mae. There were no material changes in its risk disclosures compared with the February 2026 annual report [S4], highlighting continuity in the near-term operational outlook.

An event filing dated April 21 provides further details on preferred stock series outstanding but does not indicate significant strategic shifts [S3–S8]. Together these filings signal that Annaly maintains its existing investment theses while adapting tactically to evolving rate environments.

Business Model: Income Generation via Mortgage Securities

Annaly is a mortgage real estate investment trust (REIT) that generates revenue principally through interest earned on a diversified portfolio of mortgage-related assets [S1]. The predominant component is Agency mortgage-backed securities—mortgage pools bundled with explicit or implicit government guarantees. This backing significantly reduces credit risk compared to non-Agency counterparts.

The company also invests in credit risk transfer (CRT) securities, non-Agency MBS, residential whole loans, and mortgage servicing rights (MSR). CRTs allow Annaly to gain exposure to credit risk premiums otherwise unavailable within the Agency sector. MSRs represent contractual rights to service mortgages for fees and excess spread but are illiquid with regulatory oversight complexities. Residential whole loans provide direct loan ownership but entail borrower credit risk.[S1]

Revenues fluctuate with volume of assets held, prevailing interest rates impacting yields and prepayment speeds altering cash flows. Annaly seeks to optimize returns while hedging interest rate sensitivity through derivatives strategies and cautious asset-liability management.

Industry Structure and Competitive Positioning

The mortgage REIT space is highly competitive with peers including other specialist REITs and institutional financial entities actively deploying capital into similar asset classes [S22].

Annaly leverages scale as one of the largest mortgage REITs to access large pools of Agency MBS efficiently. Its experience in navigating complex tax rules governing REITs—including ownership limits under federal law and its charter-imposed restriction preventing any shareholder from exceeding 9.8% ownership—strengthens its defensibility against hostile takeovers [S1]. Sustained higher rates can widen spreads benefiting net interest income but present refinancing risks affecting portfolio duration strategies.[N4][N5]

Additionally, secular demand drivers such as the persistent role of housing finance support from the government entities underscore a stable asset supply pipeline conducive to investment.

Risks and Watchpoints

Key risks outlined in filings remain mostly unchanged but critical:

- Interest Rate Volatility: Rate spikes can erode portfolio valuations while compressions cause margin pressure.

- Credit Quality Deterioration: Especially acute for non-Agency securities backed by subprime or lower-quality loans exposing the firm to write-downs or losses.[S26]

- Regulatory Compliance: The complex evolving landscape governing residential credit activities including servicing standards heightens operational risk [S20][S25].

- Counterparty Risk: Possibility of losses from default events on exposures related to derivative counterparties or loan sellers who fail warranties [S16].

- Dividend Uncertainty: No minimum payout level means distributions may fluctuate based on earnings performance linked closely to market conditions [S21].

- Geographical Concentration: Regional economic downturns or climate-change-driven weather events could disproportionately impact collateral values [S28][S29].

Maintaining a robust hedging framework alongside conservative underwriting for direct loan acquisitions will be essential guardrails moving forward.

What To Watch Next

Several aspects will provide forward visibility into Annaly’s trajectory:

- Changes in net interest margin with shifts in Fed policy announcements given their outsized influence on MBS yields.

- Portfolio mix evolution toward greater non-Agency holdings balancing yield enhancement against risk appetite.

- Updates on regulatory developments impacting mortgage servicing practices e.g., CFPB guidelines affecting operational costs.

- Dividends declared per share providing real-time insight into cash flow sustainability.[N4][N5]

- Any moves by management to modify shareholder ownership limits or capital structure adjustments given existing anti-takeover measures.

Earnings calls transcripts from April 2026 reinforce management’s intent on maintaining a disciplined stance within volatile markets [N3].

Financial Profile Summary

Public data indicates Annaly held $1.41 billion in cash and equivalents as of December 31, 2023, reflecting substantial liquidity [F1]. Total debt figures from earlier periods suggest relatively modest leverage compared to cash balances, implying potential flexibility in asset deployment or debt amortization strategies. Overall financial positioning combined with operating expertise supports Annaly’s ability to manage through market cycles.

Conclusion

Annaly Capital Management stands as a leading mortgage REIT anchored by robust investments in Agency MBS backed by GSE guarantees that reduce credit exposure relative to peers focusing heavily on non-guaranteed assets. Q1 2026 updates reflect steady performance sustained via comprehensive hedging approaches amid complicated macroeconomic settings marked by fluctuating rates. Its business model emphasizing income generation through multiple complementary mortgage-related asset classes demonstrates adaptability yet requires continuous vigilance due to embedded risks spanning interest rates, credit quality variation, regulatory complexity, and environmental factors.

Annaly's competitive position benefits from scale-driven access, regulatory mastery enabling REIT qualification maintenance under ownership limitations, and diversified product offerings attracting institutional capital alongside retail investors seeking yield alternatives. Subsequent periods will test execution discipline especially concerning portfolio allocation shifts toward non-agency sectors while safeguarding shareholder value amidst external uncertainties.

This analysis is based exclusively on public SEC filings dated through April 29, 2026 [S2,S3,S1] plus contemporaneous news sources [N3,N4,N5] without any proprietary or unpublished information. It is intended for informational purposes consistent with Valye News policy adherence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments