Yatsen Holding’s Strategic Brand Reset Lifts Skincare Revenue and Margins

Yatsen’s return to profitability and revenue growth in Q4 2025 underscores its successful pivot toward skincare amid China’s regulatory capital controls.

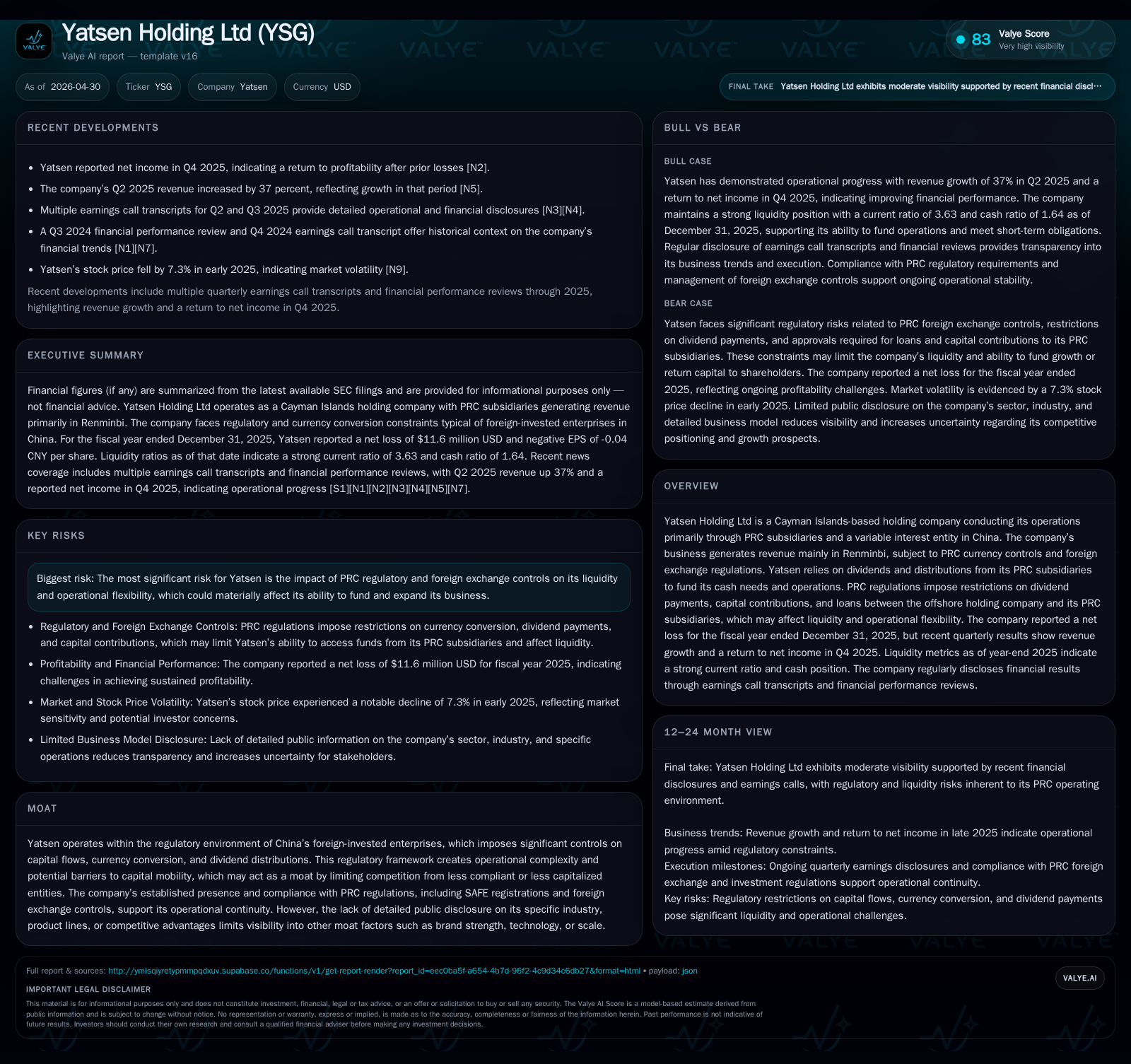

In the latest quarterly filings for early 2026, Yatsen Holding Ltd reported a meaningful rebound with revenue growth and a return to net income, reflecting operational progress after years of losses. This recovery is driven by a strategic portfolio shift favoring skincare brands, which now account for over half of revenues, supported by sustained R&D investment and premium product innovation. While the company navigates complexity imposed by PRC foreign exchange and dividend restrictions inherent to its holding structure, Yatsen’s enhanced brand equity and operational agility underpin its competitive position in China’s beauty market. Ongoing risks center on regulatory uncertainty and capital mobility constraints.

Latest Quarterly Operating Update: Path to Profitability

Yatsen Holding Ltd’s most recent quarterly disclosures for early March 2026 reveal a notable operational turnaround anchored by growth in revenue and a return to profitability from prior net losses. The Q4 2025 financial release documents an increase in net revenues to RMB4.30 billion (approximately $614.6 million), representing a rebound from flat-to-declining revenues in preceding years [S3]. Concurrently, the company narrowed its net loss dramatically from RMB710 million in 2024 to RMB92 million ($13.2 million) in 2025 [S3], demonstrating execution momentum on its strategic plan.

Additionally, an announced private placement involving convertible notes and warrants in March 2026 suggests an effort to bolster capital resources aimed at supporting ongoing brand development initiatives and navigating the complex funding environment shaped by China’s regulatory landscape [S2].

In tandem with this improved topline and bottom-line performance, gross margin expanded sharply from approximately 73.6% in 2023 to over 78% in 2025, reflecting both portfolio mix effects favoring higher-margin skincare products and prudent pricing discipline [S14][S3]. This margin expansion underscores effective operational calibration across supply chain optimization and discount management.

Business Model and Multi-Brand Portfolio Dynamics

Yatsen is fundamentally a multi-brand beauty group operating predominantly within mainland China through its Cayman Islands holding structure utilizing variable interest entity (VIE) arrangements [S1]. Its business model centers on developing distinctive color cosmetics and increasingly prioritized skincare brands that address a broad consumer demographic spectrum — from mass-market entry-level consumers through mid-tier offerings up to prestige clinical segments.

Since its founding in 2016, Yatsen has launched flagship brands such as Perfect Diary (color cosmetics with strong youth appeal), alongside key acquisitions including Galénic (premium European dermo-cosmetics), DR.WU (clinically validated dermatological skincare), and Eve Lom (luxury skincare) [S1]. The strategic pivot beginning in early 2022 has concentrated corporate resources on elevating skincare as the principal growth engine — boosting its share of total revenue from roughly one-third in 2022 to more than half by year-end 2025 [S1].

This portfolio repositioning exploits superior brand equity associated with scientifically-backed formulations and premium positioning that yield stronger pricing power than typical mass-market color cosmetics. Proprietary R&D capabilities underpin product innovation—facilitating newer high-margin SKU introductions that accelerate customer retention and cross-brand sales synergies.

Distribution channels combine online e-commerce platforms with an omnipresent offline footprint through curated experience stores located strategically across China's tiered cities. Despite a modest net reduction in total stores (from 88 stores at end-2024 to 77 at end-2025), Yatsen rebalanced its retail presence towards expanding Galénic's physical footprint while winding down less profitable Perfect Diary outlets — aiming for an optimized touchpoint engagement strategy blending physical sampling with social commerce leverage via Weixin groups where beauty advisors drive personalized interactions [S1].

Industry Environment and Regulatory Moat

Operating within the preciseing regulatory environment of China’s cosmetics sector — itself evolving under tightened government oversight concerning quality standards, cybersecurity content control, data privacy laws, as well as merger & acquisition review — Yatsen contends with significant compliance demands that constrain operational flexibility but raise barriers for less compliant entrants [S1][S27].

Structurally, foreign exchange controls imposed by SAFE Circulars on cross-border capital flows substantially delimit Yatsen's ability to remit dividends or inject fresh capital efficiently between its mainland subsidiaries and offshore holding entity. These restrictions create intrinsic liquidity bottlenecks despite consolidated profitability at group level [S1][S27]. Consequently, contractual VIE arrangements must navigate legal ambiguity while preserving operational continuity.

While these regulations present risks around financing agility and dividend repatriation timing uncertainties, they also erect a protective moat restricting easily scalable foreign competitors or undercapitalized local challengers lacking comprehensive regulatory compliance frameworks or the necessary SAFE registrations.

Growth Drivers: R&D Focus and Skincare Expansion

Yatsen’s strategic renewal hinges critically on innovation-led growth with consistent annual R&D expenditure surpassing three percent of net revenues since 2022—a figure signaling commitment above average cosmetics industry norms within regional peers [S1][S19]. The company leverages its investment into specialized formulations exemplified by Galénic’s vitamin C brightening serums and anti-wrinkle lines; DR.WU's dermatologist-backed hypoallergenic products; alongside an expanding pipeline backed by clinical efficacy data.

This innovation vector increases average selling price metrics while strengthening customer loyalty via demonstrable results—decisive factors accelerating skincare’s compound annual growth rate (~22.4% over three years ending 2025) [S1]. Additionally, Yatsen’s omni-channel ecosystem provides real-time consumer insights fueling agile new product launches responsive to fast-evolving preferences.

Geographic expansion beyond core China markets into selected Asian territories and Europe under Galénic branding reflects ambition for international brand elevation driven by scientific heritage appeal—a differentiation factor given limited global presence among Chinese-origin beauty players at this level of prestige positioning.

Risks and Operational Constraints from PRC Controls

Notwithstanding operating improvements, significant risks derive from onerous PRC foreign exchange regulations limiting offshore dividend distributions which impact cash flow agility between subsidiaries and holding company—critical given Yatsen's dependency on such flows to fund global initiatives or service any external financing obligations [S1][S27].

Moreover, governmental scrutiny over content marketing via social media platforms due to cybersecurity review requirements introduces potential volatility if future rules restrict digital engagement channels currently pivotal for brand promotion.

Legal ambiguities surrounding VIE contractual enforceability under evolving PRC legislation remain notable risk aspects that could affect ownership structures or investor sentiment. Any adverse shifts requiring approvals from authorities like CSRC could hamper fundraising or compliance costs materially.

What to Watch Next: Milestones and Demand Signals

Upcoming quarters will offer clarity on Yatsen’s capacity to maintain revenue momentum and further shrink losses towards sustained profitability through improved operating leverage. Key indicators include:

- Progress updates on expanding Galénic’s offline store footprint balanced against rationalizing other brand presence,

- Release cadence for novel skincare product lines reinforcing innovation pipeline credibility,

- Execution effectiveness of recently raised convertible note proceeds targeting growth support,

- Initial evidence of international market penetration gains,

- Regulatory developments around foreign exchange reform or cybersecurity licensing impacting operational flexibility.

Monitoring these dimensions will be critical for assessing whether Yatsen can translate its strategic resets into durable competitive advantage within China's dynamic beauty market framework.

Current Financial Snapshot: Liquidity and Margin Improvement

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $109mm | |

| 2025-12-31 | ||

| Current assets | $319mm | |

| 2025-12-31 | ||

| Current liabilities | $88mm | |

| 2025-12-31 | ||

| Current ratio | 3.63x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD million) | Period Ending |

|---|---|---|

| Cash & Equivalents | 109.4 | |

| 2025-12-31 | ||

| Current Assets | 319.5 | |

| 2025-12-31 | ||

| Current Liabilities | 88.0 | |

| 2025-12-31 | ||

| Current Ratio | 3.63 | |

| 2025-12-31 | ||

| Net Income | -11.6 | |

| 2025-12-31 | ||

| Operating Income | -26.6 | |

| 2025-12-31 |

Source: Latest audited financial statements filed April 29, 2026 [F1]

Yatsen enters the post-2025 period with a solid liquidity buffer supported by $109 million cash plus a healthy current ratio well above industry averages that enables it to manage near-term obligations comfortably despite lingering net loss positions reflecting ongoing investments into marketing personnel and brand-building activities [F1][S1]. Gross margin improvement toward the high-70s percentage range validates effective pricing discipline alongside targeted cost optimization efforts executed during the strategic transformation process.

This analysis focuses strictly on Yatsen Holding Ltd's operational developments as disclosed through SEC filings up to March-April 2026 without any investment recommendation. It integrates detailed examination of the company's business model evolution amidst China's changing regulatory environment alongside key financial metrics that contextualize recent performance trends.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments