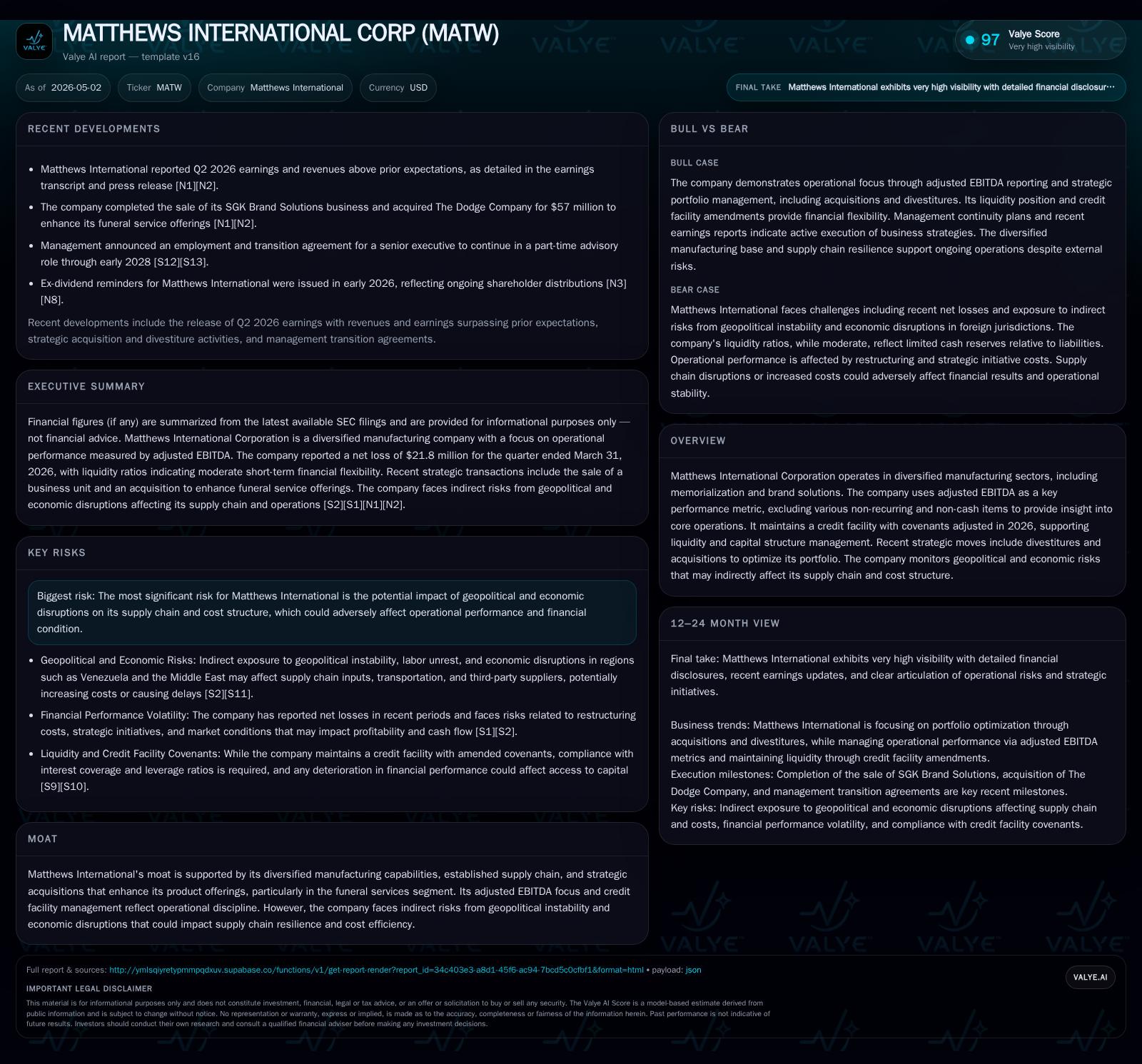

Matthews International Elevates Operational Resilience with Strategic Portfolio Adjustments

The latest quarterly filing reveals Matthews International's focus on portfolio optimization and supply chain resilience amid evolving geopolitical challenges.

In Q2 2026, Matthews International demonstrated operational discipline through strategic divestitures and acquisitions aimed at enhancing its manufacturing portfolio. The company maintains adjusted EBITDA as a core performance metric to navigate cost pressures and integrates supply chain diversification to mitigate rising geopolitical risks. Growth is expected to be driven by targeted acquisitions and margin improvement initiatives despite external uncertainties. Financially, Matthews sustains solid liquidity and leverage profiles enabling continued investment in core operations.

Q2 2026 Operating Update: Portfolio Realignments and Performance Highlights

Matthews International's latest quarterly filing dated May 1, 2026 ([S2], [S3]) underscores strategic efforts to optimize its business portfolio amid a challenging macroeconomic backdrop. The company executed targeted divestitures while adding complementary businesses that broaden manufacturing capabilities within its memorialization and brand solutions segments. These portfolio moves are designed not just to refine the revenue mix but also to shore up operational margins.

The filings reveal the company’s continued reliance on adjusted EBITDA as the primary internal performance metric, excluding items such as acquisition/divestiture costs, stock-based compensation, and one-time integration charges ([S1]). This disciplined financial focus aims to provide clear insights into core operating strength.

Management commentary in recent earnings transcripts ([N1], [N2]) highlights stable adjusted EBITDA margins despite inflationary headwinds and supply chain disruptions. While near-term growth was modest, the strategic repositioning sets the stage for stronger margin performance going forward.

A recent arbitration outcome affirmed Matthews’ rights in developing proprietary battery electrode technology, reflecting an effort to preserve innovation-related revenue streams ([S15]).

How Matthews Generates Value: Diversified Manufacturing Business Model and Product Integrity

Matthews International delivers products primarily through two broad segments: Memorialization (products related to funeral services and remembrance) and Brand Solutions (including brand identification, marking systems, and specialty industrial products) ([S1]). Revenue generation hinges on contracts with funeral homes, cemeteries, industrial customers, and branding clients.

The business model centers around high-quality manufacturing capabilities combined with tailored solutions leveraged through established distribution channels. The company's use of adjusted EBITDA emphasizes operating cash flow quality by stripping out non-operational noise such as acquisition expenses or ERP system integrations ([S1]). This approach aids stewards in budgeting capital efficiently across its diverse portfolio.

Margins fluctuate somewhat due to raw materials costs, labor inputs, and product mix shifts—particularly in the commoditized packaging segments within Brand Solutions. However, premium product lines in memorialization commonly yield better pricing power due to specialized craftsmanship and niche market relationships.

Competitive Moat and Industry Dynamics: Supply Chain, Production Capabilities, and Market Positioning

Matthews International’s competitive moat arises from its integrated manufacturing capabilities spanning multiple facilities globally combined with diversification across end markets (, [S1]). The company’s supply chain strategy aims at geographic spread to mitigate risk but is nonetheless susceptible to global logistics variability caused by geopolitical instability ([S2], [S13]).

Despite no direct exposure in volatile regions such as Venezuela or the Middle East, Matthews acknowledges intermediated risks via cost increases or delays from third-party suppliers affected by sanctions or political events ([S2]). This necessitates proactive supplier diversification and inventory buffers to maintain production continuity.

Regulatory changes related to trade tariffs or environmental compliance remain watchpoints but have been partially offset by Matthews’ ability to source alternate suppliers or adjust production schedules dynamically ([S2]). Pricing discipline helps offset some input cost inflation although competitive pressures limit full pass-through in certain segments.

Catalysts for Growth: Acquisitions, Margin Improvement Opportunities, and Market Penetration

Growth levers distinct from organic demand center heavily on Matthews’ incremental acquisitions that broaden product lines or enter adjacencies aligned with existing manufacturing expertise ([S2], [S3]). Integration efforts focus on leveraging existing sales channels for cross-selling while capturing synergies through operational streamlining.

Margin improvement initiatives emphasize adjusted EBITDA expansion through productivity gains and cost reductions targeted at legacy overheads or non-core activities ([S1], [N1]). Management has outlined plans for incremental pricing adjustments where market conditions allow along with more efficient capital allocation aided by improved credit facilities ([S5]).

Furthermore, expanding geographic reach in underpenetrated markets provides additional upside potential though tempered by globalization challenges.

Risks to Monitor: Supply Chain Vulnerabilities, Geopolitical Exposure, and Cost Pressures

The primary risk update in the Q2 2026 10-Q relates to increased geopolitical tensions leading to labor unrest abroad and disruptions affecting supply chains indirectly ([S2], [S13]). While Matthews has no direct operations in high-risk regions like Venezuela or Iran, the fallout from strikes or government actions imposes ripple effects on international trade flows impacting raw material availability and transportation logistics.

Currency volatility adds complexity to budgeting international costs while compliance with evolving trade restrictions requires ongoing diligence. Cost pressures from energy markets or inflation may erode margin if not counteracted by pricing actions or efficiency improvements.

No material new risk factors were introduced in the quarter other than updated geostrategic outlooks emphasizing vigilance in operational planning.

Key Milestones and Next Steps: Upcoming Earnings Guidance and Execution Benchmarks

Investors should track upcoming quarterly earnings announcements focusing on adjusted EBITDA trajectory which remains management's key performance anchor ([N1], [S3]). Integration status of recent acquisitions provides insight into execution effectiveness while capital expenditure trends will signal investment posture.

Supply chain resilience measures including supplier diversification metrics or inventory turnover improvements serve as operational health markers. Any changes in dividend policy or credit facility terms could also reflect underlying financial flexibility shifts ([S5], [S17]).

Financial Health at a Glance: Quarterly Snapshot of Liquidity, Debt, and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $36mm | |

| 2026-03-31 | ||

| Total debt | $572mm | |

| 2026-03-31 | ||

| Net debt | $536mm | |

| 2026-03-31 | ||

| Current assets | $480mm | |

| 2026-03-31 | ||

| Current liabilities | $293mm | |

| 2026-03-31 | ||

| Current ratio | 1.64x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 36,088,000 |

| Total Debt | 571,950,000 |

| Net Debt | 535,862,000 |

| Current Assets | 479,594,000 |

| Current Liabilities | 293,168,000 |

| Current Ratio | 1.64 |

Matthews holds about $36 million in cash against roughly $572 million total debt at quarter-end March 31, 2026 with a healthy current ratio near 1.64 reflecting adequate short-term liquidity ([F1]). The net debt position confirms moderate leverage consistent with prior periods but balanced against stable operating cash flow generation reflected in adjusted EBITDA figures approximately at $188 million annually as of FY2025 ([S1], [F1]).

The company’s credit facility terms updated earlier in fiscal year provide sufficient headroom for growth investments while requiring careful interest coverage monitoring ([S5]). Overall financial positioning supports Matthews' strategy of steady portfolio refinement alongside measured leverage management.

This analysis is based solely on publicly available SEC filings dated through May 2026 and selected news sources without any investment advice intended. The discussion reflects observed operating facts grounded strictly in cited disclosures without speculation beyond reported data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments