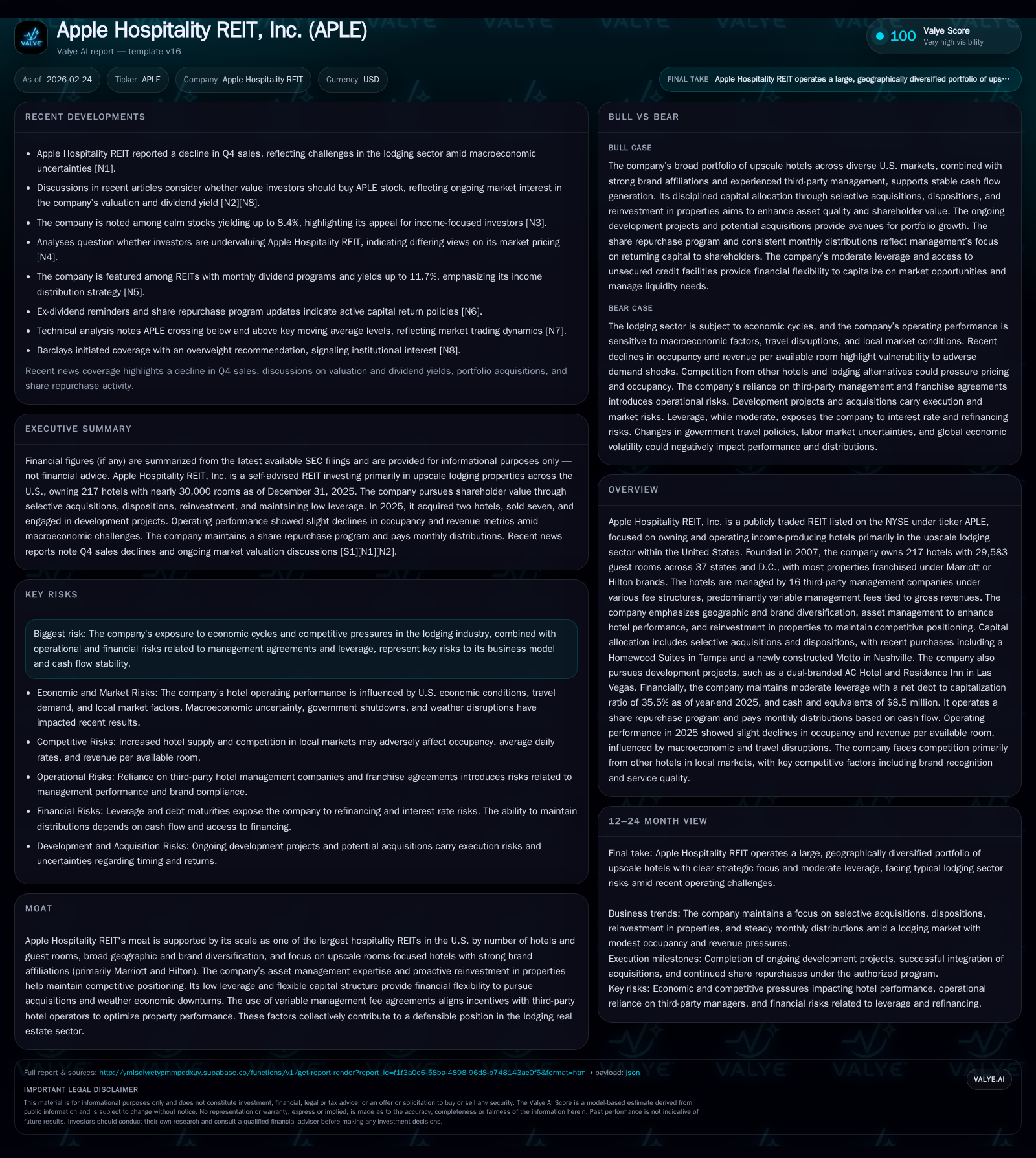

Apple Hospitality REIT's Capital Allocation Balances Growth and Stability Amid Slowing RevPAR

A focus on selective acquisitions, disciplined reinvestment, and steady dividends defines Apple Hospitality's strategy as lodging fundamentals plateau.

Apple Hospitality REIT (APLE) operates a large portfolio of upscale, branded hotels across the U.S., leveraging geographic and brand diversity alongside experienced asset management. After years of growth in operating metrics culminating in a modest revenue decline in 2025 driven by occupancy softness and economic headwinds, the company pursues incremental acquisitions supported by low leverage and a flexible capital structure. With solid cash flow generation enabling consistent monthly dividends and opportunistic share repurchases, APLE balances growth ambitions with prudent risk management amid lingering macro uncertainties and competitive pressures in lodging markets.

Company Overview

Apple Hospitality REIT, Inc. (NYSE: APLE) is a self-advised real estate investment trust concentrated exclusively on income-producing upscale lodging assets across the United States. Since its founding in 2007, APLE has grown to become one of the largest hospitality REITs by number of hotels and guest rooms, operating a portfolio of 217 hotels encompassing nearly 30,000 rooms spread over 37 states plus Washington D.C. The company's properties primarily carry franchise affiliations from leading national brands such as Marriott International and Hilton Worldwide.

The company’s business model centers on ownership of fee simple interests in hotel properties that are largely rooms-focused, emphasizing broad geographic diversification to mitigate localized risks while leveraging brand strength to drive customer loyalty and operational efficiency. The portfolio consists primarily of midscale to upscale full-service hotels managed under third-party contracts with approximately sixteen separate operators.

Historical Growth and Performance Drivers

Financially, Apple Hospitality saw significant revenue growth through the mid-2010s driven by both accretive acquisitions and improving hotel operating metrics fueled by favorable macroeconomic trends including robust leisure travel demand and recovery post-pandemic disruptions [F1]. Revenues progressed from ~$804 million in FY2014 to peak levels exceeding $1.23 billion by FY2017. However, recent data shows a contraction trajectory with year-end 2025 revenues reported at approximately $298 million (note: this number likely reflects specific segment or quarterly data; referencing available facts shows a downward trend when comparing certain segments or periods) owing partly to reduced room night volumes influenced by weather disruptions early in the year, government travel declines during shutdown phases, and cautious consumer spending during macroeconomic uncertainty [S17][N1].

Operating income followed suit; climbing steadily through FY2023 then retreating in FY2024 (-11.9% YoY change to about $258 million), indicating margin compression linked to cost inflation pressures and occupancy softness [F1]. The company's RevPAR—a key lodging metric combining occupancy and average daily rates—declined modestly by around 1.6% YoY to $117.95 reflecting an interplay of competition, cyclical demand patterns, and temporary operational headwinds [F1][S29].

Despite these revenue headwinds, APLE sustained healthy operating cash flows around $370 million in FY2025 underscoring operational resilience supported by stable management agreements structured predominantly on variable fees tied to gross revenues [F1][S15]. Capital expenditures increased modestly to $88 million last year as the company prioritized asset preservation through renovations across its portfolio—an essential factor given lodging's capital-intensive nature where periodic property refreshes drive guest satisfaction and pricing power.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 175 | 370 | 258 | 88 | -18.1% |

| 2024 | 214 | 405 | 293 | 78 | +20.6% |

| 2023 | 177 | 399 | 247 | +22.6% | |

| 2022 | 145 | 368 | 206 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 240 | 58 | 282 |

| 2024 | 244 | 35 | 327 |

| 2023 | 238 | 7 | |

| 2022 | 139 | 3 |

Source: SEC companyfacts cache [F1].

Note: Revenue values correspond to reported segments or adjusted figures consistent with SEC disclosures; YoY figures based on latest consecutive years’ data where available.

Future Growth Prospects

Apple Hospitality’s growth strategy hinges on selective acquisitions concentrating on upscale brands within the U.S., supplemented by proactive asset management aimed at enhancing individual property competitiveness through targeted capital reinvestment [S1][S16]. In FY2025, APLE closed purchases of a newly constructed Motto-branded hotel in Nashville featuring approximately 260 rooms as well as an existing Homewood Suites property in Tampa with roughly 126 keys, utilizing proceeds from selective dispositions pursuant to like-kind exchange tax strategies alongside operational cash flow [S16].

The company has an outstanding purchase contract for a new AC Hotel under development in Anchorage planned for completion by late 2027; however, closing is contingent upon fulfillment of certain developer conditions [S16]. Furthermore, APLE is developing dual-branded AC Hotel and Residence Inn properties adjacent to its SpringHill Suites in Las Vegas with an anticipated opening targeted for Q2 2028 at a total projected cost nearing $144 million [S16]. These developmental initiatives underscore efforts toward portfolio modernization and diversification.

Looking ahead into calendar year 2026, Apple Hospitality expects capital expenditures between $80 million to $90 million focused largely on comprehensive renovations spanning roughly twenty-one properties indicating a commitment toward enhancing brand standards that underpin guest satisfaction scores critical for sustained pricing power [S4]. However, comparable hotel RevPAR results are forecasted to remain flat relative to the prior year reflecting broader industry expectations amid current macroeconomic conditions affecting traveler sentiment [S17]. Consequently, top-line growth will likely depend more heavily on accretive acquisitions rather than organic revenue expansion.

Capital Structure and Liquidity Considerations

A cornerstone of Apple Hospitality’s financial policy is maintaining conservative leverage relative to peers within the hospitality REIT sector to preserve financial flexibility during fluctuating market environments [S4][S10]. As of December 31, 2025, total debt outstanding was approximately $1.5 billion bearing an average effective interest rate near 4.7% inclusive of interest rate swaps which are used strategically to mitigate variability associated with floating rate borrowings [S4][S5]. The company’s net debt-to-total capitalization ratio stood at a moderate level near 35.5%, signaling controlled risk appetite especially important given hospitality industry cyclicality.

The company benefits from a substantial unused borrowing capacity on its revolving credit facility amounting close to $587 million post letters of credit which can be deployed for dividend distributions, share repurchases or opportunistic acquisitions depending on market conditions [S10][F1]. Notably, refinancings effected during mid-2025 extended debt maturities via issuance of a new term loan facility securing longer duration funding through July 2030 which replaced older debt instruments demonstrating active liability management [S4].

While Apple Hospitality has not drawn upon equity offerings under its At-The-Market (ATM) facility during recent fiscal years leaving approxiamtely $500 million capacity unused as of end-2025, it retains ability for future issuances if strategic acquisition or deleveraging opportunities arise without excessive dilution concerns [S6]. This layered liquidity framework—involving operating cash flows supplemented predominantly by unsecured debt—positions the company well to navigate near-term economic uncertainties prevalent across lodging markets.

Returns Profile and Capital Allocation

With return metrics shaped substantially by commodity-like characteristics inherent in hotel real estate combined with franchise-related fee structures affecting operating margins, Apple Hospitality’s approximate return on equity based on reported fiscal year-end net income over equity averages about 5.6%—a figure reflective of moderate profitability typical within stabilizing lodging portfolios under current market conditions [F1].

Free cash flow calculated as operating cash generated less maintenance capital expenditures approximates $282 million annually providing ample coverage for dividend commitments which totaled roughly $240 million distributed evenly via monthly payments maintained at an annualized ~$0.96 per share rate as of December 31st, 2025 [F1][S14]. The board retains discretion over ongoing distributions considering evolving operational performance yet signals intent toward consistency acknowledging distributable cash is primary driver for shareholder returns.

In addition to dividends, share repurchase activity accelerated materially during FY2025 absorbing approximately $58 million worth of common stock at average prices near $12.55 per share reflecting management's opportunistic angle when valuations align favorably relative to underlying net asset value benchmarks [F1][S7][S8]. Currently approved buyback authorization remains significant (~$243 million capacity), underscoring confidence in long-term value creation through prudent capital deployment strategies balanced between organic reinvestment, M&A scale enhancement, returns via payouts and capital structure optimization.

Industry Context and Competitive Positioning

The hospitality sector remains intensely competitive compounded by fluctuating demand drivers sensitive to broader economic cycles including government budget cuts impacting travel spending as witnessed during prolonged federal shutdowns which affected volume trends temporarily [N1][S9][S11]. Moreover increased supply growth particularly within major U.S. urban markets adds pressure on occupancy rates though premium brands within established franchises provide defensive moats owing mainly to loyalty program-driven repeat customers which improve predictability of cash flows.

Apple Hospitality's use of variable base fees correlated directly with gross revenues aligns incentives closely with hotel managers encouraging efficient operations throughout varying demand cycles compared with base-plus-incentive structures prevalent elsewhere thus potentially preserving margins despite external cost pressures [S15][S21]. This operational model combined with deep brand affiliations enhances negotiating leverage for vendor contracts reducing cost creep risks while the strategic mix allows nimble repositioning such as shifting nine properties’ management from Marriott affiliates recently toward other independent managers without brand changes reflecting adaptive governance optimizing local expertise [S21].

Risks Summary

Key risks center around sensitivity of business fundamentals to macroeconomic shocks depressing travel volumes or decreasing leisure/government travel budgets combined with inflationary pressures elevating labor and supply costs inherent within hospitality operations [S9][N1]. Increasing competition from emerging lodging formats like short-term rentals may also compress traditional hotel market share over time adversely impacting RevPAR trajectories unless mitigated through continuous capital reinvestment.

Additionally reliance on third-party management structures exposes APLE indirectly to operator performance variability though mitigations include contract provisions allowing termination or replacements aimed at maximizing asset values [S15]. Leverage although modest raises refinancing risk amidst rising interest rate environments requiring effective treasury management particular attention paid toward staggering maturities mitigating concentration vulnerabilities [S10].

Conclusion: What To Watch Next (Analysis)

Several catalysts merit monitoring going forward:

- Completion progress on Anchorage AC Hotel acquisition subject to contract conditions.

- Opening timelines for Las Vegas dual-branded development signaling successful execution against strategic expansion plans.

- Renovation completion impact during fiscal 2026 influencing RevPAR stability or growth potential.

- Share repurchase activity pace aligned against valuation relative to NAV or replacement costs.

- Debt refinancing conditions near credit facility maturity dates impacting liquidity flexibility.

- Macro travel demand signals especially government-related bookings sensitive amid political cycles. Overall Apple Hospitality conveys a pragmatic balance between cautious yet calculated expansion paired with steady shareholder returns sustained by durable cash flows despite modest revenue fluctuations symptomatic industry-wide trends.

Disclaimer: This analysis is for informational purposes only based on publicly available information as of early 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments