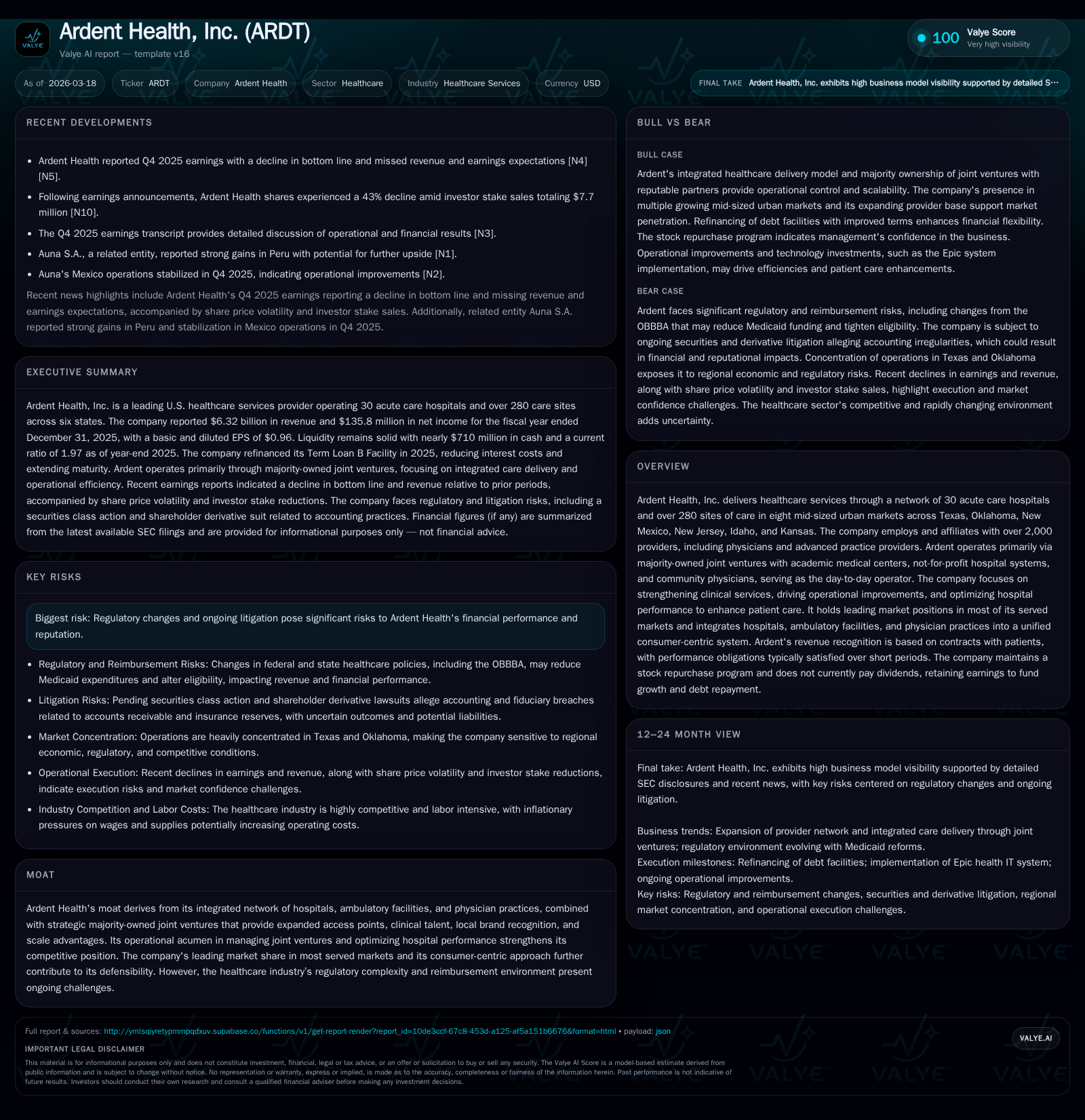

Ardent Health’s Revenue Growth Confronts Earnings Pressure and Legal Headwinds

Ardent Health advances in regional healthcare services with solid top-line growth but faces margin compression and litigation risks.

Ardent Health, Inc. operates a network of acute care hospitals and ambulatory sites primarily through majority-owned joint ventures, achieving consistent revenue growth driven by market expansion and operational improvements. Despite a 6% revenue increase in 2025 to $6.32 billion, net income declined sharply by over 35% due to higher expenses and restructuring costs amid ongoing legal challenges. The company maintains a strong liquidity position with $710 million cash on hand, low leverage ratios post refinancing, and moderate capital expenditures. Investors should monitor margin recovery initiatives, legal case developments, joint venture performance, and potential impacts of regulatory changes on reimbursement.

Company Overview

Ardent Health, Inc. manages a network of approximately 30 acute care hospitals and over 280 outpatient clinics across Texas, Oklahoma, New Mexico, New Jersey, Idaho, Kansas, and other states. The company’s business model is centered on majority-owned joint ventures (JVs) with academic medical centers, not-for-profit systems, and community physicians. Ardent acts as the primary operator within these partnerships, leveraging operational expertise alongside local brand recognition and clinical talent pools.[N1][S15]

This integrated platform spans hospitals, ambulatory care facilities, and physician practices unified under a consumer-centric approach aimed at optimizing patient outcomes and streamlining operations.[N1]

Historical Performance Trends

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 6.3 | 136 | 471 | 16 | +6.0% | -35.4% |

| 2024 | 6.0 | 210 | 315 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 454 | 10.5 |

| 2024 | 306 | 18.6 |

Source: SEC companyfacts cache [F1].

Revenue growth of approximately 6% in FY2025 was driven by expanded hospital volumes and increased penetration within its multi-state network.[F1] The steep net income decline reflects higher operating costs including restructuring charges (~$13 million), elevated depreciation ($155 million), legal expenses tied to ongoing litigation matters, and expenses related to the Epic IT system rollout.[S1]

Despite earnings pressure, operating cash flow improved sharply (+49%), underscoring robust underlying cash generation.[F1] Capital expenditures rose by over three-quarters year-over-year ($16 million vs $9 million), reflecting reinvestment in infrastructure and technology likely supporting modernization and capacity enhancements.[F1]

Debt Profile & Capital Structure

Ardent has proactively managed its debt profile through refinancing efforts aimed at reducing borrowing costs and extending maturities:

- The senior secured Term Loan B facility was refinanced in September 2025 reducing interest rate margins by an additional 50 basis points while extending maturity to September 2032.

- Quarterly principal repayments commence December 2025 at modest installment levels facilitating gradual deleveraging.[S4][S14]

- The company maintains a $325 million revolving credit facility split across two tranches supporting working capital needs; this facility matures in June 2029 with aligned covenants.[S19]

At December 31, 2025, Ardent held $709.6 million in cash complemented by available revolver capacity totaling approximately $1 billion in liquidity.[F1][S5] Net leverage stood conservatively near 0.8x (net debt/EBITDA), while lease-adjusted leverage was approximately 2.5x reflecting rent obligations under master leases common in healthcare real estate.[F1][S9]

Growth Outlook & Strategic Initiatives

Growth prospects are anchored in:

- Expanding service lines within existing markets leveraging deep JV partnerships focused on clinical quality improvement.

- Enhancing scale benefits from integrated provider networks that improve insurance contracting leverage.

- Pursuing accretive acquisitions targeting mid-sized urban markets complementary to its footprint for geographic synergy.[S15]

- Continuing investments in IT infrastructure like the Epic platform to boost clinical documentation quality and revenue cycle management despite upfront cost pressures.[S1]

Constraints include regulatory scrutiny over reimbursement models amid evolving government programs such as Medicare/Medicaid payment reforms,[N1] as well as labor cost inflation pressures from tight healthcare labor markets.

Recent Operational Developments & Milestones

Q4 FY2025 results released in March 2026 showed sustained revenue growth momentum but missed earnings expectations due largely to elevated restructuring charges tied to enterprise-wide cost optimization efforts.[N2][N3][N9] Management remains focused on clinical integration initiatives aimed at improving utilization metrics and length-of-stay efficiencies within JV hospitals.

Credit facility amendments have improved cost of capital metrics providing stable funding for future growth initiatives.[S14]

The company’s stock repurchase program authorizes up to $50 million with about $47 million remaining unused at year-end, signaling balanced capital return priorities alongside maintaining liquidity for strategic flexibility amid sector volatility.[S24]

Returns & Capital Allocation

Return on equity approximated 10.5% based on latest annual net income relative to shareholders’ equity nearing $1.29 billion at fiscal year-end.[F1] This reflects profitability pressures but suggests decent residual returns amid recent capex ramp-up.

Free cash flow (operating cash flow minus capex) was robust at roughly $454 million for FY2025,[F1] enabling comfortable coverage of debt service obligations while supporting reinvestment.

Distributions to noncontrolling interests form part of financing outflows; no regular dividends were declared during the period with capital allocation favoring share repurchases alongside debt management strategies.[S24]

Legal & Regulatory Risks

Operating within a highly regulated industry exposes Ardent to significant litigation risks:

- A securities class action filed January 2026 alleges accounting misstatements regarding receivables and insurance reserves for FY2024-FY2025 potentially inflating stock prices.

- A shareholder derivative lawsuit challenges alleged breaches of fiduciary duties linked to similar facts.

Management intends vigorous defense but acknowledges uncertainty around potential financial impacts pending judicial outcomes.[S12][S17][N9]

Additional compliance costs arise from public company status post-IPO along with cybersecurity risk mitigation efforts following prior incidents resolved through settlements without material liquidity impact but causing transient expense burdens.[S8][N1]

Conclusion & Key Considerations

Ardent Health has established a resilient regional healthcare platform driving top-line growth through well-orchestrated joint ventures blending acute care hospital capacity with ambulatory clinics efficiently run under centralized leadership models leveraging academic partnerships.

Profit margin compression from restructuring charges, legal exposures related to recent accounting disputes, rising input costs amid labor shortages, plus heightened regulatory complexity cloud near-term earnings visibility despite sustained strong cash flow generation.

Key factors for investors include:

- Progress on securities litigation resolution potentially affecting financial results or governance reforms.

- Stabilization or improvement in operating margins as Epic platform deployment matures delivering efficiencies.

- Market share dynamics across core geographies considering competitive pressures and policy changes.

- Refinancing flexibility relative to interest rate environments impacting debt servicing costs.

- Execution discipline balancing organic growth against acquisitions while preserving credit metrics.

With relatively low leverage and significant liquidity buffers,[F1] Ardent’s outlook balances operational opportunity against embedded execution risks typical of complex healthcare industry dynamics.

Disclaimer: This report is for informational purposes only without intention or implication of investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments