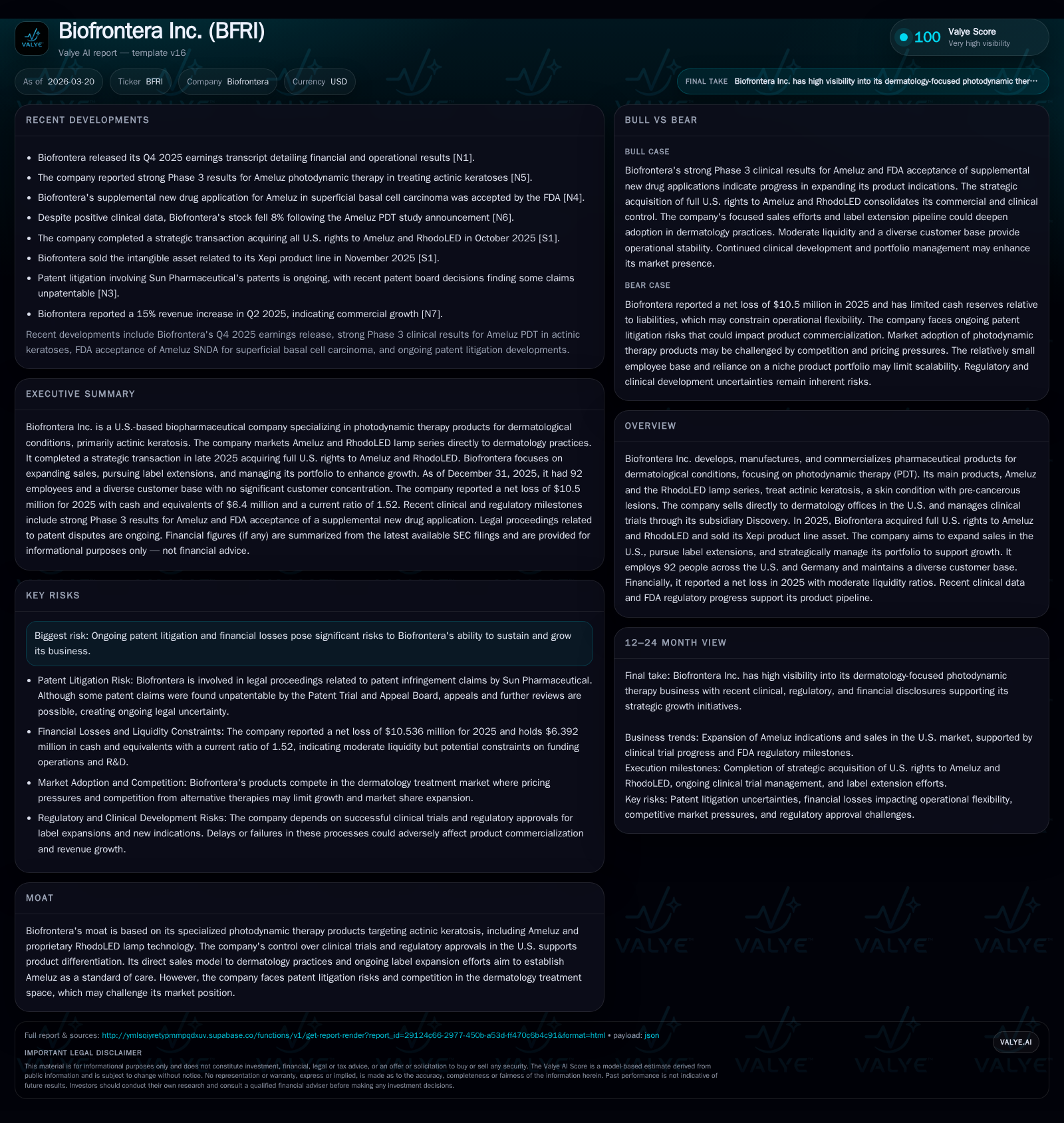

Biofrontera's Pursuit of Photodynamic Therapy Growth and Pipeline Expansion

A strategic milestone in U.S. commercialization rights reshapes Biofrontera’s growth trajectory alongside advancing clinical programs.

Biofrontera Inc. achieved a pivotal inflection point by acquiring full U.S. rights to its flagship products Ameluz and RhodoLED in late 2025, transitioning from a licensing-based revenue model to direct market control. This move aims to accelerate top-line growth and improve margin profiles amid ongoing patent litigation risks. Despite enduring net losses, which narrowed from over $22 million in 2023 to approximately $10.5 million in 2025 [F1], the company has demonstrated improved operating efficiency and clinical momentum with Phase 3 successes and FDA regulatory advancements supporting label expansion efforts. Capital deployment remains cautious with minimal capex and no shareholder returns as Biofrontera balances liquidity constraints against commercial scale-up investments.

Turning Point: Acquisition of U.S. Commercial Rights and Portfolio Rationalization

October 2025 marked a transformative milestone for Biofrontera Inc., as it completed the acquisition of all U.S. commercial rights to its core pharmaceutical assets — Ameluz® photodynamic therapy (PDT) and the proprietary RhodoLED lamp systems — via an asset purchase agreement with its former parent entity Biofrontera AG [N1, S1]. This Strategic Transaction consolidated the company's ability to sell directly to dermatology offices across the United States, replacing prior licensing arrangements that limited revenue capture and control over commercialization dynamics.

Complementing this portfolio rationalization, Biofrontera divested its Xepi product line asset in November 2025, signaling intent to sharpen focus on PDT-driven dermatological innovation [S1]. Concurrently, direct oversight of clinical trials was centralized under Discovery, Biofrontera’s wholly owned German subsidiary operating since mid-2024. This integration improves cost-efficient trial management and regulatory alignment critical for forthcoming label expansions.

The shift from a licensing-based model to full ownership presents strategic benefits: enhanced margin potential through elimination of royalty payments, streamlined clinical development processes under one corporate umbrella, and stronger alignment with the dermatology community through tailored commercial efforts.

Historical Financial Performance: From Progressive Losses to Operating Improvement

Financially, Biofrontera has endured persistent net losses characteristic of early-stage biopharmaceutical enterprises investing heavily in product launch infrastructure and R&D pipeline advancement. However, data reveal tangible signs of operating leverage.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -11 | -13 | -11 | 2000 | +40.7% |

| 2024 | -18 | -10 | -17 | 10000 | +11.8% |

| 2023 | -20 | -25 | -23 | 5000 | -3045.5% |

| 2022 | -1 | -16 | -19 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -13 | -100.5 |

| 2024 | -10 | -400.6 |

| 2023 | -25 | -420.0 |

| 2022 | -2.7 |

Source: SEC companyfacts cache [F1].

Despite top-line visibility gaps due to portfolio transitions during these years, Biofrontera almost halved its operating losses from $22.7 million in FY2023 to $11.3 million by FY2025 [F1]. Net income followed suit reflecting improvement though remaining negative at $10.5 million loss last fiscal year.

Operating cash flow remains negative (-$13.4 million in FY2025), suggesting ongoing investment into sales infrastructure and pipeline development; capex levels are nominal ($2K in FY2025), indicating a cautious posture favoring intangible asset development over fixed capital expansion.

Clinical Momentum: Phase 3 Successes and FDA Label Expansion Prospects

In early 2026 Biofrontera announced encouraging Phase 3 clinical trial data affirming Ameluz PDT’s efficacy for treatment of actinic keratosis across extremities beyond face/scalp indications—a clear extension of its therapeutic addressable market [N2]. Moreover, the FDA accepted a supplemental new drug application (SNDA) submitted by Biofrontera seeking an indication for superficial basal cell carcinoma (sBCC), widely considered a dermatologic malignancy where PDT could displace or complement surgical approaches [N6].

These developments reinforce prospective expansion opportunities via label extensions critical for driving broader clinical adoption and upselling combined therapy bundles incorporating the RhodoLED lamp system.

The company is also progressing trials targeting acne vulgaris therapy employing PDT technologies that could diversify revenues beyond non-melanoma skin cancers and pre-cancerous lesions [N4]. Direct trial oversight since mid-2024 has facilitated accelerated execution timelines enabling more responsive regulatory interactions.

Market Expansion Strategy: Dermatology Practice Penetration and Standard-of-Care Ambitions

Biofrontera operates a national direct-to-dermatology-office commercial team tasked with cultivating adoption of Ameluz PDT combined with RhodoLED lamps as the preferred standard of care for treating actinic keratosis lesions characterized as minimally to moderately thick on face and scalp regions [S1,S4]. The strategy includes:

- Focused customer acquisition campaigns reaching new dermatologists while deepening usage intensity with existing customers;

- Leveraging label expansions such as sBCC indications to broaden prescription scenarios;

- Educational efforts addressing reimbursement pathways for PDT devices and pharmaceuticals;

- Sustained engagement with Group Purchasing Organizations (GPOs) that influence pricing negotiations within consolidated purchasing frameworks.

Dermatological treatment adoption cycles typically exhibit inertia due to procedural shifts; however specialized device-drug combination therapies like Ameluz plus RhodoLED command clinician loyalty once incorporated into treatment algorithms.

Navigating Patent Litigation: Recent Board Decisions and Litigation Outlook

From mid-2024 Sun Pharmaceutical Industries initiated patent infringement allegations centered around two U.S. patents related to PDT formulations held by Biofrontera [S7,S15]. These legal proceedings have involved parallel litigation in federal court as well as administrative reviews at the U.S. Patent Trial and Appeal Board (PTAB).

On February 23, 2026 the PTAB issued a Final Written Decision invalidating all challenged claims of one patent (U.S. Patent No. 11,697,028), offering relief albeit partial given ongoing disputes over another patent which was denied PTAB review continuation [S7].

While this ruling mitigates risk for one enforcement front—potentially easing barriers for commercialization expansibility—it leaves residual uncertainty as unresolved patents continue as litigation focal points between parties potentially constraining longer-term competitive moat strength.

Legal experts familiar with PTAB procedure emphasize that appeals or Director-level petitions Sun might file could protract resolution timelines impacting licensing strategies or valuation premiums.

Capital Allocation Review: Balance Sheet Position, Cash Flow Trends, and Return Metrics

Biofrontera's financial stewardship reveals measured conservatism aligned with an early-commercial biopharma profile focused on extending runway amid cash burn risks from R&D intensiveness:

- The company held approximately $6.4 million cash and equivalents at end-FY2025 against current liabilities around $11.9 million yielding a current ratio near 1.52 — indicating reasonable near-term liquidity buffers without excess leverage [F1].

- No dividend distributions or share repurchase programs have been implemented recently consistent with strong reinvestment priorities into clinical development and sales expansion [S9–S16].

- Equity levels rose substantively from roughly $4.4 million at end-FY2024 to $10.48 million by end-FY2025 reflective partly of retained capital injections or earnings offsets despite aggregate losses noted previously [F1].

- Calculated annual return on equity remains deeply negative (~–100%) reflecting unprofitable status but trending toward narrowing deficits signifying improving operating discipline.

Capital expenditures remain minimal ($2K in FY2025) emphasizing expenditure discipline focused on intangible assets such as clinical programs rather than fixed assets.

Given sustained negative operating cash flow (-$13.36M post-capex in FY2025), internal funding capacity limits suggest future financing rounds or partnership monetizations may be necessary absent rapid revenue ramp ups.

Outlook and Key Catalysts: What to Watch in Product Adoption and Regulatory Progress

Looking forward into H2 2026 onward several pivotal elements warrant close observation informing Biofrontera's growth narrative:

- The impact of recent Phase 3 results translating into increased physician prescribing habits across expanded AK lesion locations – monitoring quarterly revenue segmentation will be instructive [N1,N2].

- FDA review timelines for the sBCC SNDA approval expected within standard regulatory windows; positive label expansions would likely catalyze further uptake alongside promotional efforts [N6].

- Progression of ongoing clinical trials targeting acne vulgaris PDT applications may unlock adjacent market verticals enhancing portfolio diversification ambitions.

- Litigation outcomes concerning pending patent enforcement actions; final resolutions here could recalibrate competitive dynamics materially adding either tailwind or headwind risk signals relative to intellectual property boundaries.

- Operational metrics such as incremental gross margin improvement attributable to direct commercialization after October 2025 rights acquisition will be key indicators measuring strategic transaction success.

These factors collectively frame an evolving landscape wherein Biofrontera balances momentum with execution risks typical within specialty biopharma sectors navigating phase gating milestones amidst constrained capital pools.

While still contending with net losses spanning consecutive years—albeit improving—Biofrontera’s sharpened focus on proprietary photodynamic therapy solutions supported by targeted U.S.-centric operations forms the core axis underpinning prospective value creation trajectories going forward.

This analysis is for informational purposes referencing publicly available filings and news; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments