BioCorRx Faces Liquidity Challenges While Advancing Naltrexone-Based Treatment Prospects

BioCorRx’s latest quarterly filing highlights acute liquidity constraints amidst ongoing clinical development efforts in addiction therapy.

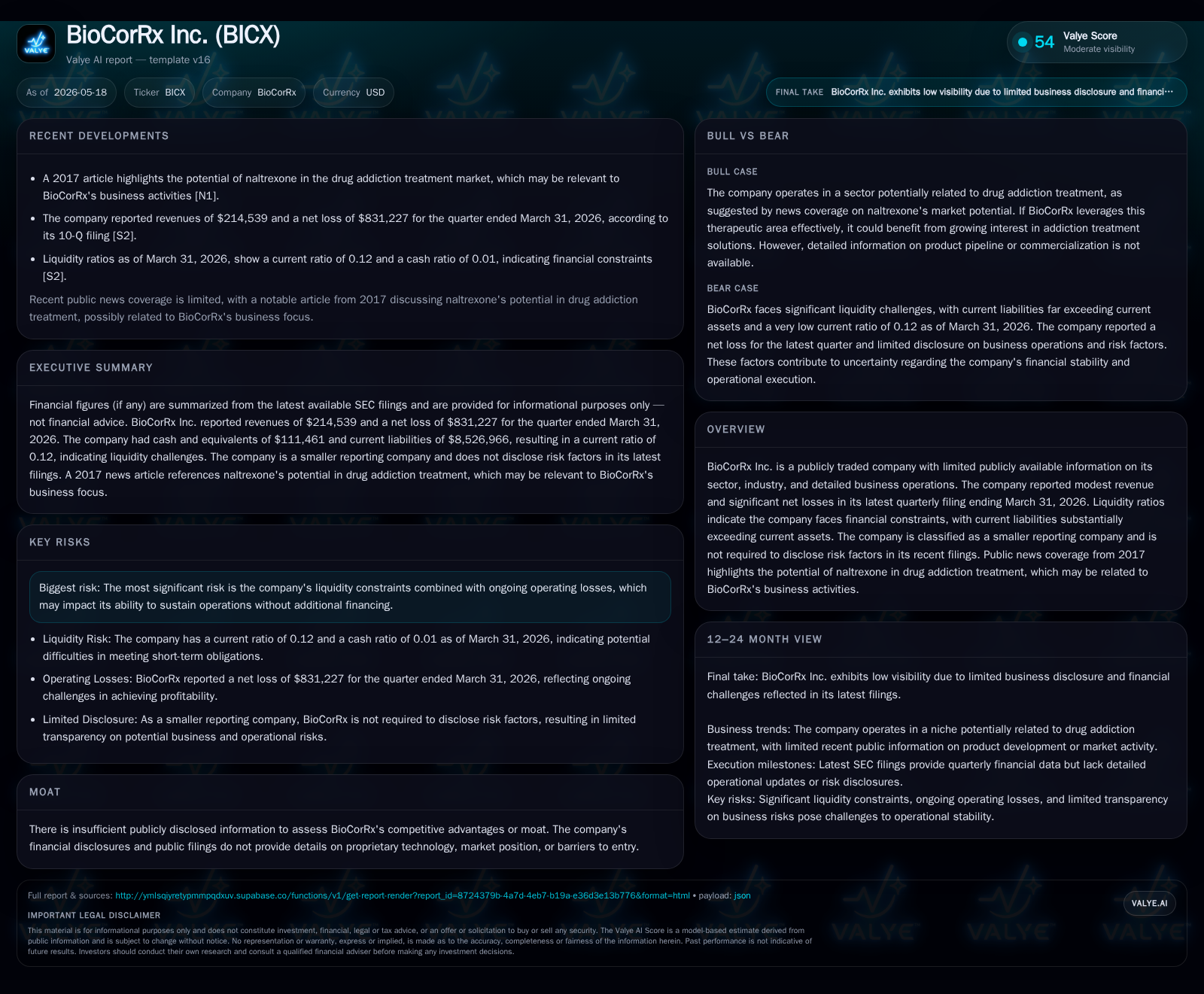

The company’s 10-Q for Q1 2026 reveals a dangerously low current ratio of 0.12, with current liabilities significantly surpassing current assets, underscoring severe financial strain. BioCorRx operates primarily in developing naltrexone formulations targeting substance abuse therapy, a niche with established clinical rationales but demanding regulatory and commercial hurdles. Recent share exchange agreements hint at management attempts to bolster shareholder alignment and future financing capacity. The path ahead hinges critically on clinical progress, market adoption, and resolving pressing liquidity risks.

Latest Quarterly Update Reflects Heightened Liquidity Pressure

BioCorRx Inc.’s most recent Form 10-Q filed on May 15, 2026, provides a sobering snapshot of its precarious financial position heading into the year’s second quarter [S2]. The company’s current assets stood at approximately $1.02 million against current liabilities of roughly $8.53 million, yielding an alarmingly low current ratio near 0.12 [F1]. This vast disparity signals acute liquidity pressure that threatens operational continuity absent additional capital inflows or drastic cost containment.

The operating disclosure does not report any new financing completed during the period nor clarifies imminent funding avenues, cementing an urgent need for the company to address its balance sheet vulnerabilities imminently. Such a fragile liquidity profile effectively constrains flexibility—raising questions about sustainable run-rate burn and short-term survival without swift intervention.

Business Model and Clinical Focus: Naltrexone and Addiction Therapy

BioCorRx’s core business is anchored in the development and commercialization of novel formulations of naltrexone, an opioid antagonist widely recognized within medical communities for its role in mitigating alcohol and opioid dependence [S1]. The company’s revenue model likely depends on licensing deals, product sales upon regulatory approval, or partnership arrangements tied closely to clinical milestones.

Naltrexone has a well-established mechanistic basis for addiction therapy but remains commercially sensitive due to patient compliance challenges and insurance reimbursement complexities. BioCorRx appears focused on enhancing delivery methods or formulation improvements to carve out differentiation within this somewhat mature segment.

Given this framework, BioCorRx’s revenues are presumably modest and highly sensitive to the outcome of regulatory approvals and clinical trial results. Product-market fit hinges on demonstrating superior efficacy or user experience advantages over incumbent treatments.

Competitive Environment and Industry Context in Addiction Treatment

The addiction therapy sector is populated by multiple players specializing in various pharmacological approaches—including injectable formulations like sustained-release naltrexone (Vivitrol) marketed by established pharmaceutical firms—and behavioral interventions supported by payers increasingly wary of costs [S1]. Although BioCorRx does not disclose direct competitor metrics, it operates within a structurally fragmented market where pricing power is limited.

Payer dynamics tend to favor established products with robust trial data and cost-effectiveness profiles; switching costs can be high for patients stabilized on incumbent therapies, creating barriers to rapid market penetration for newcomers. Furthermore, societal stigma around substance abuse disorders complicates patient recruitment for trials and broader adoption.

Thus, BioCorRx contends with entrenched commercial hurdles alongside standard pharmaceutical regulatory risks.

Growth Catalysts: Clinical Progress and Market Opportunities

Evidence from the April 2026 Form 8-K filing reveals that BioCorRx engaged in a stock exchange agreement involving key shareholders including C-suite executives [S3], which may be interpreted as an effort to solidify insider alignment ahead of anticipated strategic moves such as equity raises or partnership negotiations.

Clinically, growth is likely tethered to near-term milestones such as FDA trial clearances, topline efficacy data from ongoing studies, or incremental product development achievements—all prerequisites for augmenting revenue streams beyond nascent levels [S1][S3]

Successful demonstration of improved patient outcomes or delivery convenience could justify premium pricing or expanded payer coverage. Additionally, strategic collaborations or licensing deals remain plausible routes to scale given the company’s constrained capital resources.

Key Risks: Liquidity Constraints, Market Adoption Uncertainty, and Financing Needs

The most glaring risk centers on liquidity adequacy; the pronounced imbalance between current assets and liabilities denotes potential insolvency risk if fresh capital is not secured promptly [S2][F1]. Despite being classified as a smaller reporting company exempt from disclosing detailed risk factors under Regulation S-K [S2], implied financial fragility is unmistakable.

Operating losses at several million dollars annually dilute cash reserves rapidly—latest known operating income was negative approximately $4.8 million with net loss exceeding $3.4 million last recorded at fiscal year-end 2025 [F1]. This burn rate contrasts starkly against reported cash equivalents near only $111 thousand as of mid-2022 [F1], suggesting exponential depletion over recent quarters absent influxes.

Moreover, uncertainties surrounding commercial acceptance of naltrexone-based formulations limit predictability of revenue growth trajectories [S1]. Patient adherence issues, competitive intensity from branded injectables, reimbursement challenges by payers with strict formulary controls all heighten execution risks.

Finally, absence of any recent reported debt suggests no straightforward leverage strategy available; reliance on equity raises may face dilution resistance given financial history.

Near-Term Milestones and What to Monitor Next

Investors and analysts should closely track upcoming quarterly filings post-May 2026 quarter for evidence of any new financing activities or material changes addressing the liquidity crunch [S2]. Updates related to clinical trial progress—particularly FDA interactions or data releases—will remain pivotal gauges of commercial viability.

Given the stock exchange agreement disclosed in the April 8-K involving top executives transitioning shares back into the company [S3], subsequent announcements regarding equity management or shareholder structure adjustments will be critical signals toward solvency solutions.

Additionally, any public disclosure of partnerships partnering agreements or licensing contracts could provide important visibility into pathway-to-revenue prospects.

Financial Snapshot: Operating Losses Amid Cash Scarcity

Drawing from available financial metrics as of fiscal year-end December 31, 2025 and recent balance sheet snapshots:

- Revenue was reported at approximately $797K for calendar year 2025 [F1].

- Operating losses surpassed $4.8 million while net loss was over $3.4 million during that period [F1].

- Current assets stand around $1.02 million against multitudes higher current liabilities (approximately $8.53 million) resulting in a current ratio around 0.12 at March 31, 2026 [F1][S2].

Disclaimer: This analysis is based solely on publicly available information as of May 18, 2026. It does not constitute investment advice or research views regarding BioCorRx Inc. Securities mentioned herein should be evaluated with professional financial counsel considering specific individual circumstances.

Financial position in context

Current assets of $1020214 and current liabilities of $8.53 million imply a current ratio near 0.12x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments