Brookfield Infrastructure's Steady Revenues and Capital Strategy Support Long-Term Infrastructure Control

Brookfield Infrastructure Corporation leverages its global regulated assets and complex share structure to deliver stable cash flows amid capital-intensive operations.

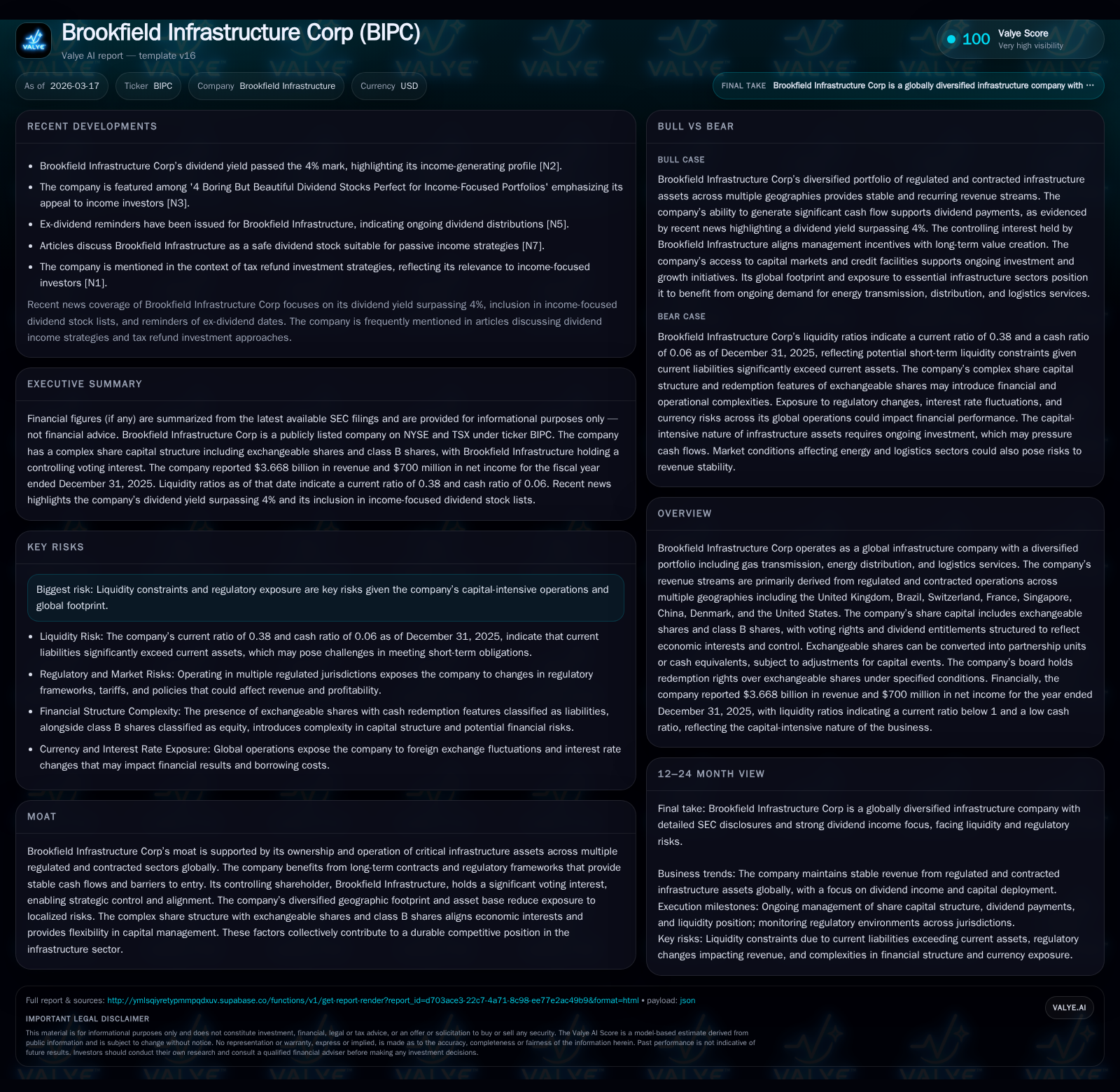

Brookfield Infrastructure Corp (BIPC) operates a diversified portfolio of critical infrastructure across regulated and contracted sectors worldwide, generating $3.67 billion in revenue and $700 million in net income in 2025 with minimal year-over-year revenue growth. Its moat stems from regulatory frameworks, long-term contracts, and control by Brookfield Infrastructure via a layered share class structure that balances economic interests and control. While cash flow generation supports a consistent dividend payout, liquidity constraints and regulatory exposures pose ongoing risks. The company's capital allocation includes an active normal course issuer bid for exchangeable shares but hasn't repurchased shares in 2025. Future growth hinges on expanding rate bases, tariff adjustments, and selective investment alongside managing leverage and geographic risks.

Overview

Brookfield Infrastructure Corp (BIPC), listed on the NYSE and TSX under "BIPC," is a global operator of critical infrastructure assets spanning regulated utilities (gas transmission, energy distribution) and logistics services[S1]. The company's portfolio spans multiple geographies — including the United Kingdom, Brazil, Switzerland, France, Singapore, China, Denmark, and the United States — strategically mitigating risks by geographic diversification[S13].

Its economic moat is anchored in regulatory protections and long-term contractual arrangements which secure steady cash flows despite macro volatility. Controlling shareholder Brookfield Infrastructure exercises substantial influence via a complex multi-class share structure: class B shares confer a 75% voting interest while exchangeable shares held by public investors are economically aligned via rights to distributions equivalent to partnership unit distributions[S1][S4]. Exchangeable shares may be converted one-for-one into partnership units or cash equivalents, subject to ownership caps limiting Brookfield's holdings to below 9.5%, ensuring flexibility while maintaining governance control[S12][S24].

Historical Performance

The company reported broadly flat revenues of $3.668 billion in fiscal year 2025 compared to $3.666 billion in fiscal year 2024—growth was effectively flat at approximately +0.1% year-over-year[F1]. This reflects a balance between inflation-driven tariff increases as well as capital commissioned into rate base against partial dispositions of stabilized assets at its global intermodal logistics operations[S13].

Notably, net income surged sharply to $700 million in 2025 from just $72 million in 2024, marking an increase exceeding 870%. This large change could result from operational improvements combined with remeasurements related to exchangeable shares classified as liabilities or other non-cash items linked to changes in unit prices or accounting treatment post-Arrangement consolidation completed in December 2024[F1][S16].

Equity declined modestly to $2.005 billion from $2.222 billion the prior year as the company reconciled financial liabilities arising from its exchangeable shares structure (classified as liabilities owing to their redemption features) offsetting some earnings gains[F1]. Cash flow generation remains pivotal given the capital-intensive nature of infrastructure assets.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 3.7 | 700 | +0.1% | +872.2% |

| 2024 | 3.7 | 72 | +46.5% | -88.1% |

| 2023 | 2.5 | 606 | +32.7% | -62.6% |

| 2022 | 1.9 | 1619 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 228 | 34.9 |

| 2024 | 213 | 3.2 |

| 2023 | 178 | 14.9 |

| 2022 | 158 | -448.5 |

Source: SEC companyfacts cache [F1].

Table: Brookfield Infrastructure Annual Financial Highlights (USD millions) [F1]

Future Growth Prospects

Growth drivers center on expanding infrastructure assets that benefit from long-term regulated or contracted cash flows:

- Inflation-linked tariff escalations underpin near-term revenue resilience especially within utilities businesses subject to regulatory rate reviews.

- Capital expenditures commissioned into rate base improve earnings quality over time.

- Geographic diversification mitigates concentrated regulatory or policy risk while offering multiple expansion opportunities across developed and emerging markets.

- The company's access to capital markets via revolving credit lines and ATM programs facilitate bolt-on acquisitions or reinvestment that sustain growth momentum[S9][S10].

Constraints include:

- Regulatory uncertainties inherent in utility sectors where rate resets or mandated policies may impact returns.

- Liquidity constraints arising from large non-recourse debt balances (~$13.2B total), requiring prudent leverage management especially amid rising interest rates[S5].

- The layered share structure caps Brookfield’s direct economic ownership due to exchange limits on class A.2 exchangeable shares maintaining an approximate maximum ownership near ~9.9% on an as-exchanged basis[S1].

- Partial disposition of assets can create revenue headwinds though freeing capital for redeployment elsewhere.

Forecasts / Milestones / Expectations

While formal guidance is not explicitly detailed within available documents, key developments warrant monitoring:

- Execution on the "at-the-market" program authorized through February 28, 2027 allowing issuance of up to $400 million exchangeable shares provides future funding optionality for share repurchases or acquisitions[S10].

- Outcomes of ongoing regulatory reviews across various jurisdictions impacting allowed returns will affect medium-term profitability.

- Progress in capital expenditure projects commissioning into the rate base will be critical for sustainable revenue growth.

- Any material changes relating to the conversion/redemption mechanics tied to exchangeable shares/share classes could impact shareholder value profiles.

In analysis terms, attention should focus on:

- Quarterly updates on discretionary capital deployment balancing distribution payouts versus reinvestment.

- Effects of commodity price volatility indirectly influencing gas transport volumes or logistics demand.

- Credit metrics given substantial non-recourse borrowings with staggered maturities through the next decade.

Returns / Capital Allocation

The company's return on equity approximates a healthy ~34.9% calculated by dividing net income ($700M) by equity ($2B) for fiscal year-end December 31, 2025[F1]. This elevated ROE partly reflects stable earnings on a relatively compact equity base post-liability reclassification effects.

Cash flow generation supports consistent dividend increases: dividends paid rose from $213 million in fiscal year ending December 31, 2024 to $228 million in fiscal year-end December 31, 2025 — aligning with stable operational cash flows from regulated assets[F1][S6]. Dividends on exchangeable shares are cumulative; unpaid amounts accrue without interest until paid ensuring prioritization over other classes like class B shares[S15][S20].

Capital allocation actions include:

- Initiation of an "at-the-market" equity offering program allowing flexible issuance of up to $400 million funded primarily through public market sales without dilutive block offerings[S10].

- Renewal of normal course issuer bids authorizing repurchase up to approximately 10% of total public float; however no repurchases executed during calendar year 2025 reflecting either market pricing conditions or strategic focus on internally funded growth investments[S8][S18].

- Maintain conservative leverage supported by committed revolving credit facilities totaling up to $150 million with Brookfield Infrastructure acting as lender/borrower alternating party providing liquidity backstops through March 2030 renewals[S9][S11].

Overall capital returns emphasize balancing steady distributions against reinvestment needs while preserving credit quality within a capital-intensive sector characterized by asset-heavy infrastructure investments.

Risks and Challenges

Liquidity management remains paramount given the scale of non-recourse borrowings ($13.17 billion at end-2025) despite staggered maturity profiles extending well into the next decade; interest rate variability could pressure financing costs[S3],[S5],[S7]. Regulatory exposures inherent in multinational utility operations introduce layers of complexity regarding allowed returns and compliance obligations across diverse jurisdictions primarily including mature Western Europe and emerging markets like Brazil[S13]. The complex share structure adds legal and operational intricacies affecting shareholder dynamics particularly around redemption rights and voting powers[S1],[S4],[S14]. These factors underscore the need for adept governance paired with proactive financial management.

Conclusion

Brookfield Infrastructure Corp exemplifies a globally diversified infrastructure platform benefiting from high barriers-to-entry imposed by regulation and contracts that yield predictable cash flows despite limited topline growth momentum recently demonstrated. Its controlling shareholder facilitates strategic governance while an intricate share class setup ensures alignment yet caps direct economic concentration. With robust dividend discipline supported by operational resilience alongside prudent leverage usage underscored by deep-pocketed support credit lines from Brookfield Infrastructure itself, BIPC presents a solid case study of balancing steady income generation with disciplined capital deployment amid global infrastructure sector realities.

This analysis is intended solely for informational purposes based on data available as of March 17, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments