Bakkt, Inc. Advances Strategic Platform Simplification and Regulatory Strength

Bakkt's 2025 corporate restructuring sharpens its focus on institutional digital asset infrastructure supported by a broad regulatory palette.

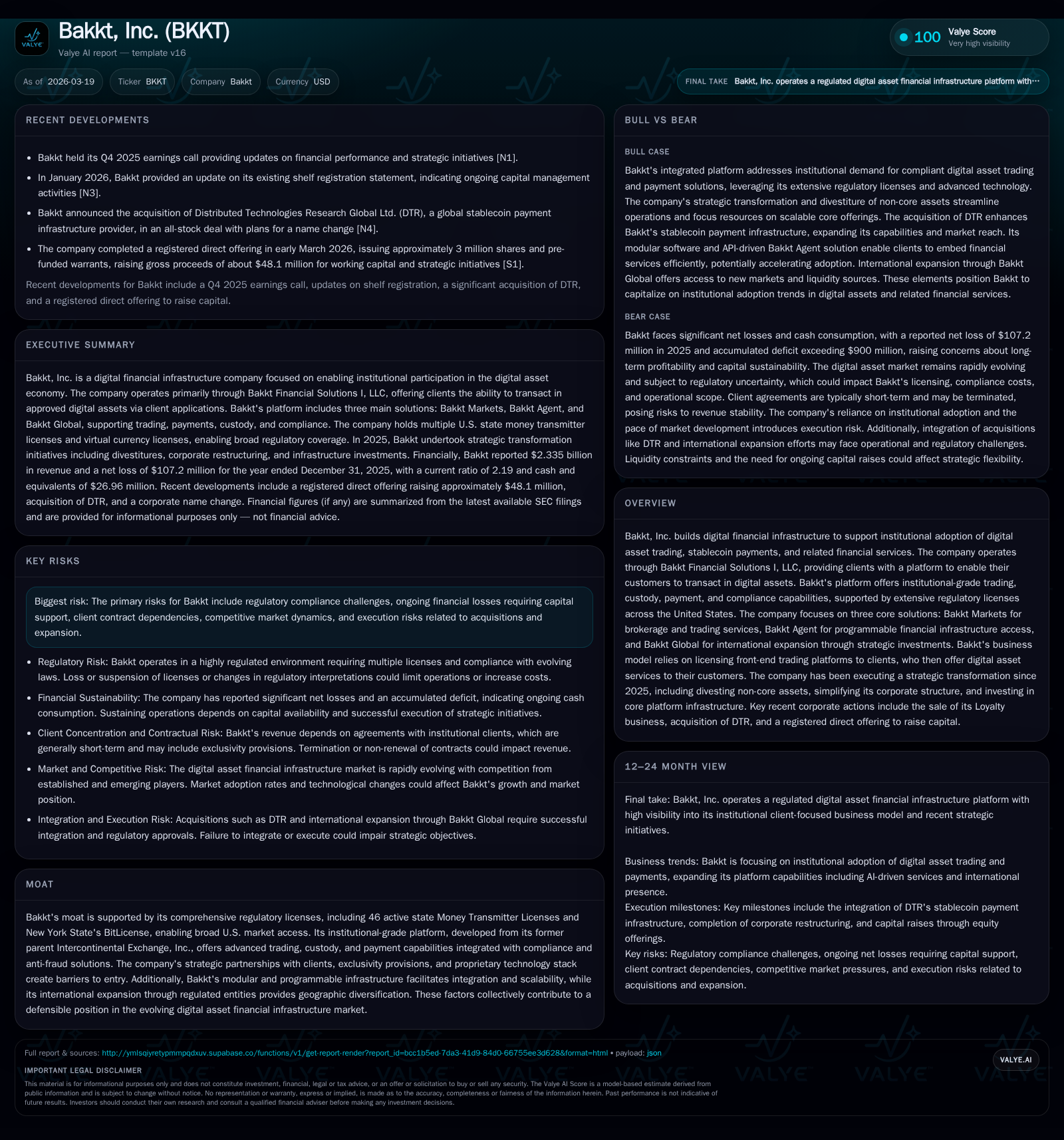

Bakkt completed a pivotal transformation by divesting its Loyalty Business in late 2025, focusing on a streamlined digital asset infrastructure platform servicing institutional clients. Despite persistent operating losses, the company leverages extensive U.S. regulatory licenses—including a BitLicense and 46 state Money Transmitter Licenses—to build a modular, client-centric fintech platform spanning trading, custody, payments, and compliance. Future growth hinges on client onboarding, AI-driven product innovations, and geographic expansion through Bakkt Global, while litigation related to the Loyalty Business sale poses short-term execution risks. Capital allocation reflects prudent liquidity management amid negative free cash flow dynamics.

From Legacy Operations to Streamlined Digital Assets Platform: Bakkt’s Strategic Transition

In fiscal year 2025, Bakkt undertook a strategic transformation culminating in the October sale of its Loyalty Business—a collection of Bridge2 Solutions entities—to Project Labrador Holdco, LLC. This divestiture finalized Bakkt's pivot from diversified fintech services toward a pure-play institutional digital asset infrastructure platform ([S1]). The Loyalty Business was significant historically but no longer aligned with the company's long-term focus on digital asset trading, custody, payments, and compliance.

Per U.S. GAAP, the Loyalty Business is classified as discontinued operations as of September 30, 2025. Post-divestiture, Bakkt concentrates operations primarily through Bakkt Financial Solutions I, LLC (BFS), simplifying its corporate structure and focusing capital on scaling its core digital asset platform.

Financial Performance Overview

Bakkt's financial results for FY2025 reflect intensified operating losses amid investments in technology and regulatory compliance. Operating income declined to -$147.8 million from -$92.9 million the prior year—a deterioration of about 59%—driven by increased spending on platform capabilities ([F1]). Net income losses widened to -$107.2 million versus -$46.7 million in FY2024.

Operating cash flow was negative $153.4 million in FY2025 compared to negative $21.2 million previously, indicating increased cash consumption linked to growth initiatives and working capital changes. Capital expenditures declined sharply by over 67% year-over-year, suggesting either completion of key investments or tighter expenditure discipline.

Liquidity remains sufficient with a current ratio around 2.19 at year-end 2025 ([F1]), though return on equity is negative approximately 95% due to sustained net losses relative to shareholders’ equity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -107 | -153 | -0.1 | -129.8% | |

| 2024 | -47 | -21 | -0.1 | 3 | +37.7% |

| 2023 | -75 | -61 | -0.2 | 9 | +87.1% |

| 2022 | -578 | -118 | -2.0 | 31 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -95.1 | ||

| 2024 | 3 | -24 | -137.7 |

| 2023 | 3 | -70 | -155.0 |

| 2022 | 3 | -148 | -600.5 |

Source: SEC companyfacts cache [F1].

Table summarizes Bakkt's recent financial trajectory highlighting increased losses alongside cash flow volatility.

Regulatory Licenses Establishing Market Access

Bakkt operates under an extensive regulatory framework granting broad U.S. market access for digital asset services. The company holds an active New York State Department of Financial Services "BitLicense" along with 46 state Money Transmitter Licenses ([S10], [S18]), enabling it to provide regulated digital asset trading, custody, stablecoin payments, and fiat on/off ramps.

This regulatory footprint supports institutional client confidence through rigorous KYC and AML protocols embedded within the platform’s compliance architecture.

Core Platform Solutions Driving Institutional Adoption

Bakkt’s offerings are organized into three main solutions:

- Bakkt Markets: A brokerage and trading platform offering institutions plug-and-play access to secure digital asset execution with integrated liquidity and custody.

- Bakkt Agent: A programmable API layer designed for institutions (and planned future direct-to-consumer use) providing automation for onboarding, virtual accounts, funding via fiat/stablecoins, cross-border payouts, identity verification workflows—all configurable via APIs to ease operational complexity ([S18], [S21]).

- Bakkt Global: Facilitates international expansion through investments in regulated entities across jurisdictions, enabling localized compliant digital asset infrastructure ([S21]).

Client agreements often include exclusivity provisions preventing referral of customers to competing platforms while allowing clients discretion over which digital assets are offered.

Outlook: Growth Drivers and Risks

In 2026 and beyond, Bakkt aims to grow adoption within existing clients while onboarding new financial institutions onto Markets and Agent solutions ([N1]). Key initiatives include expanding stablecoin payment rails integrated with AI-driven financial service modules to enhance programmability.

Internationally, growth depends on successful licensing across multiple jurisdictions via Bakkt Global—offering geographic diversification but requiring navigation of complex regulatory landscapes ([S6]).

Regulatory uncertainties remain a risk factor given evolving crypto classifications and AML rules that could increase compliance costs or limit product scope.

Macro conditions impacting the broader digital asset sector may also affect client activity levels.

Capital Allocation Balancing Growth Investment with Liquidity Preservation

As of December 31, 2025, Bakkt held approximately $27 million in cash and equivalents plus restricted cash (~$0.6 million) ([F1], [S13]). Mid-2025 equity offerings generated roughly $75 million gross proceeds supporting liquidity alongside convertible debenture issuances/redemptions optimizing capital structure ([S15]).

Capital expenditure reductions signal either completion of foundational technology investments or reined-in spending aligned with market conditions.

Modest share repurchases in prior years indicate capital discipline amid ongoing losses.

Funds are primarily allocated toward client acquisition efforts including marketing support for onboarding plus maintaining regulatory capital requirements essential for licensed operations across states ([S13]).

Litigation Related to Loyalty Business Sale Presents Execution Risk

Bakkt is engaged in litigation against Project Labrador Holdco ("Roman"), purchaser of the Loyalty Business, seeking approximately $10 million plus attorneys’ fees over alleged breaches of the purchase agreement post-sale ([S7], [S19]). Roman has filed counterclaims alleging entitlement to indemnification.

These legal proceedings are at preliminary stages; outcomes remain uncertain but could divert management attention and impose additional costs affecting near-term results.

Further shareholder derivative demands alleging fiduciary breaches add governance scrutiny though management contests these claims vigorously ([S4], [S11], [S19]).

Investors should consider these unresolved legal matters as contingent downside risks impacting predictability.

Key Metrics for Investors to Monitor Going Forward

Investors should track:

- Client onboarding rates within Markets and Agent platforms indicating product adoption;

- Progress on obtaining or renewing state virtual currency licenses reflecting regulatory environment shifts;

- Integration milestones for AI-driven programmable financial services enhancing platform capabilities;

- Developments in litigation related to Project Labrador Holdco dispute;

- Quarterly cash burn trends alongside capex spending informing liquidity outlook.

Stabilization of revenue streams post-Loyalty Business divestiture combined with measured geographic expansion will be prerequisites before potential profitability inflection points emerge given historical loss trends ([F1], [N1]).

Disclaimer: This overview is based solely on publicly filed SEC documents and verified news sources cited herein; it is not investment advice or a recommendation.

Comments