American Battery Materials Pursues Lithium and Magnesium Production Amid Exploration Stage Challenges

The company focuses on Direct Lithium Extraction from extensive Utah claims but faces significant operational and financial hurdles.

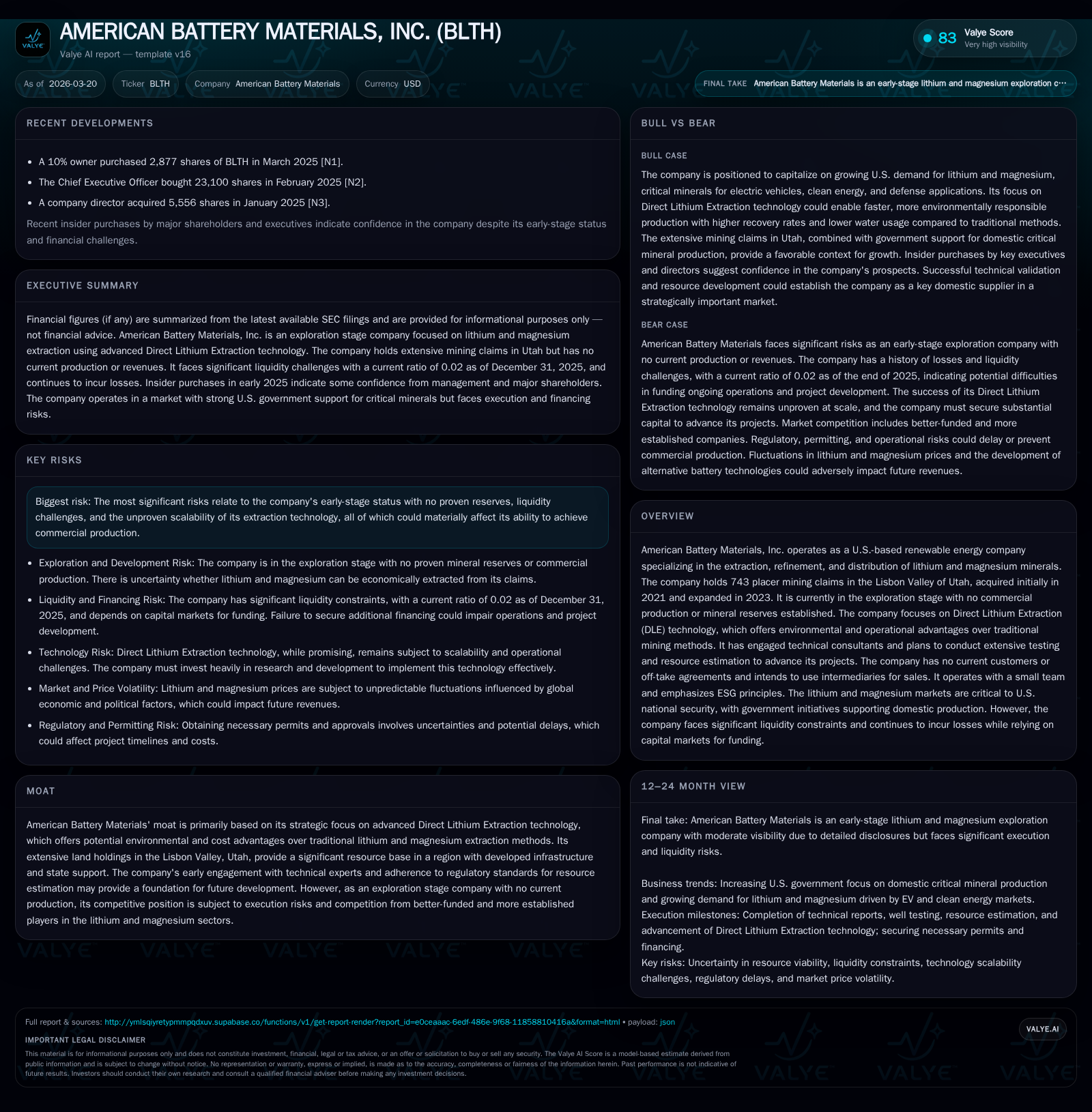

American Battery Materials, Inc. remains in the exploration phase without any commercial production or established mineral reserves. Its strategic emphasis on environmentally advanced Direct Lithium Extraction technology underpins ambitions to meet U.S. lithium and magnesium market demand. However, historical financials reveal ongoing losses, negligible revenue growth, and severe liquidity constraints, highlighting the critical need for successful resource delineation and capital infusion. Future growth hinges on drilling results, technological scalability, regulatory approvals, and access to financing amid a competitive and evolving industry landscape.

Overview and Historical Performance

American Battery Materials, Inc., trading as BLTH, operates as an early-stage U.S.-based renewable energy resource company focused on lithium and magnesium extraction via advanced brine technologies. Entering the lithium industry formally in November 2021 with the acquisition of initial federal mining claims in Utah’s Lisbon Valley [S19], the company expanded its holdings substantially to a total of 743 placer claims covering approximately 14,320 acres by mid-2023 [S19]. Prior to this focus, revenues were negligible and derived outside the lithium or magnesium domain.

Financially, the company exhibits a consistent lack of operating profitability throughout recent years. Revenue stood at $80,233 for fiscal year (FY) 2019—the latest available figure predating intensive lithium activities—and remained effectively flat from prior periods [F1]. The firm recorded escalating operating losses: -$1.13 million in FY 2022, increasing to -$2.45 million in FY 2023, then improving somewhat to -$1.57 million in FY 2024 before widening again to about -$1.86 million in FY 2025 [F1]. Net income followed a similar trajectory growing more negative from -$1.49 million in FY 2022 to roughly -$6.41 million in FY 2025—representing a near-49% year-over-year increase in net loss from FY 2024 [F1]. This performance reflects continuing expenditures on exploration activities without revenue offset.

Operating cash flow (CFO) remains negative though showed improvement from -$2.28 million in FY 2023 down to -$499K by FY 2025 [F1], indicating efforts to manage cash burn but no positive free cash generation yet. Cash and equivalents were a low $18,404 mid-2024 against current liabilities surpassing $10.6 million at end-2025—resulting in a dangerously weak current ratio near 0.02—signaling liquidity strain that necessitates near-term financing for continuation [F1][S13][S16]. Equity has declined further into negative territory at approximately -$10.3 million by December 2025 [F1], underscoring sustained accumulated deficits nearing $31 million [S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -6 | 0 | -2 | -48.8% |

| 2024 | -4 | -1 | -2 | -80.6% |

| 2023 | -2 | -2 | -2 | -60.4% |

| 2022 | -1 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 62.3 |

| 2024 | 63.3 |

| 2023 | 79.0 |

| 2022 | 114.3 |

Source: SEC companyfacts cache [F1].

Revenues noted only for FY2019; subsequent revenue absent due to exploration stage status.

Business Model and Growth Strategy

American Battery Materials aims to become a domestic producer of lithium and magnesium metals—critical inputs for electric vehicle batteries, clean energy storage systems, aerospace alloys, defense applications, and lightweight automotive components [S19][S26]. The U.S currently imports its entire primary magnesium supply following shutdowns of domestic facilities amid cost pressures [S19]. Therefore, American Battery Materials positions itself alongside a few emerging companies attempting to restart U.S.-based primary magnesium production with advanced extraction technologies [S19].

Central to their approach is Direct Lithium Extraction (DLE) technology whereby lithium-rich brine is pumped from underground aquifers into surface facilities where lithium is selectively adsorbed or filtered out using ion-exchange resins or membrane systems before reinjection of depleted brine back underground [S23][S26]. This contrasts with traditional hard-rock mining or solar evaporation ponds by offering superior lithium recovery rates (above 90%), greatly reduced water consumption, lower environmental footprint with zero tailings disposal needs (closed-loop system), and faster production timelines measured in months instead of years [S23]. Importantly for magnesium supply chains, DLE also allows simultaneous co-production of magnesium with potential cost benefits.

Their significant land position across the Lisbon Valley project—over 14,000 acres under federal claims—offers a strategic base supported by established infrastructure within Utah's mining-friendly regulatory environment [S19][S26]. The company has engaged qualified external consultants such as RESPEC LLC for geotechnical modeling and resource evaluation supporting forthcoming exploration wells and data refinement projects [S23][S26]. Efforts also include developing proprietary subsurface models informed by seismic surveys planned post-drilling appraisal wells [S10][S26].

Development Milestones and Operational Outlook

Actual commercial production remains contingent upon several major milestones: drilling two appraisal wells to confirm reservoir properties such as porosity/permeability and mineral concentrations; successful testing of extractive technology efficacy at scale; receipt of all necessary governmental permits permitting mining operations; securing long-term financing; negotiating customer contracts—currently nonexistent—and building extraction/refinement capacity [S10][S4][S14].

Given no proven mineral reserves have yet been certified per SEC Regulation S-K Item 1300 definitions—with historical brine data suggestive but inconclusive—the company's stage is strictly exploratory without revenue generation from lithium or magnesium sales as yet [S1][S10][F1].

Revenue generation depends largely on external financing raising funds for pilot programs followed by construction timeline adherence without cost overruns or regulatory roadblocks which are acknowledged risks [S20][S22][S24]. Any delay or failure could severely impair potential profitability.

American Battery Materials plans to sell its minerals through intermediaries rather than direct sales forces initially due to lacking commercial marketing capabilities today [S4]. The sector remains highly competitive with multiple better-capitalized entrants developing alternative DLE technologies or targeting other geographic regions globally [S4].

Environmental regulations represent both opportunities—with DLE touted as environmentally preferable—and challenges given stringent air/water quality standards plus remediation expectations imposed on mining firms today especially in sensitive communities [S5][S18]. The company stresses commitment to ESG principles including local community hiring and diversity policies even during initial staff expansion stages where fewer than five full-time employees serve underlying project functions currently [S14].

Financial Overview: Returns and Capital Allocation

American Battery Materials’ financial history reflects typical early-stage exploration risk profiles characterized by consistent net losses driven by R&D expenditures without producing operating income or free cash flow positivity [F1]. Latest year losses expanded considerably despite some improvement from prior years’ operating losses:

- Operating income declined further by approximately 18.8% year-over-year vs FY24 at roughly -$1.86M for FY25;

- Net losses ballooned almost +48.8% YoY reaching approx -$6.41M by end-2025;

- Operating cash flow adverse but improving at around -$499K (CFO), yielding an approximate negative free cash flow around -$513K when subtracting limited historical capex;

- Equity continues deepening into negative territory at roughly -$10.3M reflecting continued accumulated deficit expansion;

- Current assets around $190K contrast starkly against over $10M current liabilities underscoring short term liquidity vulnerability requiring additional equity/debt financing imminently.

Return on equity is not meaningful due to negative shareholders' equity position stemming from accumulated operating deficits incurred since entry into lithium business lines.

No dividends have been declared or are expected given current financial constraints and priority focus on reinvestment into development efforts rather than shareholder distributions [S7]. Likewise, share repurchases are non-existent given issuer status.

Substantial dilution risk exists if future capital needs are funded through equity issuance given limited internal cash generation capacity requiring frequent access to capital markets for sustainability [S16][S21]. Such financings could adversely affect investor ownership percentage absent material project value realization.

Risks Summary

Key risks revolve around technical feasibility—the scalability of DLE remains nascent despite pilot success stories elsewhere—with uncertainties around well productivity profiles, brine chemistry variability influencing extraction efficiency, total recoverable mineral quantities unconfirmed by proven reserves classification standards; the ability to obtain timely permits under increasingly complex environmental regulations; persistent market price volatility affecting both lithium and magnesium commodities internationally; fierce competition from larger producers domestically and abroad; potential delays escalating costs beyond budgets causing adverse economic outcomes; eventual dependency on raising substantial fresh capital amid tightening public market conditions affecting speculative mining ventures; management concentration risk concentrated among insiders with nearly half ownership essentially granting governance control; the limited operating history compounding forecasting difficulty altogether heightening investment risk profiles materially compared with more mature peers [S1][S3][S15][F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments