Bumble Inc.'s Quest for Sustainable Growth and Financial Stability

Bumble leverages its women-centric brand and AI-driven innovation to fuel growth while grappling with rising losses and leverage constraints.

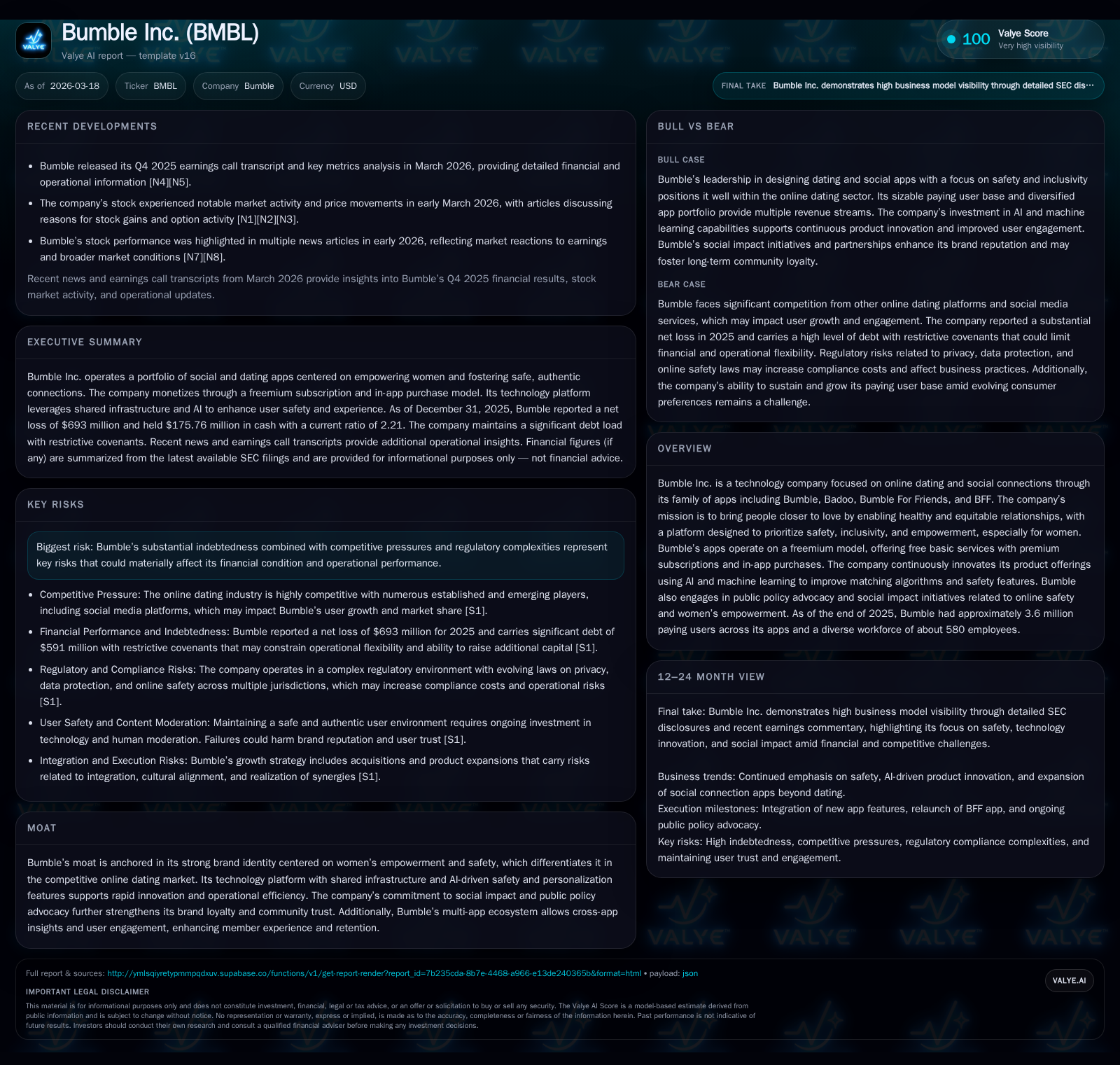

Bumble Inc. builds on a distinct brand ethos focused on women's empowerment and safety in online dating, supported by a growing base of 3.6 million paying users across multiple apps. Despite this user growth and expanding operating cash flows, the company has seen its profitability deteriorate sharply from modest gains in 2023 to large operating and net income losses by 2025, reflecting substantial investments and market pressures. High indebtedness nearing $588 million, coupled with restrictive credit covenants, limits financial flexibility amid competitive and regulatory challenges. Going forward, Bumble’s growth hinges on successful AI-driven product innovation, member engagement, and navigating evolving digital safety regulations, while managing capital allocation carefully through buybacks rather than dividends.

From Startup to Scale Player: Historical Growth Drivers

Bumble Inc., founded on a mission to bring people closer to love through equitable relationships with a focus on women's empowerment, has evolved into a prominent player in online dating technology. Its revenue model primarily relies on freemium monetization — giving free access to basic services but converting a subset of users into paying subscribers through premium subscriptions and in-app purchases.

Between FY2022 and FY2025, Bumble's financial performance witnessed significant volatility. Operating income swung from a loss of approximately $103 million in 2022 to a profit of about $53 million in 2023, only to plunge sharply into a substantial operating loss near $806 million by the end of 2025 [F1]. Net income followed a similar trajectory, turning less negative from -$79.7 million in 2022 to nearly breakeven in 2023 (-$4.2 million), then deteriorating drastically to -$693 million by FY2025 [F1]. This shift indicates intensified investments or market challenges despite notable user growth.

Operating cash flow (CFO), however, tells a somewhat different story: steadily increasing from $133 million in 2022 to $182 million in 2023, moderating slightly before doubling to $250 million by the end of 2025 [F1]. This divergence between improving operating cash flow and worsening profitability underscores Bumble’s cash-generation capabilities despite escalating costs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -693 | 250 | -806 | -24.4% |

| 2024 | -557 | 123 | -700 | -13121.2% |

| 2023 | -4 | 182 | 53 | +94.7% |

| 2022 | -80 | 133 | -103 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 29 | -121.6 |

| 2024 | 192 | -67.6 |

| 2023 | 0 | -0.3 |

| 2022 | 0 | -4.9 |

Source: SEC companyfacts cache [F1].

Table: Bumble Inc.: Historical Financial Summary (FY2022-FY2025) [F1]

The equity base has contracted significantly post-2023, dropping from over $1.6 billion down to roughly $570 million at fiscal year-end 2025 [F1], implying substantial accumulated losses impacted shareholders' equity.

This historical context frames Bumble’s pathway from early growth success into an investment-heavy phase characterized by deep operating losses concurrent with expanding paying user counts — around 3.6 million as of December 31, 2025 — across its apps [S1].

The Brand and Tech Edge: Differentiation Through Women-Centric Design and AI

Bumble’s defining competitive edge lies in its foundational mission: designing online connection platforms with women at the center to foster safer and healthier interactions [S1]. This focus manifests both technically—with proprietary safety features—and culturally—via brand messaging emphasizing empowerment and inclusivity.

The company's ecosystem comprises multiple apps including Bumble app (the flagship), Badoo (global mainstream appeal particularly outside North America), Bumble For Friends (rebranded as BFF), all employing a freemium monetization model that converts engagement into paying subscribers [S1]. Notably, Bumble app led with approximately 2.4 million paying users domestically in mature markets like the U.S., U.K., Australia, Canada by end-2025; Badoo contributed about 1.2 million global paying users mostly across Europe and Latin America segments [S1].

Technological enhancements harness artificial intelligence and machine learning chiefly for refining matching algorithms and proactively empowering user safety via AI-driven content moderation or detection systems [N1]. Such innovations align with sector patterns where AI integration is becoming table stakes for personalization at scale but also serve as barriers given the specialized expertise required.

Additionally, Bumble extends its brand differentiation through substantive public policy advocacy targeting industry standards around online safety—a commitment that builds community trust and wider social impact currency beyond mere feature sets [S1]. Partnerships like multi-year alignments with organizations such as the Women's National Basketball Association amplify marketing penetration tethered firmly to brand values.

These strategic pillars underpin Bumble's moat encompassing brand loyalty centered on inclusivity & safety plus multi-platform synergies enabling cross-pollination of insights—crucial for maintaining engagement amidst an intensely competitive environment characterized by low switching costs among dating platforms [S19].

Financial Headwinds: Deepening Operating Losses Despite User Growth

Perhaps most striking is the paradoxical financial profile emerging since the profitable peak in calendar year 2023: despite steadily growing paid membership numbers reaching millions by end-2025 [S1], Bumble has seen operating income plunge by approximately $856 million (a ~15% decrease year-over-year) culminating in an operating loss of over $805 million [F1]. Net income worsened by nearly a quarter over prior year’s loss margin reaching close to -$693 million [F1].

On closer inspection, this deteriorating profitability contrasts with robust operating cash flow growth (+102.8% YoY increase to $250 million), suggesting sizable non-cash charges or elevated reinvestment outlays limiting bottom-line earnings but leaving operational liquidity intact [F1][N1]. The company attributes these trends partly to accelerated investment into product innovation—including new AI features—and expanded marketing efforts aimed at bolstering member acquisition & engagement amidst intensifying competition [N1].

Return on equity stands deeply negative at approximately -121.6%, reflecting how cumulative net losses have eroded underlying shareholder value given shrinking equity balances from over $1.6 billion down to roughly half-billion levels between FY23-FY25 (see table above) [F1]. This signals that current profitability challenges heavily outweigh assets supporting equity claims.

While investing for longer-term growth plausibly explains some cost inflation, such magnitude demands ongoing operational discipline coupled with effective monetization enhancements lest cash burn exacerbate financing risks tied to existing indebtedness.

Capital Structure Under Pressure: High Debt and Restrictive Covenants

Bumble carries about $588 million in outstanding term loans due January 29, 2027—a critical near-term maturity that shapes liquidity strategy going forward [S4][S5]. Interest on these loans is variable rate exposing debt service costs to rising rate environments absent effective hedging programs [S5].

Credit agreements impose stringent restrictions limiting activities such as incurring further debt beyond thresholds or making dividend payments absent covenant compliance [S7]. One key ratio is the "first lien net leverage ratio" capped at approximately 5.75x EBITDA equivalent terms subject to quarterly calculation; failure risks default triggering accelerated repayment obligations or foreclosure proceedings against collateral pledged for credit facilities [S7][S22].

High leverage also narrows negotiating bandwidth for pursuing M&A or opportunistic investments vital for tech companies facing rapid innovation cycles where competitor dynamism includes AI deployment enhancements or aggressive customer acquisition campaigns [S4][S25].

Bumble operates predominantly as a holding company dependent on subsidiaries’ distributions for servicing corporate-level obligations which introduces structural liquidity dependency risks should subsidiaries restrict funds due legal capital maintenance requirements or local regulatory limits [S4][S7]. Additionally, restrictive covenants curtail ability to pursue dividends broadly; historically no dividends have been declared likely reflecting these conditions as well as prioritizing capital reinvestment or deleveraging uses [S17][S20].

Balancing debt servicing needs against maintaining investment tempo constitutes a fundamental tension point threatening operational flexibility within an increasingly competitive digital dating space.

Future Opportunities and Pitfalls: Market Positioning and Expansion Challenges

Looking ahead, Bumble's prospects ride on successfully navigating evolving member behaviors especially among younger demographics like Gen Z who exhibit distinct connection modalities and consumption patterns potentially divergent from traditional dating app usage norms [S1][N1][S19]. Retention strategies must adapt accordingly through innovative feature rollouts leveraging AI personalization without alienating core audiences.

Regulatory landscapes loom large as new laws concerning data privacy, online safety including protection of minors under frameworks like GDPR/UK GDPR or emerging U.S state mandates introduce compliance complexity that could inflate governance costs or constrain product functionality if not managed adeptly [S6][S9][S14][S18][S26][S27]. Failure risks reputational damage adversely impacting member sentiment essential for subscription revenue stability.

Geographically, Bumble pursues international expansion balancing opportunity against logistic hurdles tied to localized marketing effectiveness, cultural sensibilities influencing app adoption rates, telecom infrastructure disparities affecting connectivity patterns especially where Wi-Fi reliance dominates over cellular penetration—the latter critical for persistent app use throughout daily routines [S19]. Such nuances demand targeted regional strategies rather than broad strokes attempts.

Competitive threats remain pronounced given low switching costs for consumers amid proliferating dating platforms innovating aggressively around AI matchmaking capabilities or alternative social connection paradigms necessitating continuous product evolution from Bumble's development teams supported centrally but expectedly austere due to financial constraints discussed prior.

Investor Outlook: What to Watch in Upcoming Quarters

Although explicit forward-looking guidance remains limited publicly at this time [N1], investors should monitor several key performance indicators indicative of trajectory:

- Paying user monthly growth rates across core apps signaling effectiveness of acquisition tactics;

- Churn rates measuring member retention continuity critical under freemium economics;

- Adoption levels of newly launched AI-powered features potentially driving higher conversion;

- Developments regarding refinancing or extending debt maturities given proximity to Jan ‘27 deadlines;

- Quarterly operating cash flow trends offering real-time views into cash resilience amid ongoing losses. Market analysts recently upgraded outlooks recognizing recovery opportunities provided operational execution aligns with strategic priorities partially buoyed by positive fourth-quarter earnings surprises reported early March ‘26 [N5][N1], yet skepticism remains prudent given persistent loss pressures juxtaposed with concentrated ownership structure controlling majority voting power possibly limiting market participant influence on governance decisions [S22].[N4]

Linking Capital Allocation to Long-Term Returns: Share Buybacks without Dividends

On capital returns front, Bumble has refrained from dividend payments historically consistent with restrictive covenants limiting such disbursements due high indebtedness levels alongside Delaware law restrictions on subsidiary distributions when liabilities exceed asset values net face amount constraints [S17][S20]. Instead the company has favored repurchasing shares—buybacks totaled approximately $28.7 million during FY25 compared with $192 million in FY24 indicating reduction due likely liquidity prudence amid larger operating deficits but still signaling confidence or defensive capital deployment strategy given lack of dividends available for yield-focused investors within their Class A common stock structure overseen by majority principal shareholders controlling ~86% voting power as of early CY26 per filings marking governance implications worth attention when assessing returns sustainability dynamics [F1][S22].[N9]

Negative ROE near -122% continues weighing on shareholder value expansion prospects albeit partially offset through active buyback programs underpinned by positive operating cash flows sustaining repurchase activity despite accounting losses referenced earlier illustrating complex capital management balancing act under financial strain accompanied by high market expectations around product innovation progress.[F1][S17]

This analysis synthesizes known data points up through March '26 filings without speculating beyond provided sources. It highlights tangible tensions between Bumble's differentiated brand-driven growth ambitions buttressed by AI-led innovation against intensified financial headwinds wrought largely by escalating operational expenses paired with leverage burdens constraining flexibility needed in dynamic online dating markets replete with evolving regulatory demands and consumer preferences shifts.

Investors should contextualize historical performance within macro digital service ecosystems while vigilantly monitoring upcoming quarterly disclosures addressing operational metrics central to validating sustainable path forward absent disruptive refinancing challenges or unanticipated regulatory developments.

Disclaimer: This is an informational memorandum intended solely for analytical purposes based on current available filings and news reports without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments