BioRegenx’s AI-Driven Health Tech Expansion Confronts Liquidity and Scale Limitations

The company’s diversified health tech platform including AI-powered diagnostics and supplements grows revenues but losses and liquidity challenges persist.

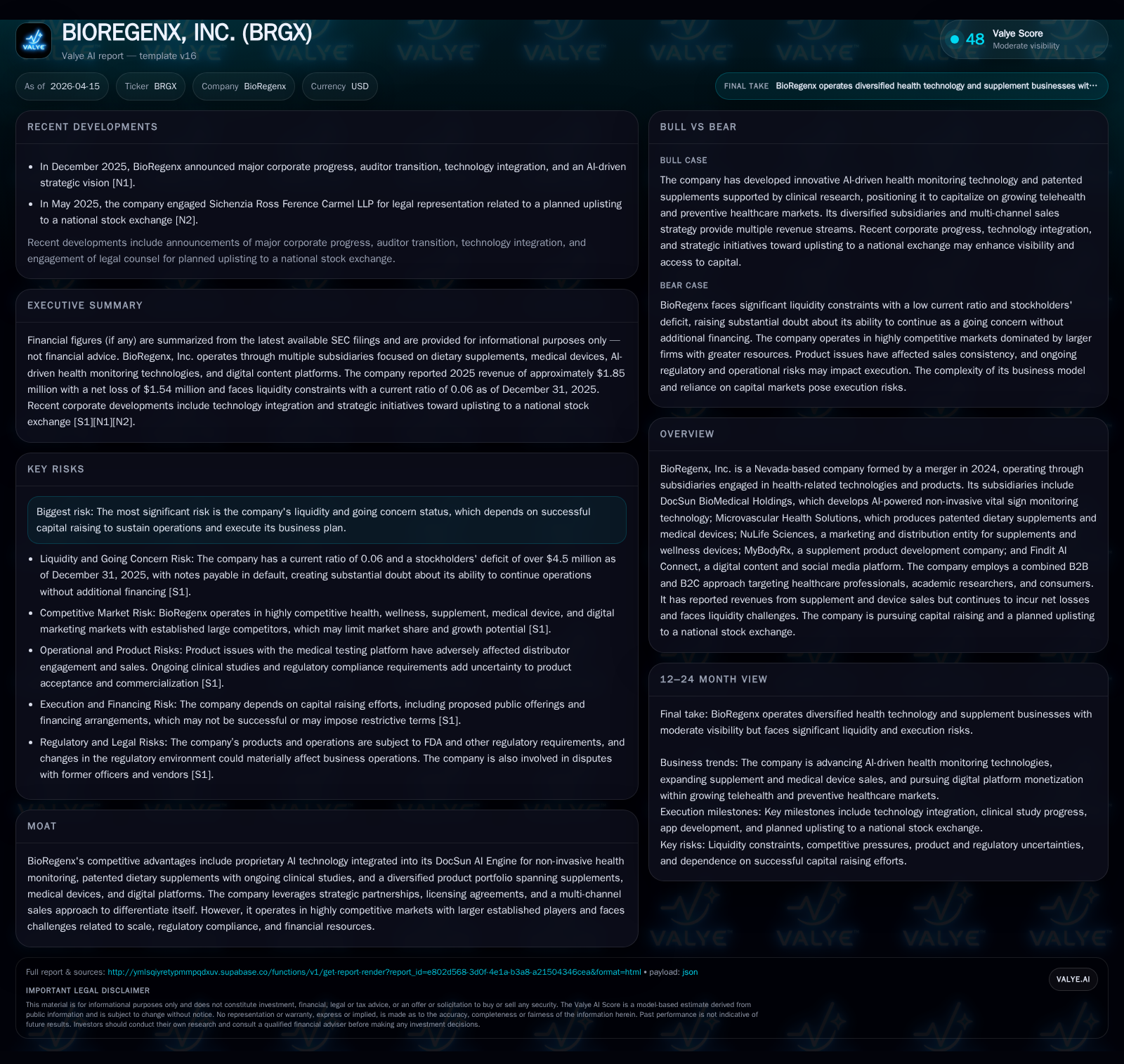

BioRegenx, Inc. operates an integrated portfolio of health-related technologies from AI-driven non-invasive monitoring to patented supplements, formed by mergers culminating in 2024. While revenues reached $1.85 million in 2025, a 21% decline from 2024, operational losses shrank markedly to $1.54 million due to lower impairments and cost reductions. The company deploys a combined B2B and B2C approach targeting healthcare providers, researchers, and consumers but faces intense competition and regulatory complexity. Liquidity constraints remain critical, with tangible doubt about continuing as a going concern without substantial financing or uplisting to a national exchange.

Company Overview

BioRegenx, Inc., a Nevada-based entity formed through a March 2024 merger of Findit, Inc., operates subsidiaries active in health technology sectors including AI-enabled non-invasive vital sign monitoring (DocSun BioMedical Holdings), patented dietary supplements plus GlycoCheck microvascular diagnostic systems (Microvascular Health Solutions), marketing/distribution (NuLife Sciences), supplement product development (MyBodyRx), and digital content distribution (Findit AI Connect) [S1], [S3], [S23]. This multi-channel portfolio combines B2B sales targeting healthcare providers and academic researchers with direct-to-consumer engagement via app stores and online platforms [S3], [S4].

Historical Financial Performance

BioRegenx's revenue declined from $2.34 million in FY2024 to approximately $1.85 million in FY2025—a decrease of about 20.8%—due principally to product issues affecting distributor engagement and a strategic shift toward online marketplace distribution [F1], [S17]. Operating expenses dramatically decreased primarily because impairment charges fell from $16.2 million in FY2024 to $725k in FY2025 alongside lower stock-based compensation [F1], [S15]. As a result, net loss narrowed substantially from over $23 million in FY2024 to approximately $1.54 million in FY2025 [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -2 | 38972 | -1 | -20.8% | +93.3% |

| 2024 | 2 | -23 | -324148 | -23 | +10420.6% | -3936.3% |

| 2023 | 0 | -1 | -13347 | 0 | -47.2% | -629.4% |

| 2022 | 0 | 0 | -64652 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 29915 | 34.0 |

| 2024 | -513538 | 682.2 |

| 2023 | 257.3 | |

| 2022 | 38.9 |

Source: SEC companyfacts cache [F1].

Note: Operating income abbreviated OpInc; CFO = Cash Flow from Operations.

Despite improved profitability metrics for FY2025 largely attributable to reduced impairment charges rather than operational scale benefits alone [F1], sustained negative earnings illustrate ongoing challenges scaling the business sustainably.

Business Model and Growth Prospects

BioRegenx leverages its proprietary DocSun AI Engine which integrates ballistocardiography with photoplethysmography and optical coherence tomography coupled with artificial intelligence algorithms for contactless vital sign monitoring applicable across healthcare facilities as well as security sectors requiring biometric liveness detection [S26], [S27].

The company markets the GlycoCheck® microvascular diagnostic system sold primarily to research institutions and medical practices with pricing between $14.9k-$32k per package plus recurring software subscription revenue models [S23]. Proprietary supplements under MyBodyRx® such as Endocalyx Pro® target preventive health oriented at wellness practitioners and wholesalers [S23].

NuLife Sciences manages distribution of multiple wellness products including pulsed electromagnetic field devices alongside hydrogen water products aiming for an integrated wellness offering supported by fitness apps incorporating genetics/epigenetics testing tools under development [S23].

Marketing strategies include direct selling to practitioners and academic researchers validating clinical effectiveness through ongoing studies plus influencer affiliate programs expanding digitally derived channel reach both B2B and B2C via app stores [S3]. Subscription pricing models for GlycoCheck software services along with bundled supplement offerings seek recurring revenue stability while premium positioning differentiates the DocSun AI Engine from commoditized wearables common within telehealth services growing at projected annual rates north of 20% globally into the next decade [S19].

Growth is challenged by intense competition from established multinational medical device companies with deeper resources; fragmented but crowded nutritional supplement markets; dominant technology firms like Alphabet leveraging search platform dominance competing against Findit AI Connect's digital media efforts; plus evolving telehealth startups employing sophisticated AI diagnostics that may eclipse smaller players' propositions [S8], [S10]. Regulatory compliance costs coupled with clinical trial uncertainties further amplify operational risks given financial constraints [S27].

Forecasts and Milestones

Management has not provided explicit numeric guidance but operational milestones include:

- Completion of clinical trials on Endocalyx Pro® supplementation efficacy supporting product claims;

- Planned uplisting through reverse share splits (up to one-for-twenty-five) aimed at enhancing institutional investor appeal;

- Securing new equity or debt financing remains critical given ongoing liquidity constraints;

- Expanding GlycoCheck system placements alongside increasing recurring software subscriptions;

- Enhancing consumer engagement via app downloads and social media-driven awareness campaigns.

Capital raise efforts led exclusively by Maxim Group LLC extend through mid-2026; successful funding will be essential for operational sustainability [S14], [S20].

Capital Allocation and Returns

At December 31st, 2025 the company reported negative stockholders' equity of approximately $(4.54) million compared to $(3.38) million at prior year-end reflecting accumulated losses post-merger [F1]. Operating cash flow turned modestly positive at about $39k driven mainly by working capital improvements after years of outflows; free cash flow was also positive around $30k following sharply reduced capex relative to prior year infrastructure investments including integration of DocSun assets acquired early 2024 which added amortization burdens now largely amortized away except residual intangibles expense reductions observed over reporting periods [F1], [S15]. No dividends or share repurchases occurred amid financial preservation needs.

Debt carries considerable risk: multiple notes payable totaling several hundred thousand dollars are in default or subject to refinancing arrangements contingent on capital raises that include conversion rights enabling lenders equity participation upon uplisting events but diluting existing shareholders if triggered [S24], [S25]. The current ratio near 0.06 underscores acute liquidity strain.

Competitive Positioning and Risks

Competition spans multiple domains:

- Established multinational suppliers dominate medical device channels;

- Nutritional supplement markets are fragmented but crowded with brands backed by larger companies investing heavily in R&D;

- Digital content algorithms compete against major ad platform monopolies like Google impacting Findit AI Connect’s reach;

- Telehealth sector growth increasingly populated by scalable AI diagnostic providers potentially eclipsing smaller firms’ offerings.

Regulatory compliance requirements across FDA Class I medical devices plus dietary supplement labeling regulations add complexity amid ongoing clinical trials whose outcomes remain uncertain yet crucial.

Liquidity challenges represent the most immediate existential risk: survival depends on securing sufficient financing without excessive dilution or restrictive covenants affecting strategic flexibility as highlighted explicitly by SEC filings citing going concern doubts compounded by defaulted debt exposing the company to creditor enforcement actions absent timely corrective capital market interventions [S24], [S26].

Conclusion

BioRegenx represents an ambitious health technology conglomerate pursuing scale within highly regulated competitive arenas marked by technological intensity spanning AI diagnostics combined with nutraceutical innovations targeting preventive healthcare segments projected for robust growth over coming years. While progress reducing losses signals operational improvement post-merger burden reduction the revenue decline alongside excessive leverage constrains near-term independent growth without substantial new capital infusion. Achieving clinical validation milestones alongside uplisting objectives remains critical pivot points underpinning potential transition toward sustainable profitability currently elusive given precarious balance sheet juxtaposed against a compelling yet capital-intensive strategy. Ultimately success hinges on navigating market penetration complexities amid competitive pressures while stabilizing finances — a challenging balance playing out under tight cash constraints.

This report is based solely on publicly filed regulatory disclosures without forecasts or investment recommendations. Readers should conduct independent due diligence before forming views on BioRegenx or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments