GIVBUX Faces Cash Strains While Expanding Its Fin-Tech Super App Platform

The company’s integrated mobile wallet platform blends payments, rewards, and charity but financial and competitive challenges weigh on progress.

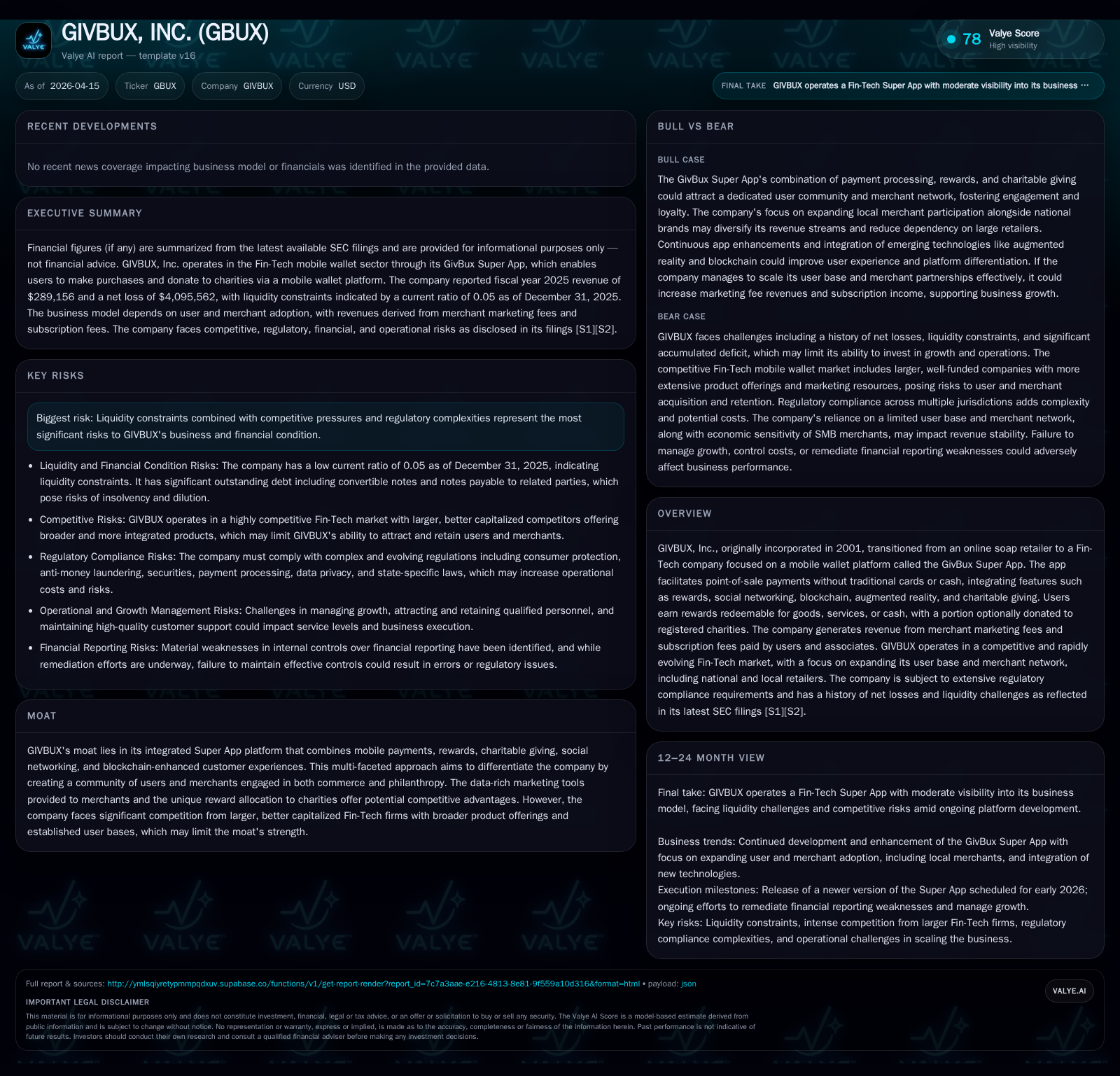

GIVBUX, Inc. has transitioned from an online retailer to a niche Fin-Tech player with its GivBux Super App, offering a mobile wallet combined with rewards, social networking, augmented reality, and charitable giving. Despite innovative features and an expanding merchant base concentrated in SMBs and national brands, the company remains unprofitable with deteriorating liquidity and a heavy debt load. Growth prospects hinge on user adoption and retention amid stiff competition from well-funded Fin-Tech firms. Regulatory complexity and risks around intellectual property further complicate the outlook. Monitoring capital raises or strategic partnerships will be critical to sustaining ongoing investment in product development.

Company Historical Performance and Transition

Originally incorporated in Colorado in 2001 as Rub-A-Dub Soap Inc., GIVBUX operated as an online retailer of handmade soaps until minimal revenues and significant losses led to a pivot. By 2006 it had shifted toward automotive tire manufacturing via Chinese subsidiaries but ceased reporting activity by 2009. The company underwent multiple restructuring efforts including a custodianship appointed by Nevada courts before merging with the fintech-focused GivBux entity in mid-2020 [S1]. This marked the start of its current line of business: operating the GivBux Super App.

The Super App is designed as an integrated mobile wallet solution enabling consumers to make point-of-sale payments without traditional plastic cards or cash. It layers in capabilities such as user-to-user communication via chat/video, blockchain-enabled customer experiences enhanced by augmented reality (AR), biometric security measures on cloud platforms for account protection, social media functionality, as well as embedded charitable giving where portions of rewards are donated automatically [S14].

Financial Results Overview (Annual)

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -4 | -1058101 | -2 | -23.5% |

| 2024 | -3 | -361541 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 82.8 |

| 2024 | 106.7 |

Source: SEC companyfacts cache [F1].

Source: [F1]

Revenues declined materially between FY2024 and FY2025 by approximately 47%, reflecting possibly subdued demand or increased churn in user subscriptions or merchant contracts [S15]. Operating losses improved by about 44%, narrowing from approximately -$3M to -$1.7M; however this still reflects significant negative profitability along with deepening net losses which widened due to other expenses including interest on debt obligations [F1]. Operating cash flow worsened sharply indicating ongoing cash burn.

Liquidity strains are severe with a current ratio near 0.05—the company holds just under $234K of current assets versus over $5.1M in current liabilities at the end of FY2025 [F1]. Negative equity also points to accumulated deficits surpassing invested capital.

Capital Structure and Cash Flow

Significant convertible notes payable totaling about $1.6M alongside related-party loans of roughly $0.8M burden the balance sheet [F1]. The credit facility detailed imposes covenants restricting further indebtedness while requiring minimum liquidity thresholds unlikely attainable given current cash flows [S16][S19]. If financing sources cannot be accessed or are too dilutive — particularly through further convertible securities issuance — shareholder value could erode materially.

Free cash flow remains negative due to ongoing R&D spending supporting app improvements scheduled for release in early 2026 along with marketing initiatives aimed at user growth [S14][S1]. Robust capital raises or strategic alliances may be required imminently.

Business Model Nuances

GivBux earns revenue primarily through merchant marketing fees—leveraging data-rich analytics provided via its integrated platform—and subscription fees paid by users and business associates [S14]. The platform supports transactions at many national retailers while increasingly targeting recruitment of local merchants to diversify offerings and reduce dependence on large brand partners [S14][S26].

User engagement metrics mention over 20,000 app downloads but full active user counts or conversion rates are not detailed; retention beyond initial acquisitions remains critical due to the subscription-based nature of revenue recognition [S14][S27]. The ability to cross-sell additional services within the app ecosystem forms a key strategy to raise average revenue per user.

Market Positioning and Competitive Landscape

In the crowded fintech wallet space, competitors include large incumbents benefiting from economies of scale, expansive service suites beyond payment processing (e.g., lending, wealth management), deeper financial resources for marketing spend and technology development [S10][S25].

Additionally, some merchants are developing proprietary payment ecosystems that could circumvent third-party platforms like GIVBUX [S25]. The company's multi-faceted Super App design incorporating social networking elements and charity-linked rewards aims for differentiation but faces risk that competitors may emulate core features rapidly or deliver more preferred innovations.

Regulatory Environment and Risks

GIVBUX navigates a multifaceted compliance landscape encompassing:

- Consumer protection frameworks including Truth in Lending Act (TILA) and Federal Trade Commission (FTC) oversight.

- Anti-money laundering requirements under Bank Secrecy Act (BSA) and ongoing transaction monitoring protocols limiting daily transfers ($1000/day) to detect suspicious payments [S26].

- Securities regulations mandated by SEC filings and OTC market oversight following its public reporting status post-merger.

- Payment card industry standards notably PCI-DSS for transaction security.

- Data privacy laws such as Gramm-Leach-Bliley Act (GLBA) plus California Consumer Privacy Act (CCPA), which impose constraints on personal data usage—company states it does not sell personal info externally [S20][S26].

- State-specific licensing laws requiring nuanced operational adjustments across jurisdictions.

- Tax compliance including IRS reporting obligations connecting transactional volumes with tax disclosures [S26][S22].

Noncompliance risks carry significant penalties including fines, litigation exposure, operational restrictions, and reputational damage affecting user uptake [S20][S24].

Intellectual Property Considerations

Protection around proprietary technologies remains tenuous given reliance on open source components subject to license conditions potentially exposing the company to litigation or compliance gaps [S23]. Patent filings have uncertain enforcement value while trademark similarity disputes may dilute brand distinction given competitor overlaps [S9][S13]. Disputes could lead to costly legal defense efforts detracting management focus from growth initiatives.

Growth Prospects and Key Milestones Ahead

The planned release of an updated Super App version early in calendar year 2026 reflects continuing product investment aimed at increasing user engagement through enhanced functionality such as better AR integrations and security features [S14].

Efforts are underway to broaden merchant onboarding particularly among local SMBs which historically form most of its base but remain prone to higher churn versus enterprises—success here could raise payment volume share driving incremental subscription renewals and upsells [S15][S27].

To improve metrics sustainably requires stepping up sales & marketing teams alongside R&D budgets without overshooting cash availability—a delicate balance acknowledged openly by management facing potential expense overruns if execution falters [S1]. Increased adoption rates across existing users’ multiple locations offer another avenue for organic growth less dependent on new client acquisition costs.

No explicit forward guidance was disclosed although monitoring quarterly trends for user count growth rates, subscription renewal percentages, merchant mix changes vs national brands will be critical signals pointing towards inflection points.

Returns / Capital Allocation Overview

Given persistent net losses coupled with negative operating cash flow (-$1.05M FY2025), there are no reported dividends or buyback programs; capital allocation focuses entirely on operational investments needed for scaling platform capabilities [F1]. Return metrics are currently negative; calculated rough ROE based on last fiscal year is highly distorted by negative equity standing at -$4.9M reflecting accumulated deficit rather than operational profitability [F1].

Capital structure highlights significant dilution risk via convertible securities issuance; future rounds may dilute existing shareholders if not balanced by meaningful enterprise valuation uplift [F1][S19]. Managing liquidity risk poses immediate importance for sustained operations.

Summary Perspective

GIVBUX presents an ambitious integration of fintech innovation—mobile wallets fused with social interaction plus philanthropy—that addresses customer behavior trends toward multi-dimensional digital engagement. However its growth journey is encumbered by financial strain stemming from eroding revenues amidst severe competitive pressures against scaled incumbents wielding wider technological stacks.

Regulatory complexity obliges substantial ongoing investments in compliance infrastructure while IP protections remain incomplete leaving open legal exposure avenues typical for emerging tech platforms reliant on open standards.

Going forward key watchpoints include progress expanding active user base beyond downloads; successful diversification away from predominantly national brands towards local merchants aiming at stickier network effects; ability to raise new financing without excessive dilution or debt burden increase; improvement in top-line stabilization reversing recent declines; managing cost structure aligning R&D plus marketing spends carefully against cash availability; ensuring regulatory adherence across multiple jurisdictions mitigating risks tied to privacy or payments rules violations.

Long term prospects depend critically on executing these growth drivers efficiently while fending off larger competitors’ price wars or feature replication.

This document is prepared solely for informational purposes based on publicly available SEC filings as of April 15, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments