CarMax’s Scale and Technology Drive Used Vehicle Retail Amid Margin Pressures

CarMax leverages its extensive network and proprietary tech to maintain leadership despite earnings pressures in fiscal 2026.

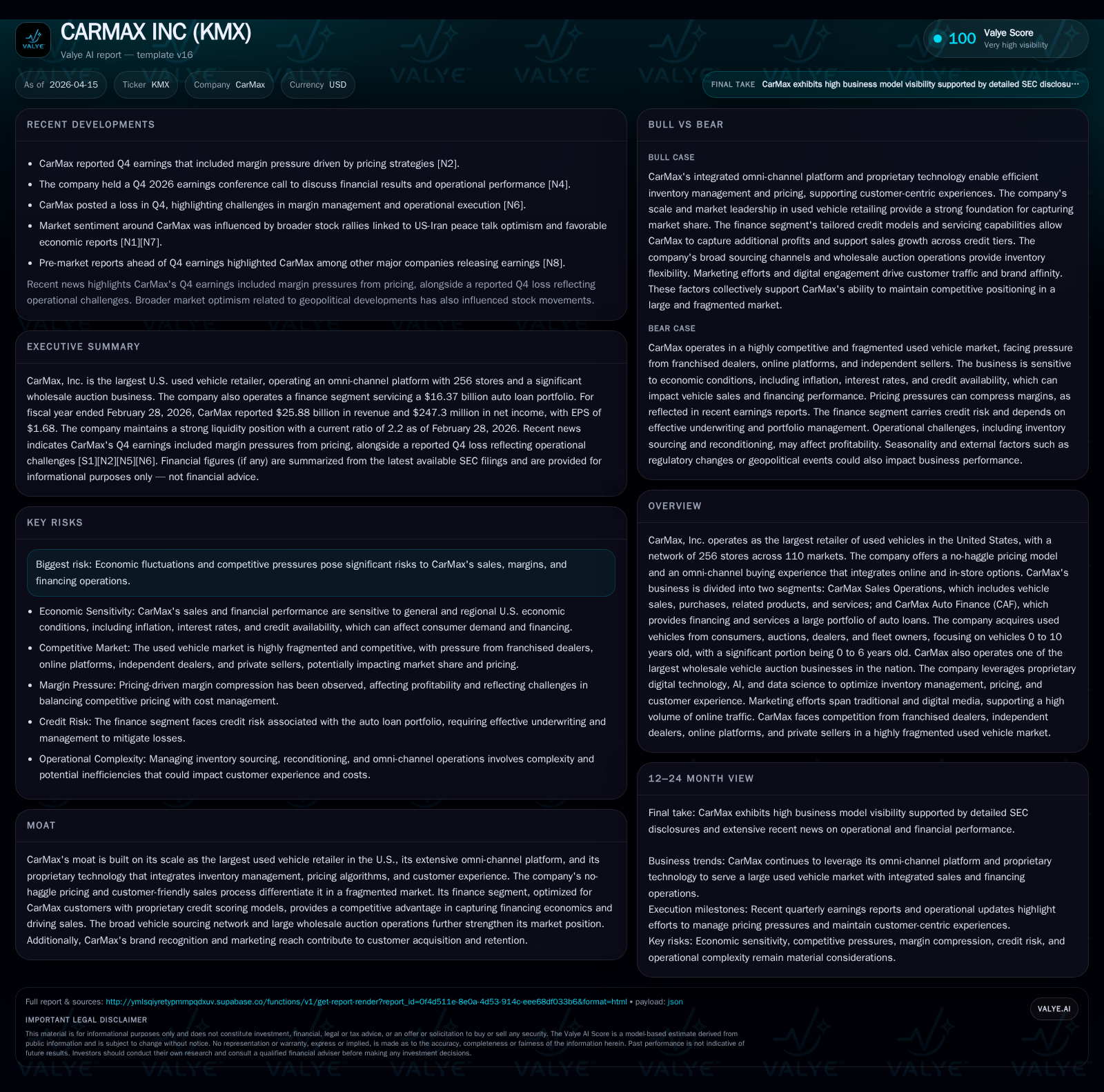

As the largest U.S. used vehicle retailer, CarMax continues to innovate with a no-haggle pricing model and omni-channel sales approach, integrating advanced AI and data science. Fiscal 2026 results reveal flat revenue but pronounced net income decline due to margin compression amid competitive pricing challenges. The company sustains strong operating cash flow growth and increases capital returns primarily through share buybacks. Future growth hinges on expanding financing penetration, enhancing wholesale auction capabilities, and adapting inventory for evolving automotive trends including EVs.

Historical Performance: Growth Trends and Earnings Dynamics

CarMax's fiscal year 2026 marked a challenging financial landscape with total revenue declining slightly by 1.8% to approximately $25.9 billion compared to $26.4 billion in the prior year [F1]. Despite stable top-line figures supported by continuing retail volumes, net income saw a steep fall of over 50%, down to $247 million from $501 million the previous year [F1]. This divergence underscores significant margin compression primarily driven by elevated used vehicle acquisition costs juxtaposed with intensified competitive pricing dynamics.

Contrasting the profitability contraction is an impressive surge in operating cash flow, which expanded by nearly 186% year-over-year reaching $1.78 billion in FY2026 [F1]. This strong cash generation capacity underpins the company's strategic capital deployment initiatives. Capex rose moderately by 15.6% to $541 million reflecting investments in store infrastructure and technology platforms essential for sustaining growth. Concurrently, share repurchases accelerated sharply with buybacks rising to $643 million from $428 million in FY2025, emblematic of a capital return focus supported by improved liquidity [F1][S4].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2026 | 25.9 | 247 | 1784 | 541 | -1.8% | -50.6% |

| 2025 | 26.4 | 501 | 624 | 468 | -0.7% | +4.5% |

| 2024 | 26.5 | 479 | 459 | 465 | -10.6% | -1.1% |

| 2023 | 29.7 | 485 | 1283 | 423 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 643 | 1243 | 4.2 |

| 2025 | 428 | 157 | 8.0 |

| 2024 | 94 | -7 | 7.9 |

| 2023 | 334 | 861 | 8.6 |

Source: SEC companyfacts cache [F1].

The table above summarizes CarMax's key financial metrics over the past four fiscal years as reported in SEC filings [F1].

Drivers Behind CarMax’s Market Leadership

CarMax’s preeminent position as the largest U.S.-based used vehicle retailer derives fundamentally from its extensive physical footprint combined with digital innovation [S7]. Operating 256 stores across more than a hundred media markets offers broad geographic reach that rivals cannot easily replicate. Complementing scale is a distinctive no-haggle pricing model that removes common friction points in car buying by providing transparent prices upfront.

The firm’s omni-channel platform empowers customers to purchase vehicles entirely online or through seamless online-to-in-store integration — supported by AI-driven tools like Skye, the virtual assistant facilitating customer engagement via chat or voice interfaces [S7][S18]. These tools reduce friction points along the customer journey while enhancing funnel efficiency.

CarMax’s inventory strategy leverages a proprietary centralized management system that constantly adjusts retail prices using algorithms incorporating sales velocity, consumer interest signals, seasonality effects, and regional demand patterns—an approach known as inventory turn optimization that balances stock freshness against depreciation risk [S11]. Approximately ninety-nine percent of offered vehicles are sold at listed prices without haggling.

Additionally, CarMax sources vehicles from consumers via both physical appraisal lanes and online instant offers enabled through proprietary digital channels like MaxOffer for dealers and sellers—a critical advantage allowing precise market segmentation through credit penetration modeling embedded within CAF’s underwriting engine optimized exclusively for CarMax buyer profiles [S21][S10][S25]. This finance arm drives roughly forty-two percent of retail vehicle purchases providing not only incremental profit pools but strategically reinforcing market share defense through tailored credit offerings covering broad borrower risk spectrums.

Complementing retail operations are virtual wholesale auctions largely focused on older units (>11 years / >100k miles), where licensed dealers acquire vehicles sold at high rates (circa ~99%) thanks to trust instilled through detailed condition disclosures and professional auctioneers ensuring transactional reliability [S24][S21].

Margin Compression and Profitability Challenges in Fiscal 2026

Despite steady revenues, CarMax experienced marked earnings pressure in FY2026 attributable largely to contraction in unit margins amid rising used car acquisition costs—reflecting broader inflationary impacts on automotive parts supply chains as well as competitive price reductions implemented defensively to preserve volumes in an increasingly crowded market comprising online direct sales platforms and third-party e-commerce facilitators [N1][N12][S1][S18].

The no-haggle pricing philosophy — a cornerstone of customer satisfaction — complicates margin management since price flexibility is constrained even as wholesale input prices fluctuate sharply. Management acknowledged during earnings calls that unit economics faced strain given transient imbalances between vehicle supply availability and consumer demand shifts during late calendar year phases of FY2026 [N1]. These pressures cascaded into a half-billion-dollar reduction of bottom-line profitability relative to prior year levels.

Simultaneously, competitive pressures within the CAF segment also exerted margin effects since competing lenders expanded enticing offers potentially eroding captive finance penetration rates; however, CAF maintained solid portfolio performance supported by proprietary credit scoring models calibrated specifically for CarMax channels mitigating credit losses risk effectively [N12][S10].[F1]

Future Growth Opportunities in Vehicle Sales and Financing

Looking ahead, CarMax posits multiple levers for future growth consistent with its strategic roadmap documented in recent filings [S5][S7]. A central thrust lies in deepening credit penetration across all credit tiers via CAF’s scalable financing platform enabling incremental unit sales driven by broadened access to tailored loan products across risk profiles previously underserved or served inefficiently.

Inventory diversification including expansion into hybrid and electric vehicles aligns with evolving consumer preferences signalling gradual transition toward cleaner automotive technologies—an imperative given industry secular trends altering sourcing, reconditioning protocols, and after-sales servicing requirements within used auto ecosystems.

Moreover, wholesale auction innovations—principally virtual auction formats introduced since FY2021—continue enhancing dealer participation rates providing new revenue streams while optimizing asset disposition cycles economically.

Data science enhancements underpinning dynamic price setting promise improved margin recovery potential through refined demand signal processing allowing more agile responsiveness to short-term market fluctuations consistent with preserving gross profit dollars per unit targets.

Nonetheless, these growth prospects remain conditioned on broader macroeconomic stability since any material economic downturn could restrict consumer discretionary spending power along with tightening credit availability impairing auto loan origination volumes particularly within subprime segments impacting CAF performance unfavorably [S20][N7].

Capital Allocation: Elevated Buybacks Amid Cash Flow Expansion

CarMax’s capital allocation profile evidences disciplined stewardship aligned with delivering shareholder value preservation under current earnings challenges [F1][S4]. Operating cash flow nearly tripled to $1.78 billion affording considerable liquidity flexibility supporting $643 million of share repurchases up substantially from prior year levels ($428 million). With no dividend issuance historically reported or declared reflecting retained reinvestment preferences alongside balance sheet optimization efforts maintaining a healthy current ratio (~2.2x) serves as a buffer amidst uncertain economic cycles.

Equity base consistency coupled with modest return on equity approximating just over four percent highlights conservative profit conversion while share buybacks likely seek per-share accretion compensating investors during episodic earnings malaise [F1].[F1]

Market Risks from Macroeconomic Factors and Competition

CarMax delineates several material risks affecting operational outlook centered on economic volatility influencing disposable income availability leading to fluctuating used vehicle demand levels as well as tightening consumer credit conditions affecting financing volumes such as increases in interest rates or changes in lending standards propagated across banking sectors servicing vehicle loans [S20][N7].

Competition manifests aggressively not only from traditional franchised dealerships but increasingly from digitally native auto retailers offering enhanced online purchase experiences sometimes coupled with alternative financing arrangements outside CAF's ambit reducing captive finance share potential [S18].[N7]

Regulatory compliance burdens spanning fair lending laws administered federally alongside variable state dealership regulations introduce ongoing operational complexity potentially raising costs or constraining business flexibilities particularly within finance operations adhering to truth-in-lending statutes overseen by bureaus like Consumer Financial Protection Bureau (CFPB) [S20].[N7]

Technology’s Role in Inventory and Pricing Optimization

A core pillar supporting CarMax’s differentiated customer experience lies within its proprietary technology stack integrating AI-driven assistants like Skye facilitating omnichannel customer engagement complemented by state-of-the-art pricing algorithm frameworks ensuring systematic adjustment of price points based on comprehensive real-time analytics encompassing sale velocity trends consumer browsing behavior seasonality factors together optimizing inventory turns while preserving targeted gross margin dollars per unit sold—terms frequently cited internally as pricing algorithm accuracy coupled with metrics tracking omni-channel funnel efficiency driving sustained shopper conversion rates across digital interfaces [S7][S18].[S11]

Technology adoption transcends front-end sales processes extending into back-office systems managing vehicle appraisal flows online instant offer mechanisms improving supply chain responsiveness enhancing overall operational agility further shielding competitive advantage amid marketplace digitization disruption risk.

Monitoring Key Milestones: What to Watch Next

Key indicators warrant monitoring include quarterly earnings performance for signals of margin stabilization or further deterioration amidst ongoing cost fluctuations as forecast guidance remains cautiously withheld pending evolving market conditions referenced in recent analyst commentary previewing Q4/FY26 results [N6][N7]. Other priority metrics comprise CAF financing acceptance rates alongside same-store sales volume trends serving as early proxies for underlying demand elasticity amidst tight credit markets.

Additionally technical metrics like vehicle transfer request proportions reflecting omni-channel platform usage intensity plus wholesale auction sell-through rates offer granularity on operational execution effectiveness supporting recovery potential narratives.

Disclaimer: This report is prepared solely for informational purposes based on publicly available data including SEC filings and news sources; it does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments